Publicly traded companies do different things with the shares they issue for different reasons. For instance, they will distribute new shares for sale to investors as a way to raise capital. This happens at the initial public offering (IPO), but it can also happen later on with secondary offerings.

If the circumstances call for it, they will also initiate stock splits, either a forward split or a reverse split. When companies split their stocks, they aren't raising money. Rather, they're changing how many shares exist and what each share is worth. Let's say that you own one share of a stock valued at $100. If the company does a 2-for-1 forward split, you'll now own two shares instead of one, but each share will be worth about $50. The shares are worth half as much, but there are twice as many, so the overall valuation stays the same.

Companies tend to execute splits when their stock prices have gone up by a significant amount. And that certainly applies to parts retailer O'Reilly Automotive (ORLY -0.94%) and bottler and distributor Coca-Cola Consolidated (COKE 0.05%). These two stocks have risen 497% and 473%, respectively, in value over the last 10 years. And that motivated the companies to split their stocks earlier in 2025.

Image source: Getty Images.

In June, O'Reilly did a huge 15-for-1 stock split, its first stock split since 2005. Coca-Cola Consolidated executed a 10-for-1 stock split back in May.

Here's why analysts believe that there's upside for O'Reilly stock and why investors might want to put Coca-Cola Consolidated on their radars even though it's completely off of Wall Street's.

Wall Street is bullish on O'Reilly Automotive

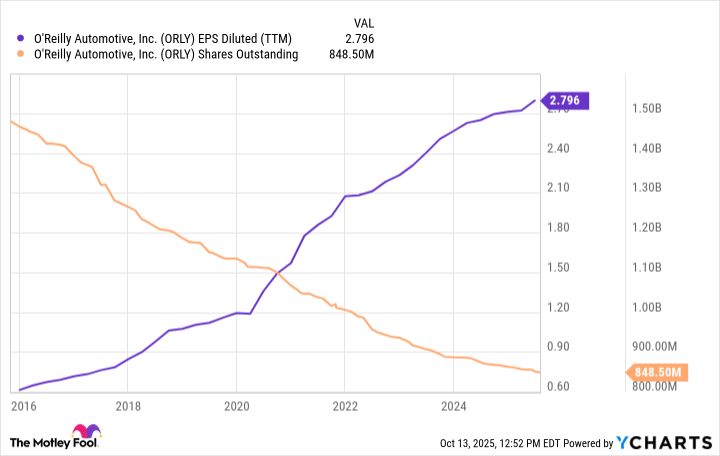

O'Reilly Automotive operates about 6,500 retail stores in North America, selling everything you need for maintaining and repairing used vehicles. There's nothing fancy about this business. But management is consistently able to achieve top-notch operating margins, which currently sit at 19%.

Analysts at TD Cowen are among Wall Street's most bullish on O'Reilly. Last month, the investment firm gave O'Reilly stock a price target of $125 per share, implying about 21% upside from where it trades as of this writing. Price targets usually have about a one-year outlook, so TD Cowen believes O'Reilly stock could see this appreciation before the end of 2026.

O'Reilly's management expects to have about $2.90 in full-year earnings per share (EPS) in its fiscal 2025, which would represent about a 6% increase from its split-adjusted EPS of $2.73 in 2024. But TD Cowen believes EPS growth in 2026 will be even better, calling for 2026 EPS of $3.30, a 14% increase from management's projections for this year.

To be sure, O'Reilly Automotive continues to grow revenue with new locations and same-store-sales gains. But management repurchases a lot of stock as well, which boosts its EPS. It's a big reason that it's been a long-term winner, and it's something that many investors expect to continue.

Data by YCharts.

Coca-Cola Consolidated is not getting as much attention

According to TipRanks and MarketWatch, there aren't any prominent Wall Street firms currently covering Coca-Cola Consolidated stock. Despite its long-term market-beating performance, it's completely off of Wall Street's radar.

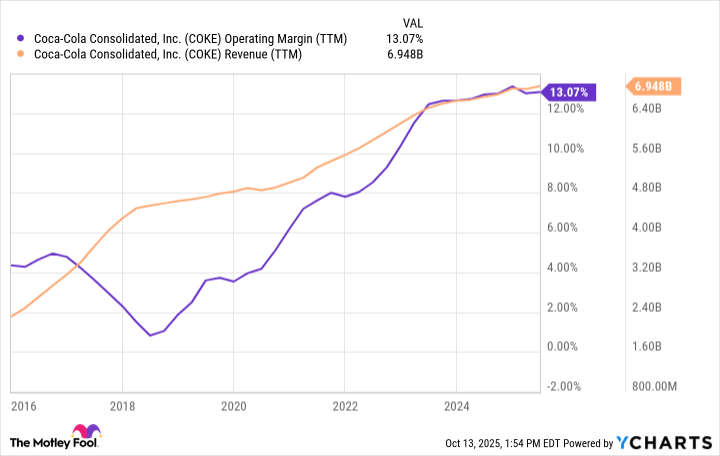

Coca-Cola Consolidated is the largest bottler of Coca-Cola products in the U.S., and it has grown substantially over the years by acquiring the rights to distribute in more territories. That seems to be less of an opportunity today compared to what it's been in the past. But management still has ways to increase profits.

In 2025, Coca-Cola Consolidated focused its investments in its own facilities. For example, it invested $90 million in its facility in Columbus, Ohio. Past facility investments have made operations more profitable, boosting overall profits. And this long-term trend has helped make it a winner.

Data by YCharts.

It won't be flashy, which is likely why it gets so little attention. But Coca-Cola Consolidated has a steady business bottling and distributing some of the most well-known beverage brands. Management generates substantial cash flow that it invests back in the business. And this often results in higher profits, leading to a higher stock price. That can keep working from here.

The better buy today

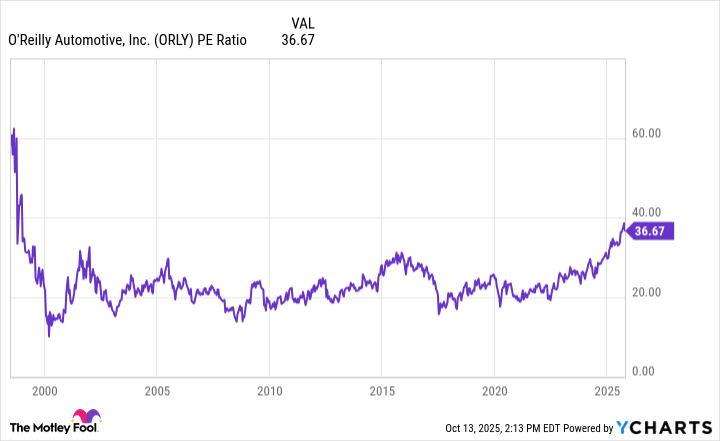

While O'Reilly may enjoy better EPS growth from here, Coca-Cola Consolidated may be a better long-term buy. TD Cowen is perhaps the most enthusiastic about O'Reilly stock from here. But the firm's price target implies it will trade at 38 times its earnings. That's pricey.

Not only is it pricey in absolute terms, but if O'Reilly traded at 38 times its earnings, it would be the most expensive valuation for the stock in nearly 30 years.

Data by YCharts.

Future stock buybacks could make the valuation a little more palatable. But still, the valuation for O'Reilly Automotive is stretched for a low-growth business. Therefore, as much as O'Reilly is a high-quality company, I'd choose Coca-Cola Consolidated stock today. It's also a high-quality business, and the valuation is far more reasonable.