The pandemic definitely benefited e-commerce companies, but the digitization of retail sales was already a long-term trend. With many e-commerce stocks soaring in 2020, many have been also-rans in 2021 as the market has generally turned to reopening and cyclical stocks.

However, after some malaise, e-commerce stocks could be in for another good period this fall. Unfortunately, some of that is due to the delta variant, which is more contagious and leading to more breakthrough cases of COVID-19. But some of it is also due to new habits developed during the pandemic, and stepped-up capabilities of e-commerce players more broadly.

In that light, here are three e-commerce stocks that look like great buys heading into the end of the year.

Image source: Getty Images.

Amazon

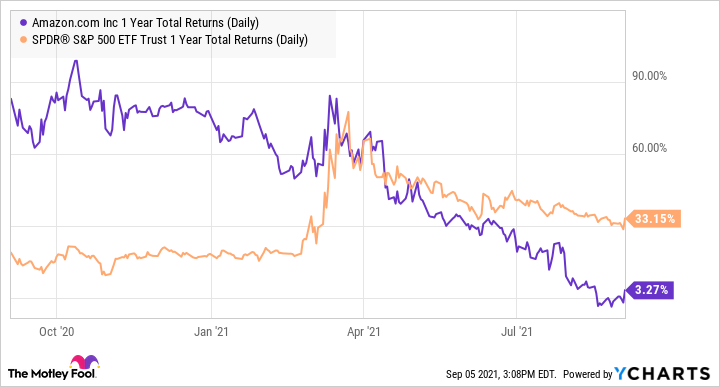

Although it outperformed handily in the opening months of the pandemic, over the past 12 months, Amazon's (AMZN -0.33%) stock has badly lagged the S&P 500, to the tune of about 30 percentage points!

AMZN 1 year total returns (daily) data by YCharts.

That's a long period for the world's largest e-commerce company to underperform, especially since its operating results have generally been solid. Yet while many investors might be used to analyzing Amazon in relation to its main e-commerce segment, which accounts for a majority of sales, it also has some key high-profit segments that benefit from the economic reopening.

In fact, two of its highest-margin segments, Amazon Web Services (AWS) and digital advertising, should do better as the economy reopens and businesses buy more cloud services and ads. In fact, while e-commerce sales decelerated last quarter, those two segments accelerated. AWS was up 37%, accelerating from 29% in the year-ago quarter, while the company's "other" category, which is mostly digital ads, accelerated 83%, up from 41% growth a year ago.

Though accounting for just 13% of sales, AWS generated over half of Amazon's operating profit last quarter. Digital ads are likely high-profit, too, though management doesn't disclose that segment's stand-alone margins. In fact, these two segments, if they continue their strong performance, could almost account for all of Amazon's current valuation, meaning investors are practically getting the core e-commerce business for free.

But of course, investors shouldn't discount the core e-commerce business, either, which should become even more efficient. In August, Amazon completed its new state-of-the-art Amazon Air Hub at the Cincinnati/Northern Kentucky International Airport, which will serve as a high-throughput hub for its national delivery network. Operations just started after four years of planning and construction, so the company looks poised to benefit from even faster and more efficient delivery, which could help sales and profitability.

In any case, Amazon's stock usually doesn't stay dormant for that long. Now may be a good time to add to or reenter this long-term winner.

Sea Limited

In contrast to Amazon, the stock of Singapore's Sea Limited (SE +4.39%) has been positively booming. After nearly quintupling in 2020, the stock has gone up another 77% in 2021, just for good measure.

However, just because the stock has been on a huge tear doesn't mean you've missed out on further gains. The company's big success in 2020 could be due to the rapid adoption of e-commerce in Sea's home markets of Southeast Asia, where the internet and e-commerce have been much less developed than in the U.S or China prior to the pandemic.

Image source: Getty Images.

But it wasn't just a "right time, right place" phenomenon; Sea has figured out how to beat established competitors to become the leading e-commerce platform across the region, despite being a late entrant. It has the added benefit of its highly profitable video game division called Garena, anchored by the massive hit Free Fire. Not only does the gaming division give the company the cash flow needed to invest in its money-losing but hypergrowth Shopee e-commerce platform, but the popularity of Free Fire also gives Shopee a quick and efficient way to acquire customers.

With Free Fire the highest-grossing mobile game not only in Southeast Asia but also Latin America and India, Sea is now launching Shopee in those regions as well, which likely explains the further gains this year. It first landed in Latin America in Brazil in 2019, but reached a milestone of becoming the most-downloaded app in the shopping category in the country last quarter, and also garnering the most time spent on its app. Shopee was second in terms of monthly users.

In addition to further landfalls in Chile, Colombia, and Mexico this year, Shopee also looks to be setting up operations in India. The country already has established e-commerce companies, but with 1.3 billion people, it has lots of market growth there for the taking. I wouldn't be surprised to see Shopee succeed over the long term in Latin America and India, even if it has to settle for a strong second place to the first-movers there. Both new markets appear big enough to power Sea to a $1 trillion market cap over the long run, should management continue to execute the way it has in the past.

JD.com

Finally, for those looking to go bargain-hunting, JD.com (JD +2.52%), like many Chinese stocks, is down significantly from its highs. The Communist Party's ongoing crackdown on China's tech sector has caused widespread selling across large tech names since the spring.

While the speed and ferocity of the new regulations have caused some investors to panic, new regulations could in fact help some companies more than it hurts. One such company is e-commerce giant JD.com, which, despite a recent bounce, is still down more than 25% off its all-time high set back in February.

Why might JD.com be a net beneficiary of new regulations? Mainly because new regulations are more likely to hurt its competitors, so JD could be a relative winner in the minds of Chinese consumers. For instance, in April, rival Alibaba was fined $2.8 billion for violating anti-monopoly regulations regarding the practice of "pick one of two," in which Alibaba would force brands into exclusivity contracts for access to its platform. With the practice now forbidden, JD can have access to certain brands it couldn't before.

In their new draft rules, regulators also sought to limit or forbid the use of aggressive subsidies, or pricing items below cost in order to drive engagement and traffic. That's been a tactic of group-buying upstart Pinduoduo, whose meteoric rise to become a top e-commerce platform was at least partly due to generous subsidies.

JD is by no means immune from regulations; in fact, in response to concerns over delivery workers' wages and rights, it just formed a union last week. However, the company has always had its own delivery infrastructure and in-house delivery employees. That has been more expensive relative to other e-commerce platforms that offload delivery to third parties. But now that exclusivity and cost subsidies are to be taken away, speedy, efficient delivery could be a main differentiator. Given its heavy past investments at the expense of profits, JD may now be in a better position than rivals.

One point of evidence is that while Alibaba missed revenue expectations last quarter, JD handily beat its analysts' expectations on both the top and bottom lines, showing little impact from Beijing's crackdown. ARK Investments' Cathie Wood has been buying the stock for her portfolio after mostly exiting Chinese stocks earlier this year. That could be a sign investors are starting to decipher winners and losers in the future Chinese regulatory regime. JD looks to be the former.