Wall Street loves a story, often pushing stocks to extremes based on a mutually agreed-upon narrative. That feels great when the narrative is a positive one, but it can sting pretty badly when the story is negative. The thing is, mercurial investors often go too far on the upside and the downside as they extrapolate current trends into the future.

Today, that's holding back the stocks of ExxonMobil (XOM +0.63%), Simon Property Group (SPG +0.80%), and International Business Machines (IBM 0.82%). Each is dealing with headwinds that have them in the Wall Street dog house, but all are likely to survive the troubles and thrive again. Here's a quick rundown on each.

1. The energy revolution still has a ways to go

The big knock against Exxon is that it drills for oil, which is destined to be replaced by cleaner alternatives such as solar- and wind-generated electricity. To be fair, that's true -- but it likely won't happen for decades (or longer). The world still needs and wants oil today. However, investors don't care. Almost anything that has to do with oil is on the outs.

Image source: Getty Images.

That includes Exxon, which currently offers a yield of 5% -- near the highest levels in decades. Add in an industry-leading streak of 37 annual dividend increases, and there's even more for dividend investors to like here. Now consider that Exxon has one of the strongest balance sheets in its peer group, with a financial debt-to-equity ratio of just 0.15 times, which is actually a low figure for any company in any industry. Moreover, Exxon is investing in oil production and processing opportunities that it thinks are highly desirable and that will support results for years to come.

That last point is actually a piece of the problem. Exxon is set to spend as much as $35 billion a year through 2025, and oil prices are stuck in a relatively low range. That's putting pressure on profits and will likely require the oil giant to tap the capital markets and sell assets to fund these investments. Wall Street is concerned that Exxon can't afford the expense. But that's based on today's low oil prices, and Exxon has a habit of investing during industry weak spots so it can come out the other side a stronger company.

If you can get comfortable with the idea that it has the financial strength to see this investment plan through (and that oil is still an important energy source, even if it's out of favor today), then high-yielding Exxon stock might be a good fit for your portfolio.

2. The mall isn't dead

If you pay attention to the news at all, you've probably heard the hyperbolic rhetoric about the "retail apocalypse." From the hysteria, you'd think that inherently social human beings will only shop online in the future. That's far from the case, even though internet shopping is leading to changes in the way people view retail and the way they interact with malls. But investors don't do nuance well, and they have put mall real estate investment trusts (REITs) such as Simon Property Group on the sale rack.

XOM Dividend Yield (TTM) data by YCharts.

That's a shame, since Simon, which owns well-situated malls, has actually been holding up pretty well despite the store closures and bankruptcies that have been hitting mall owners. Take, for example, the REIT's 94.7% occupancy level and the fact that sales per square foot increased 4.5% in the third quarter. Meanwhile, the closure of anchor tenants has actually been a positive catalyst, allowing Simon to increase rents by 22% as it releases the vacated space (which generally had below-market rents). The mall owner is also building new retail assets overseas, which should support growth over the next few years.

Meanwhile, Simon has one of the strongest balance sheets in the industry. As of the third quarter, it had $7 billion in liquidity available via cash and a credit line. That should be plenty of money to support its efforts to shift along with consumer buying habits (which includes adding more experiential tenants to the mix to draw customers into its malls).

Yes, consumer buying habits are changing, and older, less desirable malls are probably going to end up closing. The malls Simon owns, though, are more likely to change with the times and continue to attract tenants and shoppers. If you can look past the hyperbole of the retail apocalypse, you might want to do a deep dive on Simon and its 5.5% yield today while Wall Street is tossing out the baby with the bathwater.

3. A tough transition

Technology giant IBM is struggling today. Sales have been falling for years, while earnings have been heavily supported by stock buybacks. That said, it just consummated a large acquisition that has left it with a heavy debt load and resulted in the suspension of stock buyback plans. Investors are not pleased and, perhaps, for good reason.

The thing is, this over 100-year-old company has been in similar spots before. What's really going on is that the technology industry has shifted to a new direction, and IBM is working to change its offerings to better match customer needs. It has done this several times before. This type of change, though, is never pretty.

Today, IBM is selling off lower-margin businesses (such as making computers) so it can focus on higher-margin operations (such as cloud computing and security). Every business it sells, though, pulls revenue from the top line (thus the years of declines). And the new businesses in which the company is investing are still developing, so they aren't making enough to offset what's been lost. That's a mismatch on the top line that IBM hopes to rectify soon.

"Soon" is a tough sell on Wall Street since the tech giant can't really give a specific date. And the longer it takes, the less investors are inclined to give Big Blue the benefit of the doubt. Add in the acquisition of Red Hat, which materially increased IBM's debt levels, and investors are getting more and more worried that the company has lost its way. This is why IBM stock currently yields 4.8%, near the highest levels in the company's history.

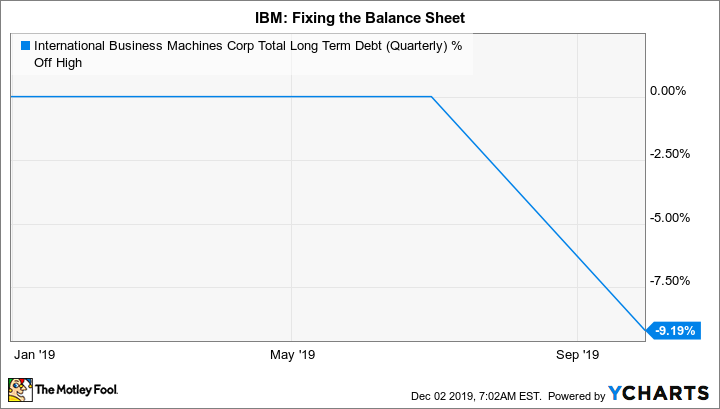

IBM Total Long Term Debt (Quarterly) data by YCharts.

That said, IBM is aware of the leverage concerns and has already reduced long-term debt by nearly 10% since the Red Hat deal closed. That's a testament to its still-robust cash flow. The Red Hat acquisition, meanwhile, gives it a valuable position in the cloud, allowing it to bridge in-house and public cloud environments as well as provide services to customers who use competing cloud providers. At this point, revenues from its new businesses are finally at about 50% of the top line and should start to have a greater impact on results as the Red Hat business starts to gain more traction. The transition is hardly over, but it looks like the trends will start to get better "soon."

To be fair, it has been a long and difficult transition, and investors are probably right to take a show-me attitude. But IBM still appears to be muddling through in OK form. That's hardly a sterling recommendation, of course, but with a nearly 5% yield, the risk/reward profile seems pretty attractive. Investors would do well to consider a deep dive while Wall Street is still in a doubting mood.

Out of step

With the market near all-time highs, it's not easy to find good deals on Wall Street. That means stepping into stocks that are out of favor for some reason. IBM, Simon, and Exxon all fall into that category. However, they all appear to be doing pretty well despite the currently negative view of their businesses. You need to do your homework on each name, of course, but you may decide that Wall Street has given up on these stocks just a little too soon. And you can collect fat dividends while you wait for investors to realize that things may not be as bad as they seem.