In this age of e-commerce, a brick-and-mortar retail chain making customized stuffed animals might sound like a business model that's barely hanging by a thread. But that couldn't be further from reality for Build-A-Bear Workshop (BBW +0.98%).

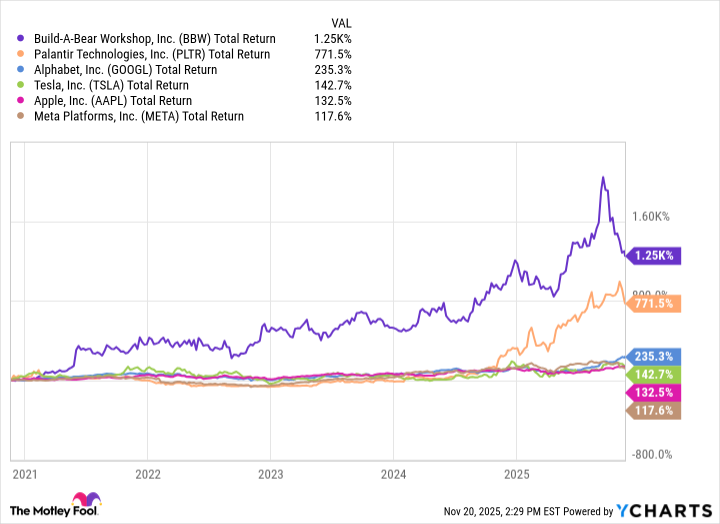

Build-A-Bear is flourishing, the business is growing, and long-term investors have enjoyed plush returns. Over the past five years, Build-A-Bear stock has outperformed the likes of Alphabet, Apple, Meta Platforms, Palantir, and Tesla by a wide margin, delivering a total return of 1,250%.

Data by YCharts.

Thinking of starting a position in Build-A-Bear? Here are three things you should know.

1. The first half of 2025 was the best in company history

Build-A-Bear just notched its most profitable second quarter and first half in company history. Revenue for the first half of fiscal 2025, which ended Aug. 2, hit an all-time high of $252.6 million, an 11.5% year-over-year increase. First-half pre-tax income jumped 31.5% to nearly $35 million, and diluted earnings per share (EPS) catapulted 44.5% to $2.11 -- both company records.

Build-A-Bear's first-half momentum prompted management to raise its full-year guidance for revenue, pre-tax income, and new store growth. This wasn't an outlier, either. Build-A-Bear has posted four consecutive years of record results, and management is expecting fiscal 2025 to be another record-setting year, assuming no dramatic shifts in tariff policy or the economy.

Image source: Getty Images.

2. Build-A-Bear is diversifying its business model

Expanding beyond its traditional retail model of corporately managed, mall-based stores has given Build-A-Bear multiple levers to accelerate revenue and earnings growth. For example, partner-operated stores like those at Great Wolf Lodge, Kalahari Resorts, and Girl Scouts Shops now comprise 25% of Build-A-Bear's total store count. These stores shift much of the capital expenditures burden to the operators and enable Build-A-Bear to generate higher-margin revenue through wholesale merchandise sales.

Commercial revenue -- primarily generated by wholesale distribution to partner-operated stores -- has increased at a 63% compound annual growth rate over the past five years. International franchise stores have become another growth lever, with revenue soaring 177% in that same period.

Build-A-Bear has been amping up its social media presence to drive digital sales. The brand now has more than 800,000 Instagram followers and 2.8 million Facebook followers. Online sales were down 12% last year, but they jumped 15% in Q2 2025.

NYSE: BBW

Key Data Points

3. Build-A-Bear is cozying up to shareholders

Build-A-Bear's shift to a more capital-light retail model has increased free cash flow by 44% over the past four years, and the company seems to delight in returning cash to shareholders. In the first half of 2025, it repurchased $7.3 million worth of its common stock and paid $5.8 million in quarterly cash dividends. Build-A-Bear repurchased $31 million worth of its stock last year.

Build-A-Bear's small float -- 12.2 million shares based on the latest available data -- has made it a popular target for short sellers and meme stock enthusiasts. But don't let that distract you. This is a high-quality company with strong brand equity, improving margins, and consistent growth -- and it's trading at a modest forward price-to-earnings (P/E) ratio of 11.5. While the exponential gains from its penny stock days may be hard to replicate, I still think there's a decent bull case for Build-A-Bear Workshop.