At a time when many automakers are pulling back from electric vehicles (EVs), Rivian Automotive (RIVN 0.89%) is embracing its branding as an EV-only company. It just broke ground on a new factory in Georgia, with plans to bring out cheaper models of its beloved cars within the next few years. Despite the ending of the U.S. government tax credit for EV purchases, Rivian believes the future of cars is still electric.

Rivian stock has recovered on this new plan, but is still at a price of around $15 compared to its debut of over $100 after its initial public offering (IPO). With its major expansion plan, could buying Rivian stock today set you up for life?

Unprofitable today at subscale production levels

Starting an automaker from scratch is difficult, but Rivian has gone from concept to production with the help of large investors such as Amazon (which is also a customer of its EV delivery vans). Back in 2022, the company started delivering its EV commercial vans as well as its R1 SUV and truck models to customers. So far, customers seem to love these vehicles, giving them rave reviews.

However, Rivian has failed to expand its quarterly deliveries from 10,000-15,000, making it a subscale player in the automotive space. For reference, Tesla does close to 500,000 deliveries every quarter. The problem for Rivian is a lack of cheaper options for customers to buy. The R1S and R1T cost $75,000 or more, which limits the vehicle to only a small sliver of the United States population. With the EV tax credit ending in September, this problem may worsen in the quarters to come.

Rivian has not generated a profit due to this subscale. Last quarter, Rivian generated just $1.24 billion in revenue, $206 million in gross profit, and had $526 million in negative free cash flow. Its cash burn has improved in recent quarters, but it will remain unprofitable unless it can get its deliveries higher to cover the fixed costs of running car manufacturing plants.

Image source: Getty Images.

Expanding in Georgia for cheaper future models

In 2025, Rivian expects to deliver just 40,000-60,000 vehicles to customers, which is not much higher than recent years. From 2026-2030, it is expecting an inflection in customer deliveries.

At its first Illinois plant, the company is expanding its capacity for a production line for the R2 model, which is expected to commence in the first half of 2026. The base price of the R2 is $45,000, which will help Rivian expand to a wider customer base.

In Georgia, Rivian just broke ground on a new factory, which may be helped by a loan from the Department of Energy. This factory will support wider production for the R2 and an upcoming R3, which will be a smaller SUV at an even lower price point. Once scaled, Rivian will hopefully be able to produce hundreds of thousands of vehicles for customers a year to take advantage of the long-term trend of EV adoption.

EV adoption has slowed down due to higher interest rates and the popping of the 2021 sector bubble, but the long-term trend still calls for more and more car sales to become electric through 2030. Rivian is investing now to take advantage of this trend.

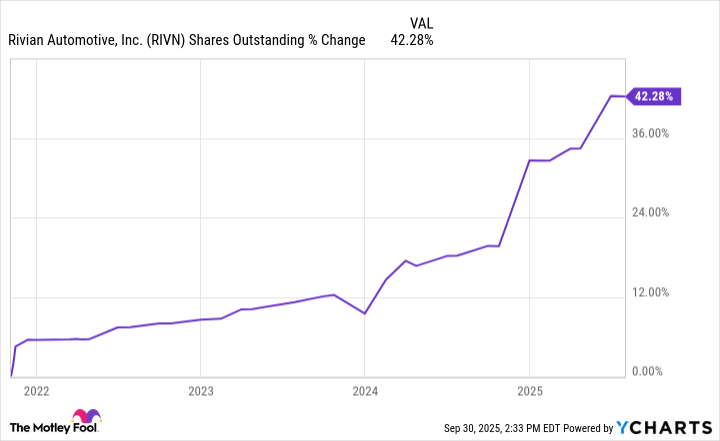

RIVN Shares Outstanding data by YCharts

Is Rivian stock a buy?

Rivian generates around $5 billion in annual revenue compared to a market cap of $17.7 billion. The company has to dilute shareholders to raise money to keep enough cash on the balance sheet, which is why its shares outstanding are up 42% since going public in 2021. It has an equity financing and debt deal with Volkswagen, with Rivian helping the legacy automaker with software and autonomous driving systems.

Even though it will burn cash for at least the next few years, Rivian has over $10 billion of cash and available financing sources it can use to fund its factory expansion in both Illinois and Georgia.

If the company can reach scale, it could be on a path to $20 billion in annual revenue or more by 2030. A simple 5% profit margin -- slightly at the low end for an average carmaker -- would give the company $1 billion in annual net earnings by 2030, or a price-to-earnings (P/E) ratio of 17.7 based on the current market cap. This market cap will keep getting diluted, while debt is also added to the balance sheet that needs to be accounted for.

All in all, Rivian stock looks like it could be a solid buy for investors if you believe in the long-term vision. But at current prices, it does not look like a huge multibagger stock that will set you up for life.