Cisco Systems (CSCO 1.74%) is best-known for providing the IT hardware (switches and routers) that drive the internet, but investors may need to rethink that view in the future. The company's fourth-quarter results, which were reported Aug. 17, reveal a company generating growth from its non-core product offerings while continuing its transition toward more software and subscription revenue. Let's take a look at trends investors should watch.

Image source: Cisco Systems.

Cisco Systems' fourth-quarter results: The raw numbers

The headline figures:

- Revenue growth of 2% came in at the high end of the guidance range of 0% to 3%.

- Non-GAAP total gross margin of 64.6% was above the guidance range of 63% to 64%.

- Non-GAAP EPS of $0.63 came in above the guidance range of $0.59 to $0.61.

Clearly, Cisco reported a good quarter, but the guidance for the first quarter of FY 2017 predicts a slowing of revenue growth and decline in gross margin:

- Revenue growth guidance of negative 1% to 1%.

- Non-GAAP gross margin guidance of 63% to 64%.

- Non-GAAP EPS expected to range from $0.58 to $0.60.

When pushed on why guidance looks weak, CEO Chuck Robbins discussed two issues in the conference call. He talked about uncertainty about how emerging-market and service provider demand -- both negative in the fourth quarter -- would play out in the first quarter. Service providers typically generate around half of routing revenue, so it was no surprise to see routing revenue down 5.8% in the quarter compared to the same period last year.

More positively, Robbins said the guidance decline was part of the company's transition to a software and subscription business as revenue is recognized over time rather than initially, as with product sales.

Restructuring and core vs. non-core growth

Cisco's business is changing. Its core switching and routing products are growing slower than its non-core revenue. For example, a look at revenue growth for switching and routing (the combined figure is also included) shows lackluster growth in recent quarters.

Data source: Cisco Systems presentations.

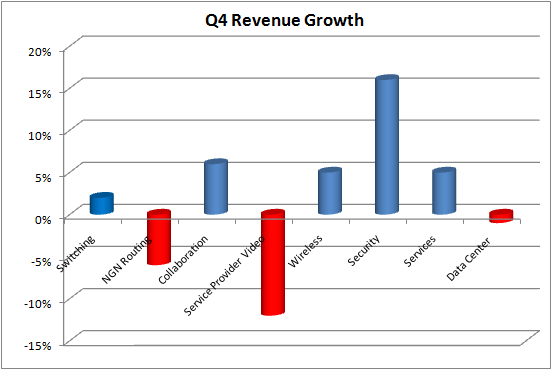

Meanwhile, a breakout of revenue growth in the most recent quarter shows how non-core areas like wireless, collaboration, and security generated good growth. In addition, Cisco continued its good run with services growth. It came in at 5% following a normalized growth rate of 4% in the third quarter, and 3% and 1% in the previous quarters.

Data source: Cisco Systems presentations.

The principle of slowing core growth relative to non-core growth was further highlighted by substantive restructuring measures announced in the earnings release and conference call. Robbins said on the call: "Today we announced a restructuring, enabling us to optimize our cost base in lower growth areas of our portfolio, and further invest in key priority areas, such as security, IoT, collaboration, next-generation data center, and cloud."

The restructuring will eliminate up to 5,500 positions, representing 7% of the company's global workforce, and CFO Kelly Kramer said the restructuring would create up to $700 million in pre-tax charges with $325 million to $400 million expected in the first quarter.

Deferred revenue

Another important part of the transition to a software and subscription business model is something called deferred revenue. It's an important metric to follow because as a company shifts from hardware sales toward subscription-based sales, it typical suffers a loss of upfront revenue in favor of longer-term subscription revenue. The latter is recognized over time; meanwhile it sits on the balance sheet as deferred revenue.

As you can see below, Cisco's deferred revenue increased in the fourth quarter after sequentially flat-lining in previous quarters -- a good sign.

Data source: Cisco Systems presentations.

The strength in services and deferred revenue growth is a sign that Cisco's transition is working. In addition, non-core revenue growth looks solid. Cisco was affected by weakness in emerging markets and service provider demand in the quarter, but its core revenue growth has been tepid for a while now. There were a lot of moving parts in the quarter, but the key takeaway is that Cisco's business is in transition.