Sometimes it's difficult to change the way you think about a stock. In the case of Rockwell Automation (ROK +0.33%) the company has always been seen as an all-purpose way to play trends in the industrial sector. However, given the importance of the company's sensors, controls, software architecture, and automation solutions to the Industrial Internet of Things (IIOT), it's time to start thinking about the company as a long-term way to play the growth of IIOT -- something that might encourage a positive rerating in the stock. Let's take a closer look.

IIOT to the rescue

In a world where moderate economic growth is restricting the ability of industrial companies to aggressively grow revenue, it's becoming increasingly important to make productivity improvements. It's also essential to wring every bit of growth that can be wrung out of existing customers, and offer new solutions to those existing customers.

This is where IIOT comes in. In a nutshell, embedding internet-enabled devices into hardware and then monitoring and analyzing the data that comes out of their actions -- think the functioning of a General Electric Company (GE +1.35%) gas turbine or aircraft engine -- helps the end user utilize that asset in a more productive way. In this way, industrial companies like GE and Honeywell International (HON -1.27%) can offer IIOT solutions to their hardware customers.

Image source: Getty Images.

Honeywell and General Electric Company

Around half of Honeywell's engineering force is employed in developing software as its aerospace and building solutions (both industries that require constant monitoring and service), while Jeff Immelt has aggressively invested in order to ensure GE is the leading player in IIOT. In addition, the incorporation of GE's digital offerings is an integral part of the rationale for GE's acquisition of Alstom's energy assets and the Baker Hughes merger.

Both companies, and others, are urgently developing IIOT solutions and creating market awareness. In truth, it's somewhat of a symbiotic process. For example, the more GE promotes its Predix Cloud offering, a platform-as-a-service solution that helps companies capture and analyze data, the more developers will create applications for industrial customers to use on the platform. Ultimately, more and more companies will likely see the benefits of adopting IIOT solutions.

The potential for growth is significant. For example, Honeywell cites an Accenture survey stating that 84% of business leaders believe IIOT can benefit them, but only 7% have a working IIOT strategy.

Here's where Rockwell comes in

Clearly, as market adoption of IIOT increases, it will be good news for Rockwell, although it's fair to say that the stock's 22% appreciation in 2017 to date isn't necessarily a consequence of investors recognizing the long-term potential of its IIOT-based solutions. It probably has more to do with the cyclical uptick in U.S. industrial production and its impact on the willingness of Rockwell's customers to make capital investments.

The improvement in the macro-outlook is evident in Rockwell's revised full-year 2017 guidance. For reference, Rockwell's financial year finishes at the end of September. As you can see below, the increase in guidance has been significant -- the increase in the midpoint of EPS guidance is 7.3% higher.

|

Full-Year Guidance |

April |

January |

|---|---|---|

|

Organic sales growth |

4.5% to 7.5% |

1% to 5% |

|

Segment operating margin |

20.5% |

20% |

|

Adjusted EPS |

$6.45 to $6.75 |

$5.95 to $6.35 |

|

Free cash flow as a % of adjusted income |

>105% |

>100% |

Data source: Rockwell Automation presentations.

Future growth and valuation

If the argument holds that the stock price increase in 2017 is due to the near-term guidance hike, then it's good news, because it means there is an opportunity for investors to buy into Rockwell's long-term potential for IIOT-led growth. The best case for buying stock in Rockwell is based on the idea that growth prospects inherent in its IIOT-based solutions will mean its organic sales growth will be in excess of industry capital spending growth in the future.

Dara source: Rockwell Automation presentations.

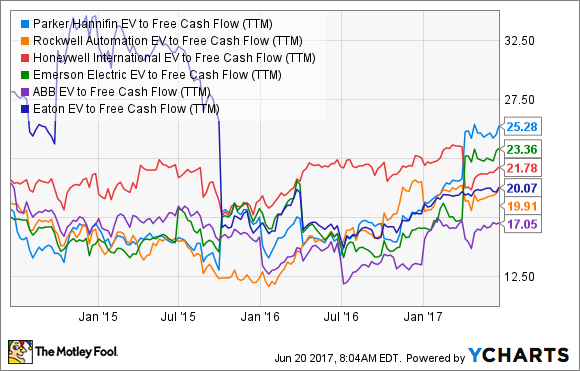

Moreover, Rockwell is an asset-light business that tends to convert income to free-cash flow at a rate in excess of 100%. As such, on an enterprise value (market cap plus net debt) to free-cash-flow basis, the stock trades toward the bottom end of its peer group.

PH EV to Free Cash Flow (TTM) data by YCharts.

The bottom line

As mega-cap companies like General Electric and Honeywell continue to invest in order to create market awareness and adoption of IIOT solutions, it will increase investment in the kind of connected automation solutions offered by Rockwell. It's a compelling investment proposition and makes Rockwell attractive for long-term investors looking to catch a favorable industry trend.