Jul 26, 2026 by Matt DiLalloBloom Energy's Next Earnings Report on July 28 Could Send the Stock Soaring. Here's Why.Bloom Energy's second-quarter financial results could prove to be a powerful catalyst for the stock.

Jul 26, 2026 by Reuben Gregg BrewerGE Aerospace has a Backlog Worth $210 Billion. Here's Why I'm Still Not BuyingGE Aerospace is performing very well as a business, and perhaps even better as a stock.

Jul 26, 2026 by Daniel SparksHSBC Just Started Covering SpaceX With a $115 Price Target. The Stock Closed Friday at $115.07.A big bank just valued the rocket maker with a 2x Elon Musk premium baked in -- and still came up short of the IPO price.

Jul 26, 2026 by Reuben Gregg BrewerGE Aerospace has a Backlog Worth $210 Billion. Here's Why I'm Still Not BuyingGE Aerospace is performing very well as a business, and perhaps even better as a stock.

Jul 26, 2026 by Joe TenebrusoWhy SLB Stock Surged This Past WeekThe world needs dependable energy, and the oil and gas services giant is helping its customers supply it.

Jul 26, 2026 by Daniel SparksHSBC Just Started Covering SpaceX With a $115 Price Target. The Stock Closed Friday at $115.07.A big bank just valued the rocket maker with a 2x Elon Musk premium baked in -- and still came up short of the IPO price.

Jul 26, 2026 by Keithen DruryMicrosoft and Meta Platforms Are Negative in 2026. Here's My Favorite One to Buy Now.Both stocks are cheaper than the S&P 500.

Jul 26, 2026 by Reuben Gregg BrewerJamie Dimon Said Markets Are Underestimating Risks Shifting "Like Tectonic Plates." He Made the Warning Right After JPMorgan Posted Its Best Quarter Ever.The CEO of JPMorgan Chase thinks investors may be ignoring risks such as geopolitical conflict and spending deficits.

Jul 26, 2026 by Daniel SparksAT&T Beat on Earnings, Announced a $10 Billion Buyback, and Still Trades at 8 Times Earnings With a 4.6% Yield.The telecom already has a plan for every dollar of its massive free cash flow stream -- and investors should love it.

Jul 26, 2026 by Marc GubertiTexas Instruments Can Ride AI Demand to New HighsTexas Instruments' analog chips act as the middlemen between the electric grid and AI chips.

Jul 26, 2026 by Bram BerkowitzMicrosoft's Next Earnings Report on July 29 Could Send the Stock Soaring. Here's Why.Microsoft stock has struggled this year.

Jul 26, 2026 by Jake LerchPINK vs. XLV: How Do These Two Health Care ETFs Match Up?PINK outperformed XLV by 8.7 percentage points over one year, but carries higher fees and volatility. XLV offers lower costs and a higher dividend yield for passive healthcare exposure.

Jul 26, 2026 by Robert IzquierdoFord Motor vs. Tesla: What The Revenue Trends of These Automotive Giants Tell InvestorsFord's revenue base remains larger, but Tesla's latest quarter shows a sharp rebound that narrows the gap.

Jul 26, 2026 by Adam SpataccoForget IonQ, Rigetti Computing, and D-Wave Quantum. This Trillion-Dollar Artificial Intelligence (AI) Stock Is the Best Quantum Computing Opportunity, and It's Currently Trading at a 7-Year Valuation Low.Quantum computing pure plays may tempt investors, but the better stock pick may be the megacap that's providing a bridge between quantum systems and classical supercomputers.

Jul 26, 2026 by Jake LerchVWO vs SPGM: What Are the Key Differences Between These Two Popular ETFs?SPGM delivered stronger 1-year returns and lower volatility, while VWO offers cheaper fees and higher dividend yield for emerging market exposure.

Jul 26, 2026 by Daniel SparksAmerican Airlines Cut Its Full-Year Guidance. The Stock Rose 6.8% the Next Day.The airline just posted the biggest quarter in its history and told investors it may lose money this year. Both are true.

Jul 26, 2026 by Keithen DruryPrediction: Alphabet Will Beat Apple to a $5 Trillion Market CapApple has a headstart, but it's not stable.

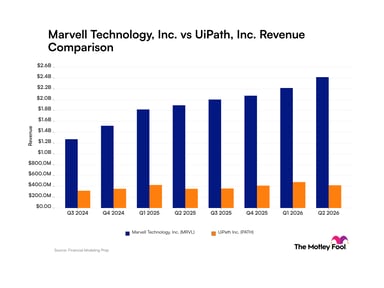

Jul 26, 2026 by Robert IzquierdoMarvell Technology vs. UiPath: What Do the Quarterly Revenue Trends of These Artificial Intelligence Companies Tell Investors?Marvell maintains a commanding revenue lead, but UiPath's latest quarter shows accelerating growth that narrows the gap.

Jul 26, 2026 by Matt DiLalloRetail Investors Are Pulling Money From Blackstone's Private Credit Fund. Here's What Its Latest Quarter Says.Private credit isn't even the main story at Blackstone.

Jul 26, 2026 by Lawrence NgaWhy CoreWeave Stock Fell 30% in Just 1 MonthThe neocloud company's stock has plunged, but its business model hasn't suddenly broken.

Jul 26, 2026 by Maurie Backman3 Reasons I Plan to Downsize in Retirement -- Despite Having a Paid-Off HomeShedding square footage is a no-brainer for me.

Jul 26, 2026 by Dana GeorgeThe Promise Act Would Push Congress to Vote on Social Security Reform Before 2032's Projected 22% Benefit Cut for RetireesA bipartisan group of U.S. senators has come together to try to ensure that Congress finds a solution to the upcoming Social Security trust fund shortage.

Jul 26, 2026 by David DierkingHere's How Much You'd Need to Invest in SCHD to Generate $1,000 per Month in DividendsThe Schwab U.S. Dividend Equity ETF (SCHD) has become one of the industry's premier dividend ETFs.