It's that time of the quarter when hedge funds file their 13F documents. 13F filings reveal the buys and sells of major SEC-registered hedge funds during the prior quarter, providing insight into the thinking of these big-time investors.

One of the most prominent names in the hedge fund world is David Tepper of Appaloosa Management, a renowned value investor with a long track record of outperformance, who's also the current owner of the Carolina Panthers.

Tepper made some interesting moves last quarter, trimming several AI and technology-related stocks while adding to beaten-down consumer names, the biggest of which was appliance giant Whirlpool (WHR +0.66%). Whirlpool is now even cheaper today than it was when Tepper bought it, so investors may want to dig into this story further.

Image source: Getty Images.

Trimming the AI winners

Notably, Tepper trimmed many of his technology sector positions in Q3, and completely sold out of both Intel (INTC 3.17%) and Oracle (ORCL +3.10%). Intel rocketed about 50% higher in the third quarter after both the U.S. government and Nvidia invested in the chipmaker, which is embarking on an ambitious turnaround. Oracle stock surged by some 40% after its September earnings report, when it announced a significant increase to its cloud backlog.

Tepper decided to book profits in these names while also trimming most of his other AI technology stocks during the quarter, including several of the Magnificent Seven and his basket of Chinese tech stocks.

It's no surprise to see Tepper take some chips off the table, as the AI tech sector has been a tremendous winner this year, culminating in a big spike in September. That's likely when Tepper decided to cash in these tech holdings and rotate into other beaten-down parts of the market.

NYSE: WHR

Key Data Points

Whirlpool was the biggest buy

With the technology winnings, Tepper bought up several beaten-down consumer discretionary stocks, with laundry machine and refrigerator giant Whirlpool being the largest purchase. In fact, Whirlpool went from zero to becoming Tepper's third-largest holding, at 5.85% of the Appaloosa portfolio.

Whirlpool has seen its stock decline a whopping 75% from its 2021 highs and is down 40% on the year. Tepper likely sees value in the beaten-down stock price, and perhaps anticipates improvement in earnings on the horizon.

What caused Whirlpool's fall? Mainly, the company has been hit by the horrible post-pandemic housing bust. Homeowners have been reluctant to move due to locked-in low-rate mortgages. At the same time, many prospective new buyers have been priced out of many markets. Thus, housing sales have slowed to a crawl over the past four years, with little if any sign of recovery, with appliance sales following suit.

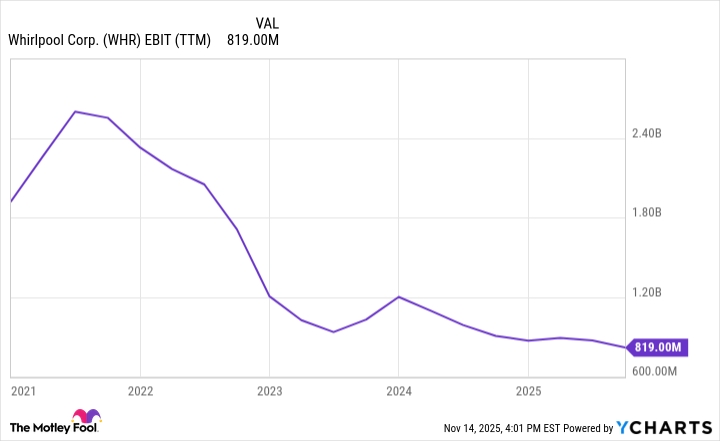

As you can see, Whirlpool's operating income has declined from approximately $2.5 billion at the height of the pandemic housing boom to just over $800 million today, a decrease that almost precisely mirrors the extent of its stock price decline.

WHR EBIT (TTM) data by YCharts

On top of the housing bust, Whirlpool has also been a victim of the new tariffs imposed this year, though not in the way you might think. Whirlpool actually sources 80% of its North American inventory from U.S. production facilities. So, you might think it would be a tariff winner.

However, as tariffs have phased in throughout the year, foreign competitors have accelerated their sales to the U.S., and U.S. retailers have pre-bought those items in an attempt to get ahead of the tariff implementation, while slowing their purchases of domestically made Whirlpool items.

Tepper is betting on a reversal

In all likelihood, Tepper likely sees retailers reverting to buying Whirlpool items after tariffs are fully implemented. During the recent conference call, Whirlpool's CEO noted that the full burden of reciprocal tariffs finalized in August didn't take effect until October 5.

Now that these tariffs are entirely in effect, retailers may resume purchasing Whirlpool appliances more regularly. While last quarter's results continued to disappoint, CEO Marc Bitzer noted the turn was not a question of "if, but when."

Meanwhile, if we experience a housing recovery, that could be a double-catalyst for higher sales and earnings. A housing recovery could begin if longer-term interest rates moderate, or if sellers locked into low-rate mortgages run out of patience and begin putting their homes up for sale.

Should investors follow suit?

Before investors follow Tepper into this trade, a word of caution. First, Tepper bought Whirlpool shares in the third quarter, when prices ranged between $80 and $100, significantly higher than they are now, around $70 per share.

So thus far, Tepper has been wrong on the stock. Whirlpool has also been increasing its debt load and now has net debt of around $5.2 billion. That's significant, considering how low earnings are at the moment. Earlier this year, the company cut its dividend, and Whirlpool is also currently logging negative free cash flow.

So while Whirlpool may present an interesting turnaround opportunity, investors should exercise caution. It appears to be a high-risk, high-upside bet on the part of Tepper, and somewhat of a bet on a housing recovery that hasn't yet emerged.