As the two biggest retailers in their industry, Lowe's (LOW 1.86%) and Home Depot (HD 1.71%) might appear to be equivalent bets on a healthy home-improvement market. Both stocks are enjoying solid sales growth and expanding profitability, after all, as they benefit from positive long-term economic trends like an aging housing stock and rising household formation rates.

Given their overlapping customer profile, you might look at the choice between the two stocks as pitting the market leader, available at a premium, against the runner-up, which can be purchased at a discount.

Image source: Getty Images.

But read on below to see why Lowe's isn't just a cheaper version of Home Depot.

To start, let's stack the two retailers against each other with a few key metrics.

Home Depot vs. Lowe's stock

|

Metric |

Home Depot |

Lowe's |

|---|---|---|

|

Market cap |

$183 billion |

$65 billion |

|

Sales growth |

6.9% |

10.1% |

|

Net profit margin |

8.4% |

4.8% |

|

Dividend yield |

2.3% |

2.2% |

|

Forward P/E |

21 |

17 |

Sales growth and profit margin are for the 2016 fiscal year. Data sources: Company financial filings and Yahoo! Finance.

Operating and financial trends

Lowe's is growing overall sales at a faster clip, and that's just what you might expect from a smaller rival that has aggressive expansion plans. The company is on pace to add 35 new warehouses to its base this year, for example, while Home Depot holds its store footprint steady.

But there really isn't much of a growth difference between these two companies. Home Depot's sales gains are far stronger at its existing locations. Its comparable-store sales were up 6% last quarter, while Lowe's was up just 2 %. That gap helps explain why Home Depot is expecting to boost overall revenue by the same 5% that Lowe's is targeting, despite its far larger sales base and more modest store expansion plans.

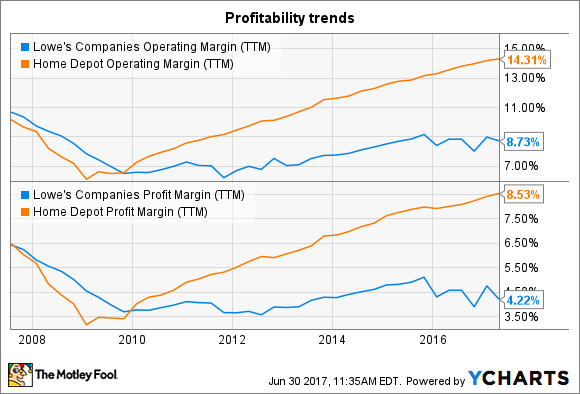

While revenue growth is basically a tie, the financial trophies in this match-up all go to Home Depot. The market leader's operating profit margin is much higher (14% compared to 9%), as is bottom-line profitability (8.4% vs. 4.8%). These numbers are not only stronger on Home Depot's side, but they also show just how much better the retailer has executed in taking advantage of the rebounding housing market over the past few years.

LOW Operating Margin (TTM) data by YCharts.

Home Depot's return on invested capital is nearly 30%, which blows away Lowe's 13% result and also makes this retailer one of the most efficient businesses on the stock market.

Dividend stocks

Both companies are attractive income investments, yielding over 2%. Yet Lowe's edges past Home Depot on the reliability of its payout. The retailer protected its annual hikes even during the worst of the housing market crises. Home Depot, in contrast, paused its increases for nearly three years. That means Lowe's is still a Dividend Aristocrat while Home Depot's streak of unbroken annual raises isn't nearly long enough to qualify it for membership in that exclusive club.

Income investors have received similar dividend growth from both investments recently, as payout hikes routinely come in at 20% or more each year. Home Depot's management is targeting faster growth ahead. Earlier this year, the company raised its payout target to 55% of sales from 50%, and at the same time announced a 29% spike in the annual dividend. Lowe's capital allocation plans call for just 35% of earnings to be returned through dividend payments.

Valuation

Lowe's stock is priced at a big discount to Home Depot's both in terms of earnings and sales. In fact, the price-to-sales gap is at a 10-year high, with investors paying about twice Home Depot's annual revenue for its business compared to just 1 times for Lowe's.

Conservative investors might see that as a compelling opportunity to buy Lowe's and simply wait for its operations, finances, and valuation, to catch up to those of its bigger rival. But the smarter money, in my view, is on the market leader who has a demonstrated ability to soak up market share even while it keeps its store footprint steady.