Past revenue performance isn’t always a reliable indicator of the best investment. Intel stock has more than doubled year to date, as it taps into a new wave of demand for its chips.

Nvidia (NVDA -2.86%) benefits from the strong demand for its superpowerful graphics processing units (GPUs) used in the most advanced artificial intelligence (AI) workloads. It has a much greater scale than Intel (INTC -4.06%), whose central processing units (CPUs) have taken a back seat to GPUs.

However, Intel shares have rocketed 154% year to date as data center demand is spreading across the semiconductor industry. Intel is benefiting from the growing demand for CPUs serving as the orchestration layer for AI. This shows shifting dynamics taking place in the industry as the data center build-out continues.

Nvidia: A Pattern of Uninterrupted Revenue Growth

Nvidia primarily generates revenue by selling GPUs and networking equipment for data centers, automotive manufacturers, and gaming.

The company posted a stellar 73% year-over-year increase in revenue in the fiscal fourth quarter, with a net income margin of 63%.

NASDAQ: NVDA

Key Data Points

Intel: Trying to Stabilize Revenue

Intel earns its revenue by designing and manufacturing CPUs and related technologies for personal computers, cloud providers, and enterprise systems.

It just surprised Wall Street with a strong first-quarter earnings report. Revenue grew 7% year over year — its highest growth rate in eight quarters. It reported a -31% net income margin for the quarter.

NASDAQ: INTC

Key Data Points

Why Revenue Matters for Retail Investors

Revenue is the most basic measure of a company’s performance. It shows investors how much money it earned from product sales. Importantly, changes in revenue over time speak volumes about a company’s addressable market, expansion potential, and ability to reach more customers.

Image source: The Motley Fool.

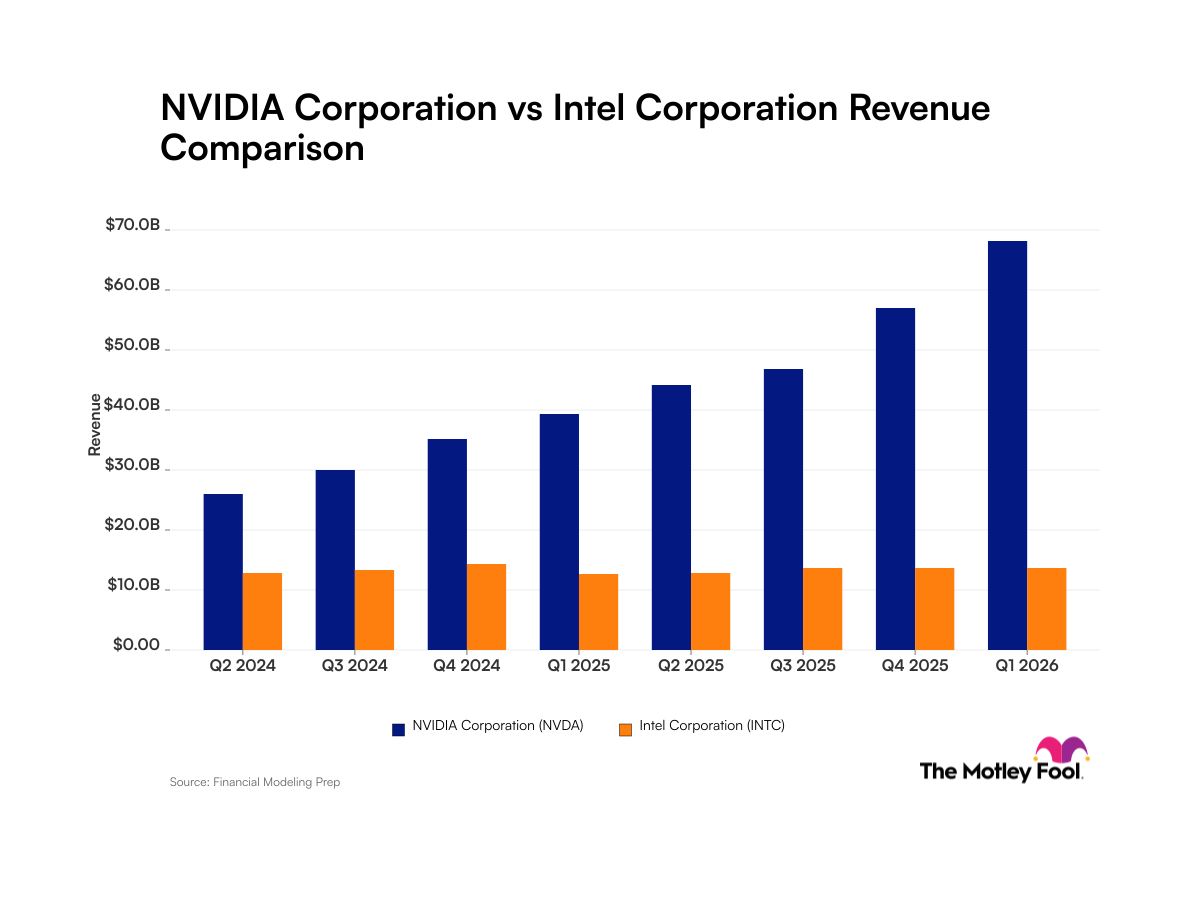

Quarterly Revenue for Nvidia and Intel

| Quarter (Period End) | Nvidia Revenue | Intel Revenue |

|---|---|---|

| Q2 2024 | $26.0 billion (period ended April 2024) | $12.8 billion (period ended June 2024) |

| Q3 2024 | $30.0 billion (period ended July 2024) | $13.3 billion (period ended Sept. 2024) |

| Q4 2024 | $35.1 billion (period ended Oct. 2024) | $14.3 billion (period ended Dec. 2024) |

| Q1 2025 | $39.3 billion (period ended Jan. 2025) | $12.7 billion (period ended March 2025) |

| Q2 2025 | $44.1 billion (period ended April 2025) | $12.9 billion (period ended June 2025) |

| Q3 2025 | $46.7 billion (period ended July 2025) | $13.7 billion (period ended Sept. 2025) |

| Q4 2025 | $57.0 billion (period ended Oct. 2025) | $13.7 billion (period ended Dec. 2025) |

| Q1 2026 | $68.1 billion (period ended Jan. 2026) | $13.6 billion (period ended March 2026) |

Data source: Company filings. Data as of April 28, 2026.

Foolish Take

Demand for Nvidia’s GPUs and other computing solutions for data centers has sent its revenue sharply higher over the last decade. It has accelerated since 2022, as hyperscalers pour more resources into building cutting-edge data centers for AI.

Intel has lost market share in both consumer and enterprise server markets, but it’s starting to find its footing. Its improved growth last quarter shows that the growing use of AI agents, robots, and edge AI use cases is starting to flow through to its revenue performance.

On a trailing-12-month basis, Nvidia’s revenue is almost $188 billion, towering over Intel’s $53 billion. Nvidia is growing much faster and generates much higher profit margins. Even with improving demand for CPUs, it’s a tall task for Intel to catch Nvidia.

It’s unclear how much Intel’s revenue may accelerate from here. But AI is expanding the semiconductor addressable market to $1 trillion, making it a big market spanning different types of chips. Intel’s guidance calls for second-quarter revenue to increase between 2% to 9% year over year.

Intel has found a valuable role to play in the AI market, but Nvidia may continue to widen its financial gap as it grows faster off a larger revenue base.