Arm Holdings (ARM -8.14%) and Qualcomm (QCOM -2.42%) are two established chip companies with more opportunities opening up due to artificial intelligence (AI). Everything from cars to consumer devices will be transformed by this technology, driving growing demand for chips.

While Arm has grown its revenue at higher rates over the past few years, Qualcomm is worth watching as it shifts its business to tackle the huge opportunity opening up in consumer devices.

Arm: Steady Upward Revenue Momentum

Arm architects, develops, and licenses central processing units (CPUs) products and related foundational technologies for original equipment manufacturers globally.

In the first quarter of 2026, revenue grew 20% year over year. Its business model is centered on licensing and royalties from its chip designs, resulting in a healthy 21% net income margin for the quarter.

NASDAQ: ARM

Key Data Points

Qualcomm: Managing High Revenue Fluctuations

Qualcomm develops and commercializes foundational wireless technologies, providing integrated circuits and system software for global communications networks.

Revenue growth has been slowing over the past year, and fell 3.5% year over year in the first quarter. This comes amid a strategic shift away from the handset market to pursue better prospects in automotive, the Internet of Things, and data center segments. It reported a net income margin of nearly 70% for the quarter.

NASDAQ: QCOM

Key Data Points

Why Revenue Matters for Retail Investors

Revenue is the most fundamental measure of a company’s performance. Changes over time can give investors insights into a business’s competitive position and growth potential.

Image source: The Motley Fool.

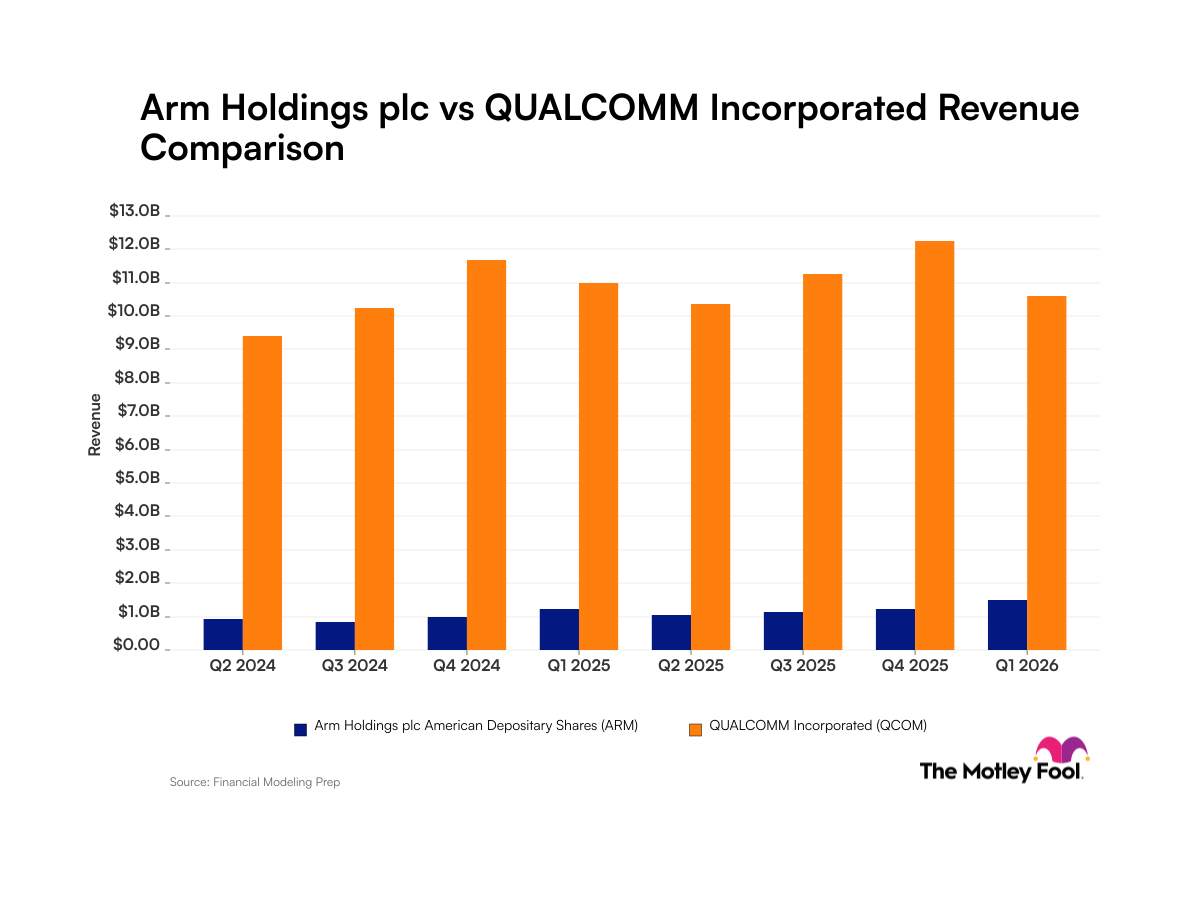

Quarterly Revenue for Arm and Qualcomm

| Quarter (Period End) | Arm Revenue | Qualcomm Revenue |

|---|---|---|

| Q2 2024 | $939.0 million (period ended June 2024) | $9.4 billion (period ended June 2024) |

| Q3 2024 | $844.0 million (period ending Sept. 2024) | $10.2 billion (period ending Sept. 2024) |

| Q4 2024 | $983.0 million (period ended Dec. 2024) | $11.7 billion (period ended Dec. 2024) |

| Q1 2025 | $1.2 billion (period ended March 2025) | $11.0 billion (period ended March 2025) |

| Q2 2025 | $1.1 billion (period ended June 2025) | $10.4 billion (period ended June 2025) |

| Q3 2025 | $1.1 billion (period ended Sept. 2025) | $11.3 billion (period ended Sept. 2025) |

| Q4 2025 | $1.2 billion (period ended Dec. 2025) | $12.3 billion (period ended Dec. 2025) |

| Q1 2026 | $1.5 billion (period ended March 2026) | $10.6 billion (period ended March 2026) |

Data source: Company filings. Data as of May 28, 2026.

Foolish Take

Comparing revenue growth between two companies in the same industry, in this case, semiconductors, can usually point investors to the better investment. It’s no surprise that Arm stock has significantly outperformed Qualcomm over the past three years, rising almost 600% compared to Qualcomm’s roughly 123% return.

Qualcomm is a profitable company with a long history of delivering growth. Still, Arm is seeing its chip designs used in several markets, including automotive, which are becoming increasingly computerized.

Arm is positioned to benefit from the growth in AI agents, where CPUs are in high demand. Meanwhile, Qualcomm is currently transitioning its lineup to focus on the opportunities in data centers and AI-powered consumer devices, including smart glasses, which it believes could become as widely adopted as smartphones.

Given Qualcomm’s strategic shift underway, it will be worth watching to see whether it can accelerate revenue growth over the next few years, or if Arm continues to grow faster and narrows the revenue gap.