Has there been as exciting a stock over these past three years as artificial intelligence (AI) software standout Palantir Technologies (PLTR 2.59%)?

Probably not. The company's growth has continued to accelerate since launching its Artificial Intelligence Platform (AIP) for AI applications in mid-2023. The stock id up a whopping 1,300% over the past three years.

It's healthy to be a bit skeptical when stocks generate such massive returns in such a short time. AI continues to prove its staying power, with companies everywhere investing significant resources in data centers and AI development. It's time to look to the future.

So, where will Palantir Technologies be in three years? Here is what investors might expect.

Image source: The Motley Fool.

Palantir's momentum with government and commercial customers gives it a tremendously high ceiling

Over time, AI is likely to become a game-changer for nearly every organization. That goes for government organizations and corporations alike.

What makes Palantir Technologies special is its strong ties to both groups. Its growth momentum is strongest in the United States, where sales from government customers increased by 45% year over year in the first quarter of 2025, and revenue from commercial customers grew even faster, up 71% year over year. Palantir has generated $3.1 billion in revenue over the past 12 months and still has just 769 customers.

Palantir develops custom software for a seemingly endless range of use cases. The military uses it to support missions, and hospitals use it to coordinate staff and patient care. Those are two examples of many. Essentially, any organization that generates data and can benefit from using that data to do things more efficiently or make better decisions is a potential Palantir customer.

Such flexibility in its technology opens up a vast potential customer base. There are roughly 20,000 large companies in the United States, and the government has other departments and organizations. Investors are excited for good reason; Palantir has a high ceiling if things continue to go well.

But the stock price now reflects much of that potential

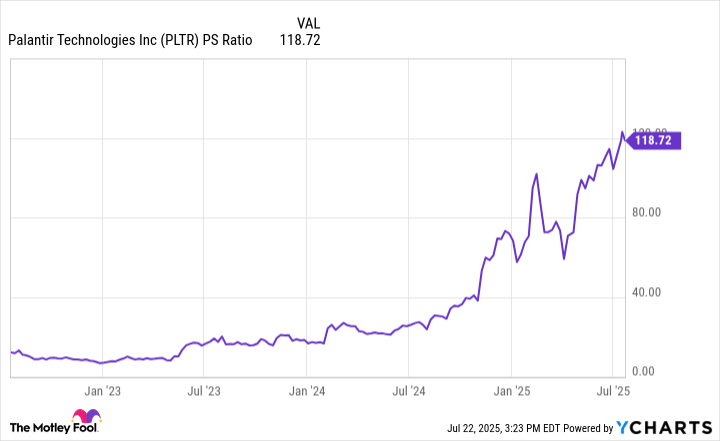

The chart below is not of Palantir's share price but rather its price-to-sales (P/S) ratio. That's the relationship between the stock's market value and Palantir's revenue. If the stock's value and Palantir's revenue rose proportionately, the line would be flat. Instead, it reflects how the stock price has consistently risen faster, pushing that ratio ever higher.

Data by YCharts. PS Ratio = price-to-sales ratio.

Excessive valuations can be hazardous to your portfolio. At some point, valuations can get so high that they create impossible expectations. When the stock inevitably fails to meet those expectations, the share price can unwind violently. The bubble bursts.

At this point, it's fair to argue that Palantir's valuation is irrationally high. There may not be a higher valuation on Wall Street today, and the only similar example I can think of is Snowflake, just after it went public amid a stock market bubble in 2020-2021. Investors who bought Snowflake stock the day it began trading are still waiting for it to show a gain years later.

Here is where the stock may go over the next three years

Nobody can predict where a stock may trade in the future, but the odds are rising that Palantir will serve up disappointing returns for a while from these high prices. I'll assume that Palantir sustains 40% annualized revenue growth over the next three years. That would mean that its trailing-12-month revenue of $3.1 billion would grow to $4.3 billion, then $6 billion, and finally, $8.5 billion three years from now.

Today, Palantir trades at a market cap of $358 billion. Here are some projections for what the stock could do, depending on various valuations.

| Price-to-Sales Ratio | July 2028 Market Cap | Total Three-Year Upside or Downside |

|---|---|---|

| 100 | $850 billion | 137% |

| 90 | $765 billion | 113% |

| 75 | $637.5 billion | 78% |

| 60 | $510 billion | 42% |

| 40 | $340 billion | -5% |

Data source: The author's own calculations.

Palantir's growth could slow down or accelerate, but assuming 40% annualized revenue growth is probably generous. Analysts currently estimate that Palantir's full-year 2025 revenue will be 35% higher than last year, so this exercise assumes growth will accelerate further and then maintain that pace for over two years.

And yet, investors still must hope that the stock can maintain a breathtakingly high valuation. Otherwise, the upside dries up quickly. A P/S ratio of 40 is still very steep. Even Nvidia, perhaps the top AI stock today, trades at 27 times its revenue.

The bottom line? Palantir probably has more room to fall than to continue rising at this point. Therefore, the odds favor Palantir disappointing investors after an epic past three years.