A Home Depot (HD +0.01%) investment looks like a solid deal as investors head into the new year. Its sales, earnings, and profitability figures are all at record highs even as shares have gotten cheaper relative to its main rival, Lowe's (LOW +0.01%).

Before you pull the trigger on any stock purchase, though, it's important to familiarize yourself with the company you're considering buying. Not only does that knowledge inform your initial investing decision, but it also protects you from hasty selling moves based on short-term business dips. With that in mind, here are a few top trends that any shareholder should know about Home Depot.

Growth slowdown

Home Depot is growing faster than most retailers (including Lowe's) right now. It last posted 6% comparable-store sales gains, versus 3% for its smaller competitor. However, that growth isn't as robust as it used to be. The company enjoyed 4% higher customer traffic in each of the last two fiscal years but has seen that pace decelerate to 3% in 2016.

Home Depot is offsetting the shopper showdown by soaking up market share in the professional contractor segment of the industry. These customers tend to spend more per trip (upwards of $900), and so even a small boost in their visit frequency can go a long way. If overall traffic growth continues to decelerate, though, revenue gains over the next few years could disappoint.

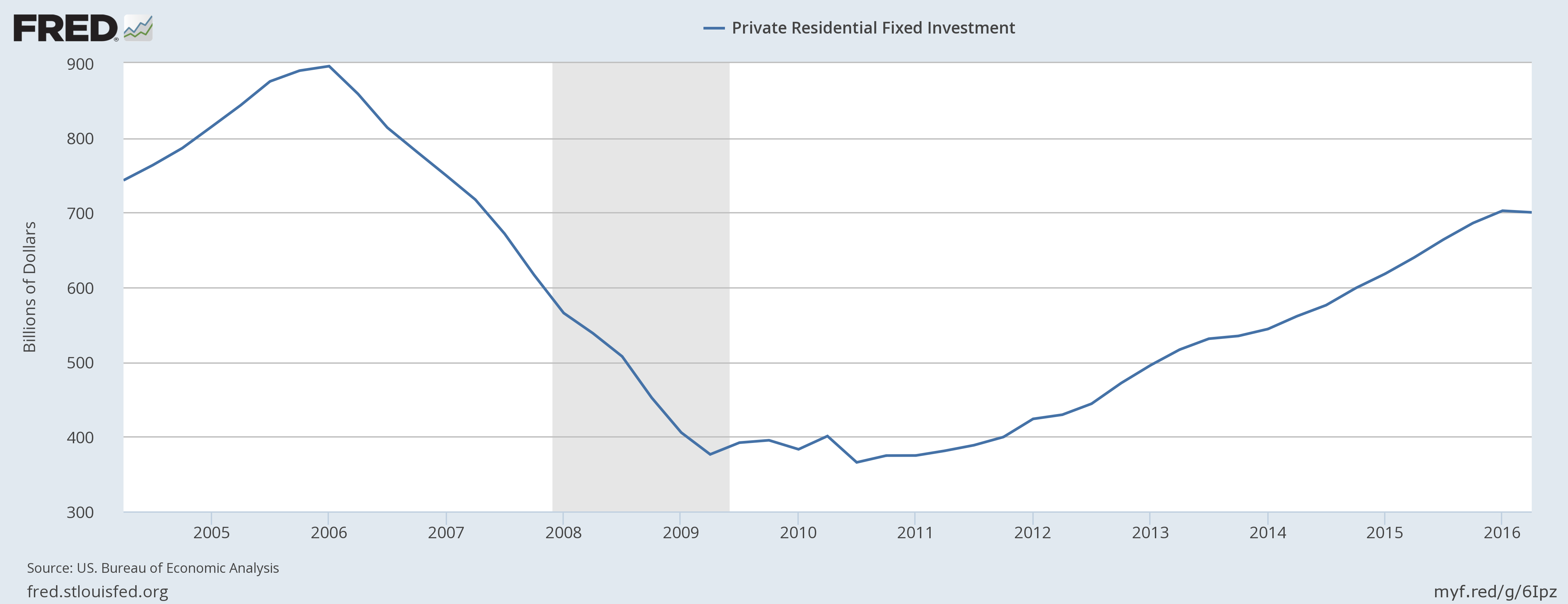

Market risks

Home Depot's business is heavily dependent on the stability of the housing market. It doesn't need boom times to enjoy solid growth, but it certainly hasn't hurt that Americans are now spending $700 billion per year on home improvement projects -- up from $400 billion in 2010.

There's room for further gains ahead. In fact, Home Depot projects that an aging stock of homes and below-average rates of housing formation point to an expanding market at least through 2018. That should help the company pass $100 billion of revenue, and $15 billion of operating profit, by that time. There's always a risk that the market turns lower, though, as it did during the housing market crisis that sliced Home Depot's earnings in half from 2006 through 2009.

Unusual expansion plan

Unlike Lowe's, Home Depot isn't benefiting from a fast-growing store base. In hasn't opened a new location in the U.S. in the last three years, while Lowe's tacked on 40 warehouses in 2016. That stable physical footprint puts pressure on existing locations to deliver nearly all the sales gains.

On the positive side, it also leaves more cash available for major business initiatives like building up the e-commerce infrastructure and pushing into complementary markets like maintenance, repair, and operations.

Dividend quirks

A Home Depot stock purchase includes an attractive dividend income stream. The payout has surged higher by double digits in each of the last three years. For perspective, consider that Home Depot's 2016 dividend is roughly equal to what the retailer earned in total profit just five years before.

Home Depot allocates a larger portion of its earnings to dividend payments, at 50% compared to Lowe's annual target of 35%. While that aggressive capital return strategy supercharges growth, it also exposes the dividend to market shocks. Home Depot had to suspend annual increases during the worst of the housing crisis while Lowe's succeeded in keeping its long-term growth streak alive.

Getting a good deal

In part because of the factors outlined above, Home Depot's stock has trailed the broader market over the last year. The good news for prospective shareholders is that the underperformance has made shares cheaper even as the business's earning power has improved.

Home Depot's dominant position in its industry, coupled with market-leading capital allocation efficiency, make it a more attractive long-term buy at 22 times trailing earnings than at the 25 price-to-earnings ratio investors paid at the start of 2016. It's also a nice discount over the 26 times earnings that they're currently shelling out for Lowe's.