Taiwan Semiconductor Manufacturing (TSM 1.60%) has been at the center of the artificial intelligence (AI) chip boom by virtue of its status as the world's largest semiconductor foundry. The company, commonly known as TSMC, reported second quarter results on July 17, only to remind the market why it is one of the best ways to capitalize on the growth in AI semiconductor demand.

All the major chip companies, such as Broadcom, Marvell, Nvidia, AMD, and Intel, have been using TSMC's fabrication plants to manufacture their AI chips. Moreover, the chips that go into AI-enabled smartphones are manufactured at TSMC's facilities since it counts the likes of Qualcomm and Apple as customers too.

This world-class client base and the secular growth of the AI chip market allowed TSMC to deliver outstanding Q2 results and boost its full-year guidance as well. Take a closer look at the latest numbers, and you'll see why it's not too late for investors to buy this hot AI stock.

Image source: Getty Images.

TSMC's AI-fueled growth is here to stay

TSMC reported an impressive 44% year-over-year increase in its Q2 revenue to $30.1 billion, exceeding the high end of its guidance range. Meanwhile, the company's adjusted earnings per share shot up at a much faster pace of 61%, a testament to its solid pricing power.

TSMC controls 68% of the global semiconductor foundry market, well ahead of its closest rival, Samsung, which has a market share of just under 8%. The company has managed to build such a huge gap over the competition thanks to the technological lead of its process nodes. As a result, TSMC has the ability to raise the prices of its services, and that explains why its gross margin increased by more than five percentage points last quarter from the prior-year period.

Importantly, TSMC is now anticipating its full-year revenue will grow 30% in 2025, up from its earlier estimate of mid-20% growth. But TSMC could end the year with an even bigger top-line jump as it has already achieved 40% year-over-year growth in the first half of 2025, and it is expecting a 38% spike in revenue in the current quarter (at the midpoint of guidance).

What's worth noting here is that TSMC says its guidance takes into account the potential impact of tariffs on its business. Even then, the company has raised its full-year outlook, and it won't be surprising to see it end 2025 with a bigger-than-expected jump in revenue and earnings. In fact, TSMC's red-hot growth seems sustainable for a long time to come, considering the secular growth opportunity presented by AI.

The various AI-focused end-markets that TSMC serves are on track to boom remarkably in the next five years. For instance, the investment in AI chips and computing hardware could exceed a whopping $3 trillion by 2030, according to the consulting firm McKinsey.

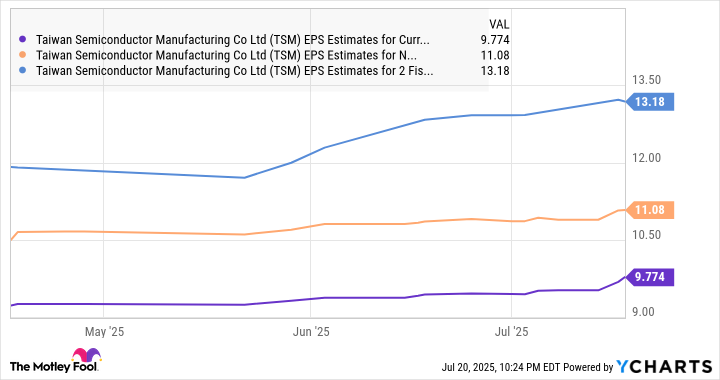

Not surprisingly, analysts are also increasing their estimates for the company's earnings through 2027.

Data by YCharts.

The stock is built for more upside

TSMC stock has jumped an impressive 59% in the past three months. Even then, it is trading at 28 times trailing earnings as compared to the tech-laden Nasdaq 100 index's average earnings multiple of more than 32. The forward earnings multiple of 24 is even more attractive and is yet another signal of the company's continued bottom-line growth.

Investors looking to add an AI stock to their portfolios should consider buying TSMC as a top pick. It has room to run higher and is trading at a discount to the broader technology sector, despite quarter after quarter of outstanding execution.