Healthcare stocks have lagged behind the overall market so far in 2019. Don't expect that to be the new normal, though. Over the long run, healthcare stocks hold the potential to deliver market-beating returns thanks to aging demographic trends.

Which healthcare stocks are good picks for investors to buy in December? Here's why Intuitive Surgical (ISRG 0.71%), Teladoc Health (TDOC 6.04%), and Vertex Pharmaceuticals (VRTX 0.55%) rank near the top of the list.

Image source: Getty Images.

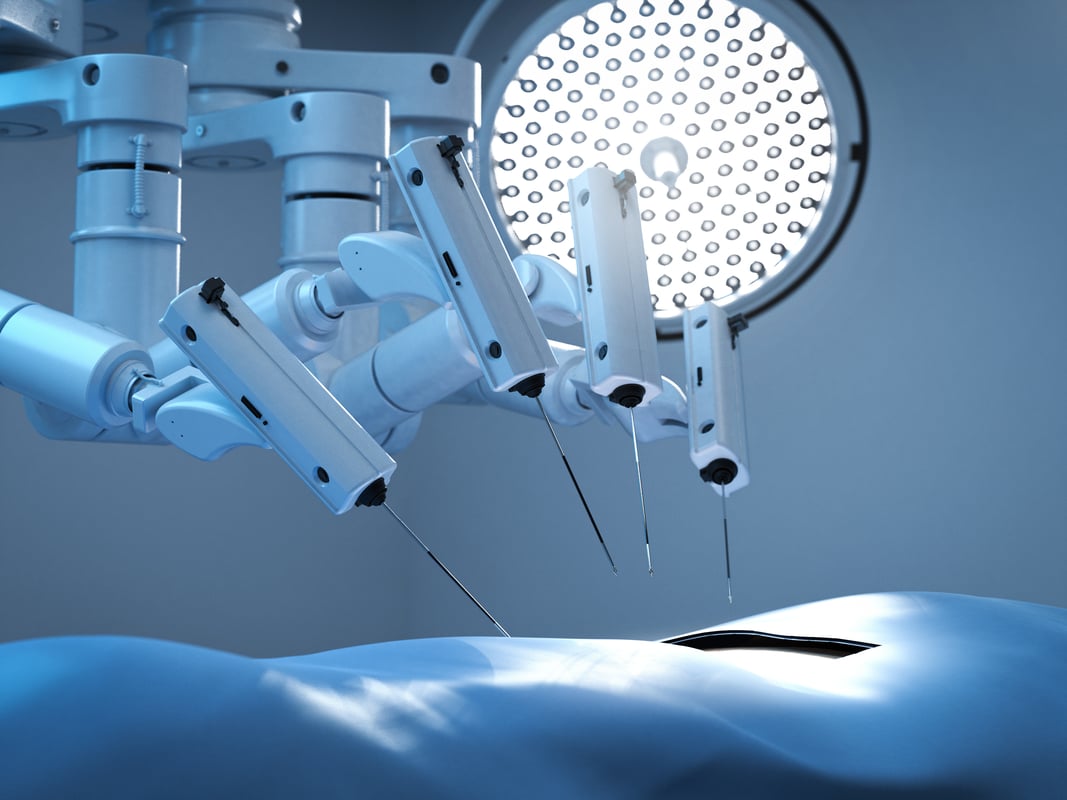

1. Intuitive Surgical

Intuitive Surgical absolutely dominates the robotic surgical systems market. The company's da Vinci systems have been used in over 6 million surgical procedures. More than 5,400 da Vinci robotic surgical systems are installed across the world.

Even though it's been in business for over two decades, Intuitive Surgical is still growing rapidly. The company reported third-quarter revenue of nearly $1.13 billion, up 23% year over year. Worldwide procedures using da Vinci jumped nearly 20%.

More growth should be on the way. The more systems Intuitive ships, the more its recurring revenue from replacement instruments, accessories, and services increases. The company already makes over 70% of its total revenue from recurring sources. Intuitive shipped 275 da Vinci systems in Q3 -- up 19% year over year -- so look for even higher recurring revenue in the near future. It also continues to launch new products, including enhancements for da Vinci and its new Ion system for lung biopsy.

Intuitive Surgical faces the prospects of increased competition, with Medtronic introducing its new robotic surgical system and Johnson & Johnson expanding its presence in the market. However, I think this competition actually presents a compelling reason to expect higher growth from Intuitive as new market entrants further validate the use of robotically assisted surgery.

2. Teladoc Health

Some call it telehealth. Others call it telemedicine or virtual care. Whatever the name you use, the delivery of healthcare services remotely using internet technology is hot. And Teladoc Health stands as the market leader, with over 40% of the Fortune 500 companies using its services.

Teladoc's growth remains very strong. The company posted revenue of nearly $138 million in the third quarter, a 24% year-over-year increase. And that excluded the impact of Teladoc's acquisition of French telemedicine provider MedecinDirect.

The appeal for telehealth services should increase in the future. Expanding older populations will drive higher demand for healthcare services. Employers, payers, and government health programs will look for ways to control costs, with telehealth providing a great option for doing so. Teladoc's scope of services and global footprint should position the company to benefit tremendously from these trends.

However, there are some drawbacks to investing in Teladoc Health. It's not profitable yet. The stock isn't cheap. Teladoc could also face more competition as big companies like Amazon.com eye the telehealth market. But I think Teladoc's growth prospects outweigh any of these concerns.

3. Vertex Pharmaceuticals

Vertex Pharmaceuticals markets four drugs that treat the underlying genetic cause of cystic fibrosis (CF). At this point, the biotech enjoys a monopoly in the CF market and should dominate the market for a long time to come.

The company reported Q3 revenue of $950 million, up 21% year over year. But that revenue didn't include sales for its latest approved drug, Trikafta. Vertex expects the new drug to enable it to boost the addressable patient population for its therapies by more than 50% as Trikafta gains additional regulatory approvals in Europe.

Vertex's CF revenue will soar over the next few years thanks to Trikafta and the company securing key reimbursements recently in multiple countries. The biotech also hopes to move beyond CF. Its pipeline includes several programs targeting rare genetic diseases plus not-so-rare indications such as pain and type 1 diabetes.

The stock might look expensive with shares trading at 33 times expected earnings. However, I think Vertex is worth the premium price tag with its excellent growth prospects in CF and multiple shots on goal in treating other indications. I continue to view Vertex as the best biotech stock on the market.