Back in 2023, Bank of America analyst Michael Hartnett first applied the nickname the "Magnificent Seven" to a group of tech powerhouses that were standing out for their size and recent trend of outperforming the broader market. The rest of Wall Street quickly picked up the phrase. Those companies and their current market caps are:

- Nvidia: $4.4 trillion

- Microsoft: $3.7 trillion

- Apple: $3.3 trillion

- Alphabet (GOOG 2.17%) (GOOGL 2.23%): $2.5 trillion

- Amazon: $2.4 trillion

- Meta Platforms (META 1.20%): $1.9 trillion

- Tesla: $1.1 trillion

All are leaders in their segments of the technology sector, and each is now investing heavily in artificial intelligence (AI) -- outlays that could fuel substantial growth down the line.

Generally speaking, it would probably be a good idea to own all seven of these stocks over the long term, but Meta Platforms and Alphabet look like particularly attractive buys now due to their unique AI strategies and their relatively cheap valuations. When investors look back on this moment in a few years, here's why they might be glad they added those two names to their portfolios.

Image source: Getty Images.

The case for Meta Platforms

Meta owns a family of popular social networks, including Facebook, Instagram, and WhatsApp -- apps that are used by more than 3.4 billion people every day. The company monetizes those platforms by selling advertising slots to businesses, so it makes more money when users spend more time online, because that means they see more ads.

Meta is using AI in its recommendation algorithms to learn what type of content each user likes to see, so it can feed them more of it. During the second quarter, this strategy drove a 6% increase in the amount of time users were spending on Instagram compared to the year-ago period, and a 5% increase for Facebook.

Meta also uses AI in its ad-recommendation engine to target users more effectively, which led to a modest increase in conversions on both Instagram and Facebook during Q2. Since higher conversions give businesses greater returns on their advertising spend, this will allow Meta to charge more money per ad.

But one of the biggest pieces of the company's AI strategy is its Llama family of open-source large language models (LLMs), which are designed to rival some of the best models from leading developers like OpenAI. Llama underpins new features like Meta AI, a chatbot that can answer questions on practically any topic, and even generate images. It already has over 1 billion monthly active users, so it's becoming a key contributor to Meta's mission to boost engagement.

Thanks to higher engagement and better conversion rates, Meta's revenue soared by 22% year over year to $47.5 billion in Q2, well ahead of management's guidance range of $42.5 billion to $45.5 billion. According to Wall Street's consensus estimates (provided by Yahoo! Finance), Meta is now on track to deliver $196 billion in revenue and $28.07 in earnings per share (EPS) during 2025, both of which would be record highs.

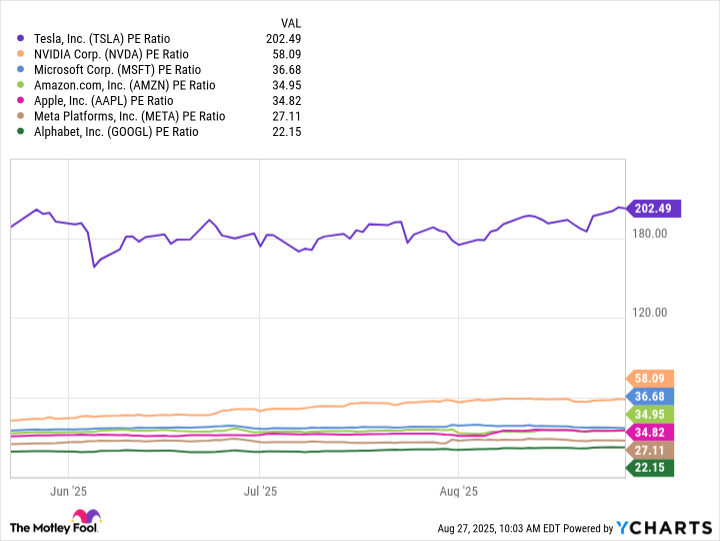

Meta currently trades at a price-to-earnings (P/E) ratio of just 27.3, making it the second-cheapest name in the Magnificent Seven. Therefore, even though the stock is hovering near an all-time high, it might still be a bargain for long-term investors.

The case for Alphabet

Alphabet is the parent company of Google, YouTube, and Waymo, among other businesses. Google Search accounts for the lion's share of its revenue, and despite initial concerns that AI chatbots would pull traffic away from the platform, AI might actually be its greatest tailwind instead.

Alphabet developed a family of LLMs it has dubbed Gemini, and they underpin a new Google Search feature called AI Overviews. They incorporate text, images, and links to third-party sources to deliver responses to users' queries that appear above the traditional search results. This reduces users' need to sift through web pages to find information.

Alphabet said 2 billion people were using AI Overviews during the second quarter, and since they monetize at a similar rate to traditional Google Search results, the new product isn't cannibalizing the company's golden goose.

The Google Search segment generated a record $54.2 billion in revenue during Q2, which was up 11.7% from the year-ago period. This marked an acceleration from the 9.8% growth it delivered in the first quarter, so concerns that AI would disrupt the search engine appear to be overblown.

AI is also driving significant growth for Google Cloud. The company offers state-of-the-art data center capacity and access to the latest LLMs, which are the two main ingredients required to develop and power AI software. That's why nearly all AI unicorns (start-ups worth $1 billion or more) are using the platform.

During Q2, the cloud platform brought in $13.6 billion in revenue, which was up 32% year over year. That was an acceleration from 28% growth in the first quarter. But it gets better, because Google Cloud has a whopping $106 billion order backlog from customers that are waiting for more data center capacity to come online. That should fuel more stellar top-line results from here.

Trading at a P/E ratio of just 22.1, Alphabet is the cheapest Magnificent Seven stock. The company is facing some regulatory issues and a court ruling that could disrupt its business in the short-to-medium term, but I think its valuation fairly compensates investors for the potential risks. Given the momentum in Gemini, Google Cloud, and AI Overviews, I think investors who buy Alphabet stock now will be glad they did when they look back on this moment in a few years.