Microsoft (MSFT 0.47%) fell just 0.1% on Nov. 7. But it was enough to extend the stock's consecutive down days to eight.

Reports indicate that the eight-session losing streak is Microsoft's longest since 2011. And it comes on the back of Microsoft's first-quarter fiscal 2026 earnings, which were released on Oct. 29.

Here's why Microsoft is now down more than 8% from its 52-week high, and why the megacap growth stock is an excellent buy now.

Image source: Getty Images.

A maturing market

Microsoft isn't the only megacap tech stock that is selling off.

Meta Platforms is down big since reporting earnings. Oracle has given up nearly all the gains that followed its first-quarter fiscal 2026 results and the announcement of its $300 billion multiyear cloud deal with OpenAI. Meanwhile, Nvidia and Palantir Technologies have sold off since Michael Burry -- known for his bet against the housing market in 2006 that paid off in 2008 -- disclosed a $1.1 billion short position on the two artificial intelligence (AI) growth stocks.

The sell-offs in prominent AI stocks show that the AI investment narrative is maturing. Instead of reacting positively to AI spending announcements, investors want to see a clear roadmap for AI investments to pay off.

NASDAQ: MSFT

Key Data Points

Microsoft is pouring money into AI

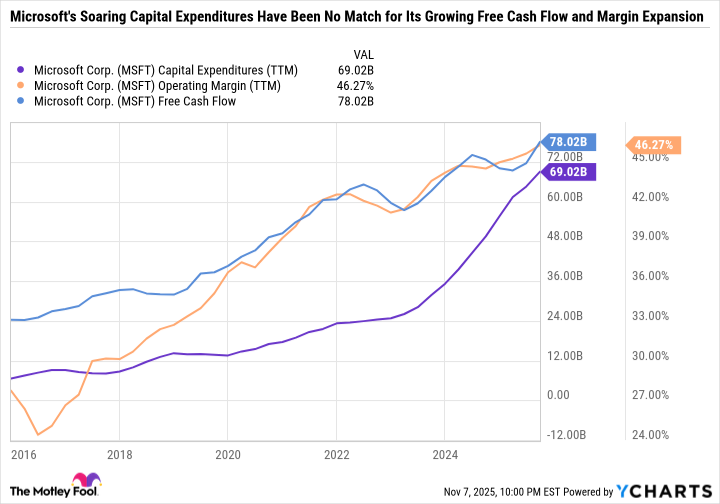

In its latest quarter, Microsoft announced accelerated spending on graphics processing units and central processing units to increase capacity needed to fulfill AI and cloud demand. The spending may come as a surprise, given that Microsoft's capital expenditures (capex) have nearly tripled in the last three years.

As you can see in the following chart, Microsoft has accomplished the very difficult task of growing its operating margin and free cash flow (FCF) despite surging capex.

MSFT Capital Expenditures (TTM) data by YCharts

However, some investors may fear that higher capex for long-term projects that could take a while to pay off will eventually erode FCF and lead to margin compression.

There's already evidence that Microsoft's AI spending is impacting its capital allocation. Microsoft has reduced stock buybacks so that it can increase capex without straining its balance sheet. Long-term investors would probably prefer that Microsoft invests in ideas that can boost its operating income rather than just reducing its share count with buybacks. However, the move does add pressure on ideas to pay off.

Microsoft's ace in the hole

While it's understandable why some investors would be questioning the pace of Microsoft's AI spending, I'd argue that this is precisely the kind of move that Microsoft should be doing.

If there were any hyperscaler that can afford to overspend and take risks, it's Microsoft. The company's impeccable balance sheet and high-margin business give it a significant advantage in the AI race. In its latest quarter, all three of Microsoft's business segments achieved operating margins of at least 30% -- even its consumer-facing more personal computing segment. And the larger the segment by revenue, the higher the margin.

In other words, if Microsoft overspends on AI, it still has many levers it can pull to grow earnings and cushion the blow of higher capex. On the other hand, Amazon relies heavily on Amazon Web Services to drive its cash flows and long-term investments, Alphabet leans on Google Search for its cash flows, and Oracle is taking on considerable debt to build more than 70 data centers in just a few years.

A foundational AI stock to buy now

One of the greatest challenges during roaring bull markets is differentiating between the stocks that are rising due to improving fundamentals and those that are inflated by hot air. Microsoft has more than doubled in the last three years. And yet, it's still arguably a good value because the company is at the top of its game and has plenty of ways to consistently grow high-margin earnings for decades to come.

In today's premium-priced market, Microsoft is a solid buy for investors seeking an AI leader well positioned to withstand a cyclical slowdown in AI spending or a broader economic downturn.