The name Occidental Petroleum (OXY 2.16%) gets more attention than it used to, thanks to the involvement of Warren Buffett and Berkshire Hathaway (BRK.A 0.09%)(BRK.B 0.28%), the company Buffett runs. Given the Oracle of Omaha's fame as an investor, some might buy Occidental Petroleum for this fact alone.

But you'll probably want to get a bit more of an understanding here, because Buffett also owns Chevron (CVX +0.07%), a far larger energy company. There's a lot to unpack.

Why did Buffett get involved in Occidental Petroleum?

Occidental Petroleum has a market cap of around $40 billion, which makes it a large company but a relatively small energy business. To put some perspective on that, ExxonMobil is an industry giant and has a market cap of roughly $450 billion. Chevron, for reference, has a market cap of around $300 billion.

Image source: Getty Images.

Why does size matter here? Because all three energy companies use the same basic business model. They are what are known as integrated energy companies, with operations that span from the upstream (energy production), through the midstream (pipelines), and all the way to the downstream (chemicals and refining). They are, therefore, competitors, with Oxy, as it is more commonly known, the small fry.

But Oxy managed to punch above its weight in 2019 when it bought Anadarko out from under Chevron. That's when Buffett and Berkshire Hathaway got involved, helping to finance Oxy's winning bid for Anadarko. It was a huge sign that Oxy isn't happy living in the shadows -- it wants to grow so it can better compete with the energy sector's largest players. The growth opportunity here is why you buy Oxy.

The problem with Occidental Petroleum

There are some important nuances here, though. For example, the purchase of Anadarko left Oxy's balance sheet in a weakened state. When oil prices crashed during the coronavirus pandemic in 2020, the company was forced to cut its dividend.

However, Oxy has worked hard to strengthen its financial position. And it has already gotten back on the growth via acquisition track.

NYSE: OXY

Key Data Points

That said, this growth-oriented energy company has a somewhat modest dividend yield of 2.2%. Exxon's yield is 3.7%, while Chevron's yield is 4.4%. Clearly, if you are buying Oxy, you are buying for the growth, not the income.

Which brings up an interesting twist: Buffett owns Oxy, but he also owns Chevron. So if you want to invest like Buffett, you could literally buy either one.

Compared to Oxy, Chevron is a slow and steady tortoise, noting that the company has increased its dividend annually for 38 consecutive years. While Chevron offers income, size, and stability, it doesn't offer the same growth prospects. Sure, Chevron will buy other companies, noting it recently acquired Hess. But the vast scale of its operations means such deals won't likely have the same growth impact on its business as will Oxy's acquisitions.

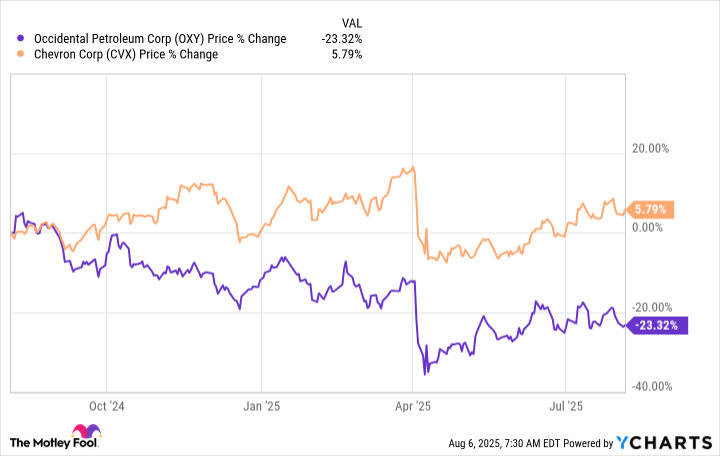

Right now, geopolitical events have left energy prices in a state of flux. Over the past year, Chevron's stock has fallen around 5%. Oxy's shares are down over 20%!

Given the difference in the sizes of these two integrated energy businesses and Oxy's focus on growth, this disparate performance isn't really shocking. Oxy is a riskier energy stock, and Wall Street is treating the shares appropriately in an uncertain period for energy prices.

Oxy could be a buy, for the right investor

Buffett, however, hasn't given up on Oxy. That is a huge vote of support, noting that the Oracle of Omaha likes to hold companies for the long term so he can benefit from the growth of a business over time.

Oxy probably won't appeal to conservative investors or those with an income focus (Chevron would be the better choice). However, if you lean into growth, this dip could be an interesting opportunity to invest alongside Warren Buffett and Berkshire Hathaway while Oxy's stock is trading hands more cheaply.