Telecommunications stocks have some of the highest dividend yields on the market, but they can't seem to get much traction in growing their stock price. Verizon Communications (VZ -0.82%) has been stuck in a rut for years, AT&T (T -0.37%) is in the same boat after a number of strategic missteps, and the only stock that seems to be appreciating is T-Mobile US (TMUS -10.79%) after its merger with Sprint.

As unloved as these stocks are, there might still be an opportunity for long-term investors. 5G networks that are being rolled out nationwide open up new markets into homes and businesses and could provide an avenue for growth. These opportunities are why I think Verizon is both a great dividend stock and an underappreciated growth stock in the long term.

Image source: Getty Images.

The foundation

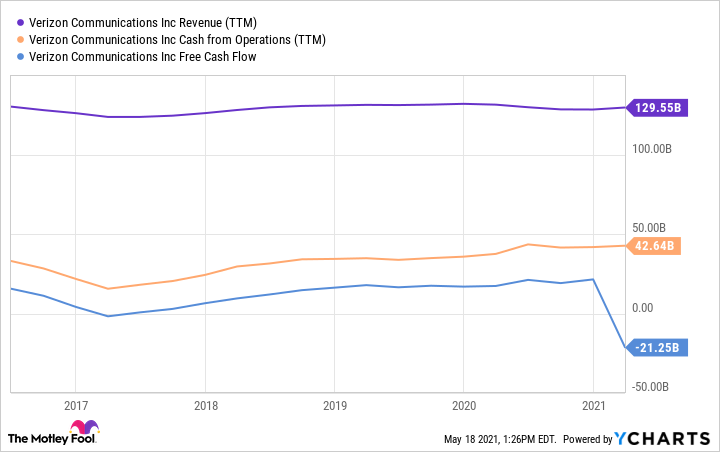

Before looking at Verizon's growth opportunities, let's consider the foundation on which it's building. You can see in the chart below that Verizon's revenue has been steady for years and operating cash flow has been improving. Free cash flow has been strong until the first quarter, when the company spent $45 billion on spectrum licenses.

VZ revenue (TTM) data by YCharts. TTM = trailing 12 months.

Compare this to T-Mobile, which is definitely growing faster than Verizon, but is also generating negative free cash flow each year.

TMUS revenue (TTM) data by YCharts.

Above, you're starting to see the trade-off companies are making. T-Mobile has priced its plans aggressively on the assumption that it can attract users, which it has done. But that's come at the expense of cash flow. Verizon has kept prices higher and is banking on a superior network keeping enough customers to remain profitable and eventually invest in a next-generation network that will attract even more customers. The cash flow advantage is why Verizon could spend $45 billion on wireless spectrum in the most recent auction. It may have been backed into a corner somewhat, but it has the funds and cash flow to outbid rivals to build the next-generation network it needs to grow.

Setting up for growth

The chart above isn't very inspirational from a growth standpoint, but if we look at what Verizon has coming down the pipeline, it could be a better growth stock than investors are thinking. Adding more smartphone connections isn't where the best opportunities lie, although there may be an opportunity there and with connected devices, but adding home internet could be a big deal for Verizon long term.

Verizon has already said that C-band and millimeter wave (mmWave) spectrum will make up the 5G networks that will allow it to offer home and business wireless internet. And management said that 15 million households will be within reach of 4G and 5G fixed wireless by the end of this year, with 50 million households within coverage range of 5G by the end of 2025.

This is essentially a new market for Verizon, replacing the wired connections that cable, DSL, and even fiber have been making to homes and businesses. If Verizon can bundle smartphone connections with fixed wireless connections, it could expand its revenue opportunity by billions of dollars each year.

On top of the obvious addition of fixed wireless, building a great 5G network will allow for connected cities, smart devices, autonomous vehicles, edge computing in virtual and augmented reality, and other innovations. These are all options for growth that may or may not materialize but give Verizon further upside.

Verizon is priced right for investors

Despite all of the growth options I highlighted above, Verizon is trading more like a value stock. Shares trade for just 12.5 times earnings and have a 4.3% dividend yield, which is great for a dividend stock.

This is why I'm excited about the possibility to add fixed wireless internet to the portfolio, which will give millions of people a better option than their current broadband internet. And if the narrative around Verizon changes even a little, it could generate great returns for the next decade.