So, is Caterpillar (CAT +0.49%) stock poised for a metamorphosis? It's an important question, because if the heavy equipment maker is transforming into a less cyclical company with potentially higher profit margins, then the stock could be due for a valuation rerating. That could lead to substantive share price appreciation.

Here's a look at the likelihood of that happening.

Image source: Getty Images.

Caterpillar's traditional cyclicality

The construction, infrastructure, mining, energy, and transportation machinery company is traditionally looked at as one of the great cyclical stocks on the market. In other words, its revenue, margin, and earnings tend to follow its end demand, which tends to be cyclical and often correlates with economic growth.

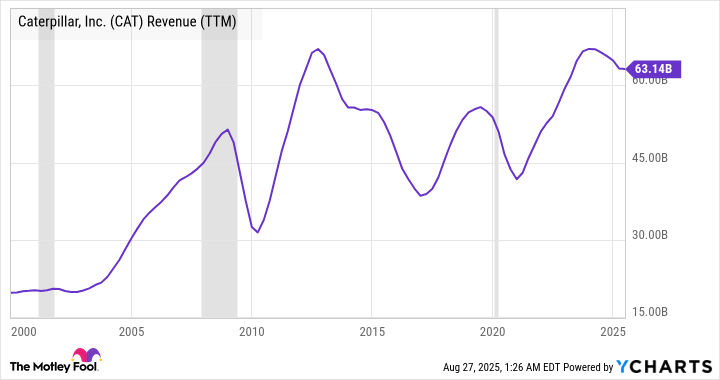

When the economy is booming, developers initiate construction projects, infrastructure projects are built, and demand for commodities rises. Everything points toward more spending on Caterpillar's heavy machinery. As you can see below, its revenue tends to fluctuate periodically. In particular, note the dramatic declines that follow recessions (these figures are based on trailing-12-month figures).

In addition, the period from 2013 to 2016 is weak due to the severe slump in mining and energy commodities during that time -- a point I'll return to shortly.

CAT Revenue (TTM) data by YCharts

The cyclicality of Caterpillar's revenue and earnings means investors have to be careful not to pile in when its revenue is about to peak (when its earnings are high and its price-to-earnings ratio can be low) and also not to avoid buying the stock when its earnings are low (and when its price-to-earnings ratio can be high).

The cyclicality makes things difficult for investors, and it also makes the timing of capital allocation decisions difficult for management.

How Caterpillar can become a less cyclical company

There are two ways this situation can improve. The first is through internal action, such as the initiative to grow its less cyclical services revenue through the use of digitally connected technologies that interact with its machinery, and via the sale of customer value agreements (CVAs) that provide for servicing and maintenance.

Management aims to double its services revenue from $14 billion in 2016 (when it contributed 21% of revenue) to $28 billion in 2026 (which, according to the Wall Street consensus, would represent 39% of revenue). Given that services revenue was $24 billion in 2024 and is expected to be at a similar level in 2025 , there's definitely progress, but it may prove a stretch to get to $28 billion in 2026.

End markets becoming less cyclical?

The second way could come from a flattening of the fluctuations in the trendline of its end markets, or rather, enough of its end markets to reduce over-cyclicality. There is also room for optimism here.

For ease of reference, the chart below breaks out revenue by end market, with energy & transportation (E&T) further broken out. The fast-growing power generation business (sales up 28% year over year in the second quarter) is growing due to its power equipment used as primary and back-up power for data centers.

Data source: Caterpillar presentations. Chart by author.

Meanwhile, its resource mining and oil and gas end markets would benefit from a sustained period of commodity price stability, not least because the miners and oil and gas companies appear to be taking a more disciplined approach to investing, gradually rather than in a boom-and-bust cycle.

Ultimately, the construction machinery segment is likely to remain cyclical overall; however, its sales into infrastructure projects may prove less cyclical in the long term.

Is Caterpillar becoming a less cyclical company?

The shift into more service revenue is definitely helping, and the long-term demand for its power equipment appears to be secular, rather than cyclical, in origin.

However, the reality is that, while mining and energy companies are becoming more disciplined in their spending (implying that supply growth is more measured), many other factors influence the pricing of commodities, such as iron ore. They include the construction end market, which will also be influenced by the interest rate cycle.

NYSE: CAT

Key Data Points

All told, the answer to the question is: Yes, Caterpillar's revenue is becoming less cyclical. But is it about to metamorphose into a company with stable growth prospects, one that investors should not price as cyclical? The answer still has to be no. The company won't stop being cyclical anytime soon. Still, the trend line of its earnings through the cycle could improve thanks to the services initiative and improvements in end markets like power and resources.

It's something to look out for when management subsequently updates its medium- to long-term growth prospects, as it last did in the fourth quarter of 2023, when it upgraded free-cash-flow expectations through the cycle to $5 billion-$10 billion, compared to $4 billion-$8 billion previously.