Last year was a big one for Netflix (NFLX +1.88%). The company finished 2020 with just shy of 204 million global subscribers, 37 million more than a year ago, as consumers stuck at home looked for ways to pass the time during the pandemic turned to the streaming service for assistance. And thanks in no small part to a pause in new content production during the lockdown last spring, Netflix also reported a big increase in profitability. Some of this profitable progress is bound to take a step back again in 2021, though, as spending on content ramps back up.

Despite the mostly good news for this company, given the streaming leader's business model, I still can't get super excited about making a purchase of its stock for my portfolio.

Netflix is the early bird that caught the streaming TV worm

Back in 2012, Netflix entered the competitive media industry fray as a producer of content. It started really ramping up its original content efforts in 2014 and used this exclusive library of new content to quickly acquire subscribers in both the U.S. and abroad.

Image source: Getty Images.

It was a great long-term move as it has helped the company maintain a sizable subscriber lead among internet-based TV platforms, even as potential competitors like Disney (DIS +0.56%) began supercharging their efforts in next-gen entertainment by doing things like launching Disney+ and gaining control of Hulu. When it comes to streaming, Netflix gets credit as the early bird that caught the worm.

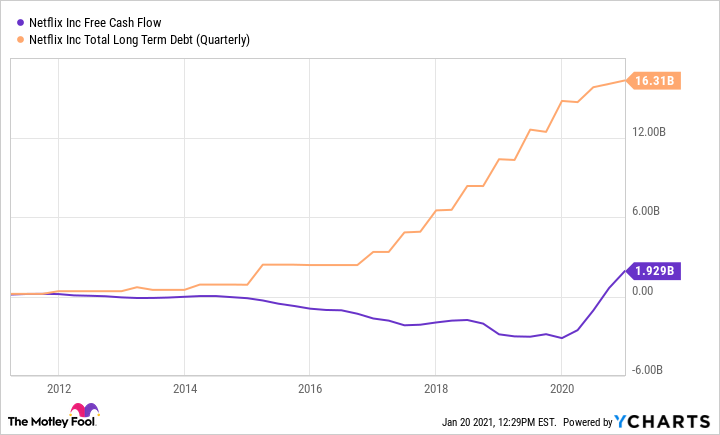

Nevertheless, I was never comfortable with Netflix's decision to get heavily into content production. It's an expensive endeavor, and it relies almost entirely on a growing subscriber base to pay for that new content. "Legacy" media companies like Disney have always utilized the global box office to make sizable revenue upfront from theater ticket sales, and then continuously monetize movies over time by selling broadcast rights to distributors and various networks. Since Netflix doesn't have the same vertically integrated business model with the ability to monetize content to the same extent, it made up the difference between subscription income, and content creation and distribution costs by tapping the debt markets.

Data by YCharts.

However, the vertically integrated business model advantage that media companies had broke in 2020 because of COVID-19. At-home entertainment like Netflix suddenly had an advantage, and it's still unclear what the fate of movie theater chains will be. And because TV and movie production came to a standstill last spring (and thus spending to support production also froze), Netflix went from a loss-generating company to a profitable one (using free cash flow and revenue minus cash operating expenses and capital expenditures). However, as content spending has come back online, Netflix is back in the red. During the final quarter of 2020, free cash flow was negative $284 million.

Another media company could get the cheese

Netflix did say it expects to reach free-cash-flow breakeven in 2021. For a company like this that has been prioritizing growth for years, turning the corner on profitability is an important milestone -- one that can keep sending a stock higher for a long time.

But Netflix is a conundrum to me. Rather than reinvest the cash it expects to begin generating like other high-growth companies might after they turn this corner, Netflix intends to start paying down debt and will possibly initiate a share buyback program. Talk of such actions, before it has even reached sustainable free-cash-flow-positive territory, would indicate this is already a much more mature business model (rather than a young, high-growth one) than it gets credit for.

Which brings me to my point: Certain "legacy" media companies might be a better buy here. I'm talking specifically about Disney. It's already free-cash-flow positive, even though it, too is investing heavily in currently loss-generating streaming services and its theater and theme park businesses are operating on a limited basis at best right now. For a longer-term growth play, I think Disney is the way to go, not to mention the potential rebound potential it has once travel starts to loosen up as effects of the pandemic ease.

Data by YCharts.

Don't get me wrong; I don't fault anyone for owning Netflix. It continues to add subscribers in international markets at a healthy pace, and reaching sustainable positive free cash flow will be a big deal. But Netflix lacks the vertically integrated and highly profitable business model that Disney has, and I'm not seeing any "next plans" for the cash it expects to begin generating. As long as the never-ending game of content creation without any additional profit-generating potential (outside of subscribers) is the game here, I just can't see Netflix being all that lucrative of a streaming media platform. Netflix is the streaming pioneer, but Disney is the second mouse that could get the cheese.