Wall Street is an interesting beast, acting as a weighing machine over the long term but subject to emotional gyrations over shorter periods. It can be hard to fight the mood of the market, but if you can think long term while others are focused on the short term, you can find some solid investments. Three that are worth a very close look today are high-yielding ExxonMobil (XOM -0.24%), Tanger Factory Outlet Centers (SKT +0.22%), and General Mills (GIS +0.70%). Here's a quick rundown of why you might want to buy these stocks right now.

1. A rock solid energy giant

Exxon is offering investors a 4.4% yield. That's around the highest yield for the stock since the 1990s. Now is a pretty good time to pick up the shares if you are an income investor. Meanwhile, the company has an incredibly strong balance sheet, with long-term debt at less than 10% of the capital structure. That's low for any industry, let alone the often-volatile energy space.

Image source: Getty Images.

The yield is so high today because investors are worried about the integrated energy giant's production and its return on capital employed (ROCE, a measure of how well Exxon uses shareholder cash). Both metrics have been declining in recent years. But things have started to look up on both accounts, as management begins taking action on its long-term plans.

On the production front, Exxon has increased its output sequentially in each of the last two quarters. Since the uptick was driven by just one of several focus areas, 2018 looks like it will turn out to be a key inflection point for the company's upstream (drilling) business.

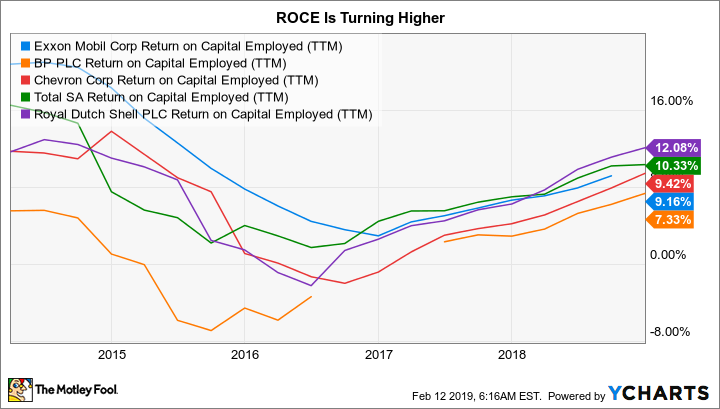

With regard to ROCE, Exxon is stuck in the middle of its peer group after years of leading the pack. However, ROCE has started to turn higher again. Management's goal is to push ROCE from the mid-to-high-single-digits into the mid-teens. It expects to get there by taking greater control of its investment projects. Having greater operational control means it can use its expertise on getting better returns out of large, complex upstream and downstream assets. It also intends to focus its business around industry-leading assets, as management highlighted during its fourth-quarter earnings conference call.

XOM Return on Capital Employed (TTM) data by YCharts.

Although Exxon's 2025 goal of doubling earnings is still a ways off, early results from the plan suggest that now is the time to buy this high-yielding energy name. Eventually Wall Street will realize that the giant company has started to turn the ship.

2. Strong enough to handle the transition

Next up is Tanger, a real estate investment trust (REIT) that owns 44 factory outlet centers and sports a heady 6.2% dividend yield. Being in the retail sector is rough today, as investor preferences appear to be in a state of flux driven by online shopping -- what the media has hyperbolically called the "retail apocalypse."

That's overkill, even though the shift in shopping habits is very real. To put it simply, people will still shop at physical stores in the future, and it's worth noting that a large number of once online-only retailers have begun to open brick-and-mortar locations. What's really going on is that older, out-of-favor concepts are going away and new ones are stepping in to replace them.

That's not a smooth process or one that happens quickly. So retail landlords like Tanger end up muddling through the transition, as they deal with bankruptcies and store closures. It can be tough, with lesser-quality enclosed malls taking the biggest hit and, frequently, shutting under the strain. But Tanger is different because it owns outlet centers, which are relatively cheap to operate, a low-cost option for lessees, and fairly easy to fill with replacement tenants. It just takes time.

SKT Dividend Yield (TTM) data by YCharts.

And Tanger is financially strong enough to get through this transition in one piece. For example, total debt to adjusted total assets is roughly 50%, a reasonable figure for a property-owning company. Meanwhile, it covers interest expenses by roughly 5 times. Tanger is not at risk of going bankrupt. Its dividend, meanwhile, only eats up around 60% of its funds from operations (FFO -- a key performance metric in the REIT space). Not only does that mean the dividend appears very secure, but it also leaves plenty of cash for other purposes, like replacing tenants.

What's most interesting about Tanger right now, however, is its current valuation. Although it stacks up nicely against industry bellwether Simon Property Group, Tanger trades at around nine times its projected 2018 FFO versus Simon's 15 times trailing 2018 FFO. Simon's yield, meanwhile, is a relatively meager 4.4%.

Rock-solid Tanger is built to survive headwinds like the retail apocalypse. When its portfolio repositioning starts to gain more steam, investors will likely reward it with a higher price. If you can look past the dire retail headlines here, now is a great time to pick up this high-yield stock.

3. A bit more risk, but over 100 years of history

The last name in this trio is General Mills, which is offering investors a robust 4.4% yield today. Like Exxon, the yield here hasn't been this high since the 1990s. But there's a key factor to keep in mind: General Mills has been providing customers with packaged foods for more than a century, owning household names like Cheerios, Yoplait, and Betty Crocker. While customer preferences have shifted toward food perceived to be fresher and healthier, dealing with changing tastes isn't new to General Mills.

GIS Dividend Yield (TTM) data by YCharts.

To adjust along with the current industry shift, General Mills has been selling older brands (like Green Giant) and buying ones that are more on target with current customers (such as Annie's, Larabar, and Blue Buffalo pet food). It is also updating the products in its current lineup to better meet customer tastes. Once again, it will just take some time for the packaged-food giant to work through the transition.

That said, there is one troubling issue here: debt. Unlike Exxon and Tanger, General Mills has leveraged up to fund acquisitions, most notably the recent Blue Buffalo purchase. Long-term debt is nearly 70% above where it was before the deal was consummated in 2018 and makes up nearly two-thirds of the capital structure. Although interest coverage is still solid, at roughly 4.1 times in the fiscal second quarter, that's down from around 9 times a year ago. These are disconcerting numbers, to be sure.

GIS Times Interest Earned (TTM) data by YCharts.

However, General Mills' leverage isn't outlandish for an industry that sells lots of small necessity products to lots of end customers. And, as noted, the increased leverage is driven by a portfolio overhaul. It's expensive, but buying and selling brands like this isn't new for General Mills. With debt levels already starting to drop (over the last two quarters, the company has reduced debt by over $450 million), investors with a modest tolerance for uncertainty should consider buying this stock now before the deleveraging process starts to gain steam and investors reward the stock with a higher valuation.

Grab these yields while you can

Exxon, Tanger, and General Mills are all companies in transition. That has investors worried, which has depressed the stocks and lifted their yields. If you can look past the near-term concerns to a future in which the transitions are further along, now is a great time to jump aboard.

Check out the latest Exxon, Tanger, and General Mills earnings call transcripts.

Financially strong Exxon is probably the least risky option here, appropriate for most investors. Tanger also has a strong balance sheet and a bright future, but the hype surrounding the retail apocalypse is pretty intense. You'll need a strong enough constitution to deal with (or perhaps ignore) the dire retail headlines. General Mills, meanwhile, is the riskiest of the trio largely because of its somewhat aggressive use of leverage. If you can afford the time and effort to monitor its balance sheet, however, taking on the current uncertainty is likely to be well rewarded.