Artificial intelligence (AI) has whipped investors into a frenzy in 2023, and it has driven shares of semiconductor giant Nvidia (NVDA 1.97%) to a whopping 209% gain for the year. But while Nvidia is the most dominant player in the AI segment of the chip industry, it's certainly not the only one.

Investors have been watching Advanced Micro Devices (AMD 1.03%) closely, because its new MI300 AI chip set appears capable of competing with Nvidia's hardware. But AMD won't be shipping the MI300 until later this year, and investors have now endured two consecutive quarters of revenue declines while they wait.

While Nvidia stock is trading near the best levels in its history, AMD stock remains 29% below its all-time high. But that might be an opportunity for investors ahead of what could be a much stronger second half of 2023. Here's why.

NASDAQ: AMD

Key Data Points

The MI300 could be a game-changer for AMD

Many years ago, businesses used to store their data on their physical premises. Today, cloud providers like Amazon Web Services build and manage enormous data centers that businesses can rent for a fraction of the cost instead. The cloud has evolved to facilitate many commercial activities from software development to video streaming to training AI models.

AI has become a key point of focus for cloud providers, because companies are demanding AI tools to help improve their productivity. As a result, those cloud providers need the most advanced semiconductor hardware inside their data centers to maximize computing power.

That's where Nvidia has found success; its A100 and H100 data center chips are designed for AI workloads, and they're the most powerful in the industry. Nvidia CEO Jensen Huang says there is $1 trillion worth of existing data center infrastructure that needs upgrading to support accelerated computing and AI -- naturally, AMD wants a slice of that gigantic pie.

AMD's new MI300 comes in two configurations. The MI300A is a 3D stacked package combining processors (CPUs) and graphics chips (GPUs) to create what AMD says is the world's first advanced processing unit (APU) for data centers. It's already the product of choice for the new El Capitan supercomputer at the Lawrence Livermore National Laboratory.

It's expected to be more powerful than the current top 200 supercomputers combined. If all 7.7 billion people on Earth completed one calculation per second, it would collectively take them eight years to do what El Capitan can do in one second.

Then there's the MI300X, which is a GPU-only chip designed for training large language models. It also comes in the AMD Instinct configuration, which stacks eight MI300X chips into an industry-standard format capable of plugging directly into existing data center infrastructure. This could help drive adoption by cost-conscious cloud providers, which would increase AMD's market share.

AMD is coming off another shaky quarter

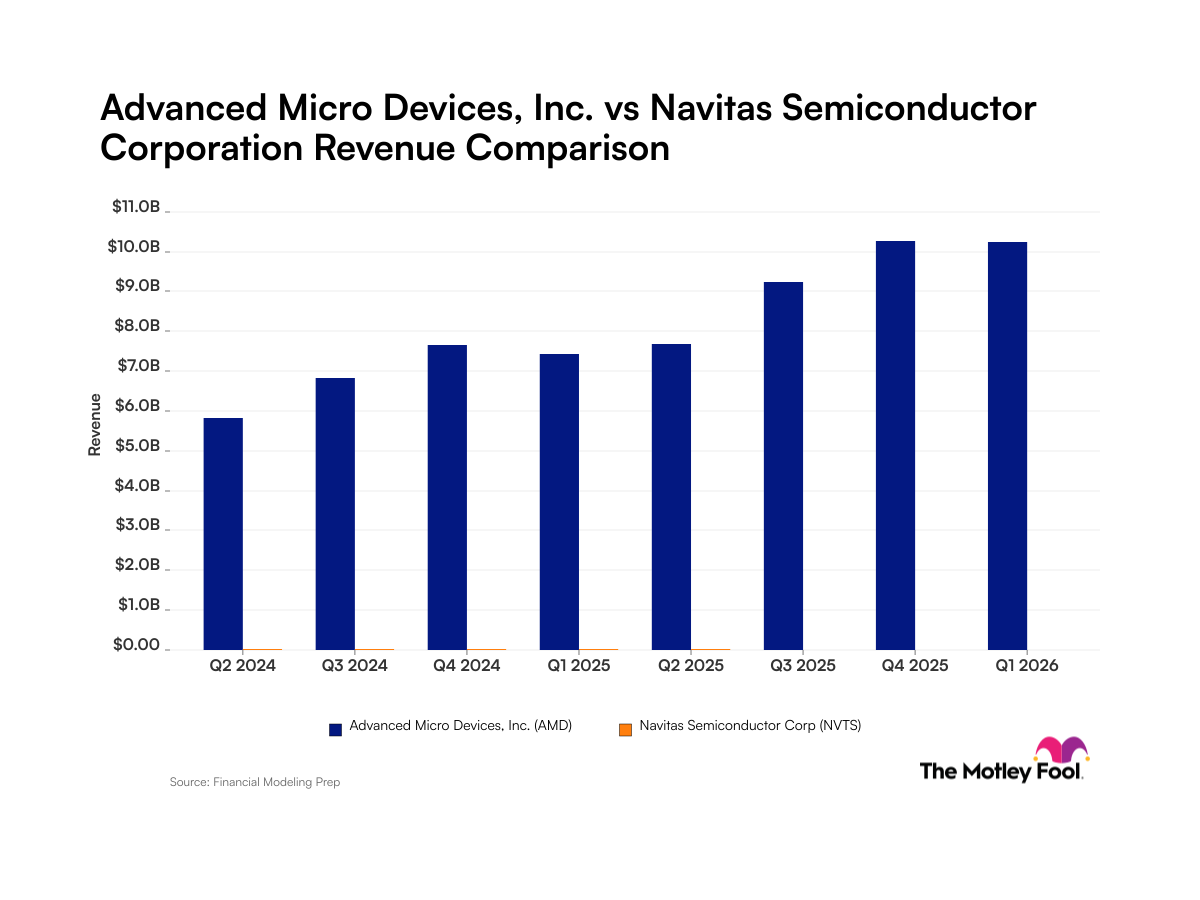

While Nvidia has delivered spectacular growth so far this year, AMD has reported two consecutive quarters of year-over-year revenue declines. Its consumer segments are the main drag, because people are simply buying fewer computers and gaming products in this tough economic environment.

But AMD also saw a decline in its data center revenue in Q2, which has previously been a growth engine for the company. Within that segment, CEO Lisa Su told investors that adoption of AMD's new fourth generation data center CPU for cloud instances accelerated, with revenue nearly doubling sequentially. Unfortunately, it wasn't enough to drive the business to year-over-year growth.

Data source: Advanced Micro Devices. Infographic by The Motley Fool.

Su does expect the second half of 2023 to deliver powerful growth of about 50% in the data center segment, likely thanks to shipments of the MI300 that are due to begin in the fourth quarter. She also told investors engagements with top-tier cloud providers, large enterprises, and leading AI companies soared by more than seven times in Q2, which hints at strong product sales later this year.

AMD stock is a great value ahead of MI300 sales

As I touched on earlier, Nvidia has a firm grip on the AI chip space with an estimated 90% market share. Thanks to its surging stock price this year, the company is valued at $1.1 trillion right now, and analysts expect it to deliver $43 billion in revenue for fiscal 2024 (ending Jan. 31, 2024).

AMD is Nvidia's primary threat, and since it's coming off a low base in terms of market share, it has everything to gain. Wall Street expects AMD to deliver $20.9 billion in revenue in 2023, which is about half of Nvidia's revenue, yet AMD stock is valued at less than one-fifth ($176 billion) of Nvidia.

There's no exact science that says the valuation gap needs to close, but it does suggest investors aren't giving AMD much credit for its potential to eat away at Nvidia's advantage. Nvidia did produce substantial growth in its most recent quarter, which is one reason investors might be pricing its stock at a big premium.

But since AMD stock is down 29% from its all-time high, it's also trading at a relatively cheap level compared to its own historical valuation. It traded at a price-to-sales ratio of 11.4 in 2020 and 10.7 in 2021, but it's sitting at around 7.6 today. If the company's revenue accelerates in the second half of 2023 as Su suggests, that valuation will look even better by the end of the year.

The long term is even more exciting because Su predicts the market for AI chips could grow at a compound annual rate of 50% going forward, and she says AMD could take a sizable portion of what could be a $150 billion opportunity by 2027. As a result, the last two sluggish quarters and subsequent weakness in AMD stock could present a fantastic opportunity to buy for the long run.