November is a great time to take a long, hard look at your investment portfolio. If you have stocks that have performed poorly and you no longer have confidence about their long-term prospects, selling them before the year is over potentially allows you to harvest the losses for a tax benefit. It also frees up cash to invest in other stocks with a greater potential for delivering great returns.

We asked five Motley Fool contributors which top stocks they think are great picks for investors to buy in November. Here's why they chose Bookings Holdings (BKNG 0.84%), Cleveland-Cliffs (CLF +1.79%), MediPharm Labs (MEDIF 3.48%), MongoDB (MDB 2.55%), and The Trade Desk (TTD +0.22%).

Image source: Getty Images.

Around the world with one stock

Dan Caplinger (Booking Holdings): Travel around the globe has expanded dramatically in recent decades, with a rising consumer class in many emerging markets adding new travelers to the market at a breakneck pace. Moreover, the success of airlines over the past decade has helped to spur greater capacity to allow people to go where they want more conveniently. Meanwhile, the rise of the internet has forever changed the way people do commerce, and allowing people to arrange for travel online has become a fast-growing business.

Booking Holdings is at the intersection of the travel and e-commerce trends. As the leading online travel website, Booking has put together a strong combination of businesses under a single corporate roof. Starting with its Priceline "name your own price" travel website, Booking has made acquisitions like international hotel specialist Booking.com, online travel website aggregator tool KAYAK, and restaurant reservation service OpenTable. Booking.com was arguably the most important acquisition the company made, and that led it to change its name from Priceline Group to Booking Holdings in 2018.

Growth at Booking has slowed recently, worrying some who follow the online travel giant. Much of the drop in revenue growth has come from the strong U.S. dollar, to which Booking is particularly susceptible because of its extensive international business and exposure to foreign currency movements.

However, the company still has ambitious plans to expand. China has been a big target for Booking's growth, as it's made substantial investments in companies such as online travel platform Ctrip.com International, food delivery app provider Meituan Dianping, and ride-hailing specialist Didi Chuxing. China's economy has slowed recently, but its growth is still considerably faster than you'll find in many other parts of the world, and the nation's huge population makes it too fertile a source of potential business for Booking to ignore. Moreover, a strong presence in China would give Booking a base from which to capitalize on other opportunities across Asia.

Early in November, Booking Holdings will give investors its latest reading on how it's doing financially. Those watching the stock expect the online travel giant to post earnings growth of around 18% for the key late-summer season, with revenue gains of roughly 6%. Shareholders will want to keep an eye on the key metric of room nights booked, as Booking gave guidance three months ago that third-quarter growth in that category would come in around 6% to 8%.

Historically, Booking has done a good job of surpassing the guidance it's given investors, and that's why now's a good time to take a look at the stock. The online travel industry has a lot of tailwinds that should help it grow around the globe, and Booking's already extensive international presence makes it the most likely company to reap the rewards as more people around the world discover the joys of travel.

It may be a bad time for iron ore, but it's a great time for Cleveland-Cliffs

Tyler Crowe (Cleveland-Cliffs): I'm well aware that it sounds insane to suggest that an iron ore miner on the verge of bankruptcy a few years ago is a great stock to buy now. Yet as much as the specter of an impending recession and global trade slowdown looms large over commodities, there is a compelling reason to think that U.S.-based iron ore producer Cleveland-Cliffs is a great stock to own right now.

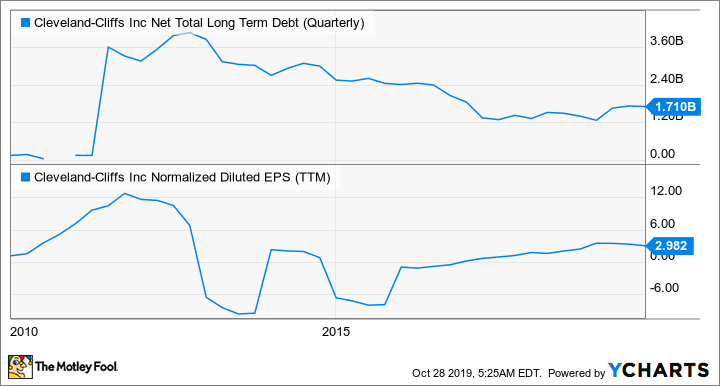

Much of the investment thesis in Cleveland-Cliffs comes down to its management team that took a bloated and unprofitable business and turned it into a resilient cash-generating operation in a matter of three years. The company has reduced its total debt outstanding by more than half from its peak in 2013, it has started to invest in new growth businesses, it has restored its dividend, and it's had the financial flexibility to buy back $250 million in shares so far this year.

CLF Net Total Long Term Debt (Quarterly) data by YCharts

Despite the monumental changes Cleveland-Cliffs management has implemented over the past few years, the company's stock still trades as though the company is in deep financial distress. Shares trade at 2.5 times earnings, and current prices aren't that far off where they were when the company was discussing Chapter 11 bankruptcy proceedings.

I don't have any deep insight into where iron ore prices are going from here. Fortunately, little of the investment thesis in Cleveland-Cliffs has to do with the future of iron ore prices. The iron ore market is much more nuanced than the spot price of iron ore pellets, and there are some inherent advantages to owning more than 55% of the U.S. iron ore market. What's more, this management team has seen this company through a lot more than just weak iron ore prices. With shares trading at such a low valuation, Cleveland-Cliffs looks like a great value stock today.

This high-growth small-cap stock will have investors seeing green

Sean Williams (MediPharm Labs): Over the past seven months, you probably couldn't dream up a more nightmarish investment than cannabis stocks. And while many still have a lot of growing up to do, one niche marijuana middleman is already profitable and de-risked from a lot of the supply issues plaguing the Canadian landscape. Say hello to extraction-services provider MediPharm Labs.

Extraction companies like MediPharm take cannabis and hemp biomass and, based on the scope of contracts signed with their clients, provide resins, distillates, concentrates, and/or targeted cannabinoids. These are also businesses that may offer white-label manufacturing and packaging services.

What makes extraction providers so exciting is that Canada, which became the first industrialized country to legalize recreational marijuana in October 2018, officially legalized derivative pot products on Oct. 17, 2019. Derivatives are products such as edibles, vapes, cannabis-infused beverages, concentrates, and topicals, and they'll begin appearing in Canadian dispensaries by mid-December. Because derivatives offer considerably better margins than traditional dried cannabis flower, these alternative consumption options are a must-have for all Canadian pot growers.

But here's the thing: Not every marijuana stock has the ability or the capacity to process cannabis or hemp on site. That's where MediPharm Labs comes into play. Its Barrie, Ontario, facility will soon be able to handle 300,000 kilos of annual processing capacity, with an eventual push to 500,000 kilos per year. Thus far, the most notable deal MediPharm has landed is with Cronos Group. In exchange for $30 million over an 18-month period, MediPharm is supplying Cronos with concentrates.

Aside from the fact that extraction-service providers like MediPharm are the go-to middlemen for pot stocks, the contracts these extraction companies sign are typically 18 to 36 months in length. Thus, they provide predictable cash flow over the intermediate term in a fast-growing yet nascent industry with little certainty.

Despite beginning operations last November, MediPharm already managed to report its first quarterly profit in the second quarter. As the company's expansion capacity ramps up, it should quickly and easily build on its profit momentum. Given the importance of derivative products over the long run for the cannabis industry, 22 times next year's earnings per share looks to be a veritable steal for MediPharm Labs.

A massive growth runway

Brian Feroldi (MongoDB): All businesses use data to make decisions, but raw data is useless unless it is captured, organized, and stored in an efficient and searchable database. This need has driven many of the largest companies on the planet to rely on database providers such as Oracle for decades.

But legacy databases are having a hard time keeping up with the needs of modern-day businesses, since we now capture huge amounts of data that can't be stuffed into neat columns and rows. Think photos, videos, and audio files. The rise of e-commerce and cloud computing is also putting a strain on traditional databases that they were never designed to handle.

These factors are causing enterprises to seek out alternative solutions like never before, and MongoDB is seizing the opportunity like no one else.

MongoDB built its database system from the ground up to solve all of the shortfalls of legacy solutions. MongoDB's software is open-source and free to download, and it can capture, store, and organize data in almost any type of format. The database is also distributed, which makes it easy to split it across lots of low-cost servers, eliminating the need to buy certain types of expensive hardware.

These benefits explain why more than 60 million developers have already downloaded MongoDB's software. That's wonderful news for investors, because MongoDB uses a "freemium" model to drive growth. Developers can easily download MongoDB's software and play with it until they become comfortable. However, they get only a limited amount of storage space. Unlocking more requires them to become paying subscribers.

MongoDB has the numbers to prove that its strategy is working brilliantly. Its customer count more than doubled to 15,000 in the most recent quarter. The company's net annual recurring revenue expansion rate, which tracks same-customer subscription revenue from between periods, has remained above 120% for more than four years in a row. That helped drive 67% revenue growth to $99.4 million in the most recent quarter.

These numbers are impressive, but the exciting part is that they're still small when compared with the company's true potential. The global database software market hauls in $64 billion in revenue each year and continues to grow. By contrast, MongoDB expects to generate less than $400 million in annual sales during the current fiscal year. That means it hasn't even captured 1% of its addressable market opportunity yet.

The biggest knock against investing in MongoDB is that it's still losing money -- its net loss was $37 million last quarter --and that its valuation is sky-high, with shares currently trading for more than 20 times trailing sales. Investors need to keep those risks in mind. But my view is that the company's growth opportunity is so massive that it still makes sense to take a small position today and add to it over time.

Those might sound like empty words, but I recently added MongoDB to my personal portfolio, so my money is where my mouth is.

Adding up

Keith Speights (The Trade Desk): I like stocks that are leaders in a fast-growing market that's in its infancy. The Trade Desk fits that bill perfectly.

This company provides a software platform for advertising agencies to buy ads from more than 500 billion digital opportunities every day. This software-based model is called programmatic advertising.

There's no question that The Trade Desk is a leader in the programmatic advertising market. AdExchanger named its platform the "Best Demand-Side Technology" earlier this year, while the ClickZ Marketing Technology Awards named The Trade Desk as "Best Demand Side Platform" for 2019.

The Trade Desk's opportunity is ginormous. The global advertising market should be close to $725 billion this year and is projected to grow to $1 trillion by the middle of the next decade. Programmatic advertising will probably total only $34 billion in 2019. But it should make up most of the market in the not-too-distant future, growing at a rate five times faster than the overall advertising market.

I especially like The Trade Desk's prospects in connected television (CTV), which includes streaming TV services that are ad-supported. The company signed a deal in August with Amazon.com that The Trade Desk CEO Jeff Green called "a game changer." Amazon will allow advertisers to place ads on apps that use the Amazon Fire TV platform through The Trade Desk and one other third-party platform.

My view is that the Amazon deal is only one of many opportunities that The Trade Desk will seize in CTV. As the digital and programming advertising market expands, The Trade Desk should be able to deliver sizzling growth for long-term investors.