Despite a bumpy beginning to April, 2025 has shaped up as another banner year for Wall Street's major stock indexes. The benchmark S&P 500 (^GSPC 0.19%), growth stock-dominated Nasdaq Composite (^IXIC 0.10%), and ageless Dow Jones Industrial Average (^DJI 0.80%) have all logged several record-closing highs this year.

There's little question that hype surrounding the evolution of artificial intelligence has powered all three indexes higher. Empowering software and systems with the tools to make rapid decisions without the need for human oversight or intervention is a potential game changer for most industries around the world.

Investors are also excited about the Federal Reserve's ongoing rate-easing cycle. Lowering interest rates makes borrowing less costly for businesses, which can lead to increased hiring, more spending on innovation, and an uptick in merger and acquisition activity.

Image source: Getty Images.

But things may not be as rosy with the U.S. economy as the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average would appear to indicate. While the economy and stock market aren't joined at the hip, what happens with the former typically influences the latter.

According to several economic data points, the foundation of the U.S. economy appears to be breaking -- and Wall Street has, thus far, been content in turning a blind eye.

Key economic indicators are making dubious history

To preface the following discussion, no data point or correlated event can guarantee what's to come for the U.S. economy or stock market. Nevertheless, select data points and correlative events do have a phenomenal track record of forecasting the future. The following economic indicators all suggest trouble is brewing with the U.S. economy and/or banking system.

To begin with, the delinquency rate for commercial mortgage-backed securities (CMBS) hit an all-time high of 11.76% in October 2025, according to commercial real estate research and analytics firm Trepp. To put this figure into perspective, CMBS delinquencies have increased almost tenfold since 2023 and are now a whole percentage point higher than they were in the years following the financial crisis.

BREAKING 🚨: Commercial Real Estate

-- Barchart (@Barchart) November 18, 2025

Office CMBS Delinquency Rate jumps to 11.8%, the highest level in history 👀 pic.twitter.com/O3TCPJFEmk

With interest rates kept at or near historic lows by the Federal Reserve throughout the 2010s and following the COVID-19 pandemic, commercial real estate builders saw opportunity, even if corporate demand for office space wasn't apparent. However, a modest uptick in the U.S. unemployment rate, coupled with growth in the work-from-home culture that stemmed from the pandemic, has left the commercial real estate landscape in a potentially precarious position.

Auto loan delinquencies are also climbing at an alarming pace. According to the latest update from Fitch Ratings, the Auto Loan 60+ Delinquency Index -- this measures subprime auto loans where payments are delinquent by at least 60 days -- hit an all-time high of 6.65% in October. Subprime auto loan delinquencies during the Great Recession topped out at around 5%, and previously peaked at close to 6% in 1996.

Americans are falling behind on their car payments at alarming rates:

-- The Kobeissi Letter (@KobeissiLetter) October 26, 2025

Subprime auto loan delinquency rates reached 6.43%, the 2nd-highest on record.

The 60-day delinquency rate for subprime auto loans has more than DOUBLED over the last 3 years.

Delinquency rates are now... pic.twitter.com/upYHNGcm83

As of the end of September, outstanding auto loan debt in the U.S. stood at $1.66 trillion. Although an auto loan delinquency crisis wouldn't hit the U.S. financial system as hard as the subprime mortgage crisis did in the late 2000s, it wouldn't be a drop in the bucket or something that could be swept under the rug, either.

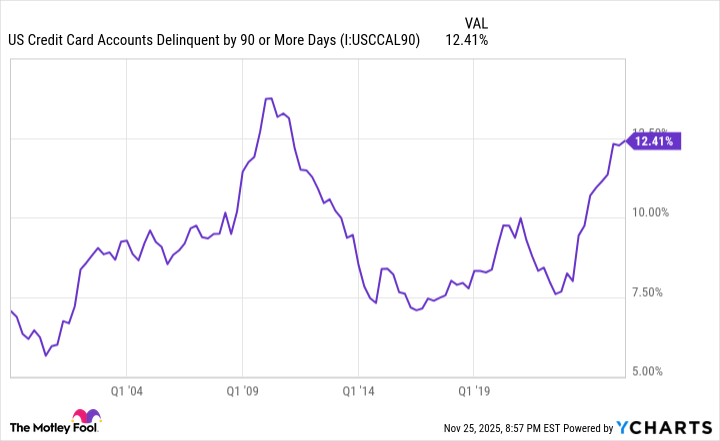

The final piece of this terrifying puzzle involves severe U.S. credit card delinquencies, which have been steadily increasing over the past two years.

US Credit Card Accounts Delinquent by 90 or More Days data by YCharts.

Based on data provided by the Federal Reserve Bank of New York, the share of U.S. credit card balances in arrears on their payments by at least 90 days rose to 12.41% in the third quarter of 2025. This represents the highest percentage of severe delinquencies since the first quarter of 2011, and is about 130 basis points away from setting an all-time high, which was recorded in 2010, shortly after the height of the financial crisis.

With outstanding credit card debt surging to a record high of more than $1.2 trillion, it suggests that consumers are on a weaker financial footing than the stock market's run-up would indicate.

Image source: Getty Images.

Economic cycles aren't linear -- and that's great news for long-term investors

However, historical precedent tends to be more friend than foe for long-term investors. Although a growing number of economic indicators foreshadow trouble to come for the U.S. economy and Wall Street, time has proved to be the greatest ally of both.

As much as workers and investors might fear recessions and slowdowns, they're a normal, healthy, and inevitable part of the economic cycle. No degree of well-wishing or fiscal/monetary policy maneuvering can prevent recessions from happening.

But what's crucial to note is that economic cycles aren't linear. In other words, economic expansions and recessions aren't mirror images of each other.

Since the end of World War II (September 1945), the average U.S. recession has lasted around 10 months, with no downturn enduring longer than 18 months. In comparison, the typical economic expansion has lasted for approximately five years, with two periods of growth surpassing the 10-year mark. Even though it's impossible to predict when recessions will materialize ahead of time or what catalyst is responsible for pushing the U.S. economy over the proverbial cliff, the nonlinearity of economic cycles ensures steady growth over long periods.

This disparity between optimism and pessimism is also evident in the S&P 500, Nasdaq Composite, and Dow Jones Industrial Average.

In June 2023, shortly after the S&P 500 had bounced 20% from its October 2022 lows and entered a new bull market, the analysts at Bespoke Investment Group published the data set you see below on X (formerly Twitter).

It's official. A new bull market is confirmed.

-- Bespoke (@bespokeinvest) June 8, 2023

The S&P 500 is now up 20% from its 10/12/22 closing low. The prior bear market saw the index fall 25.4% over 282 days.

Read more at https://t.co/H4p1RcpfIn. pic.twitter.com/tnRz1wdonp

This data set compares the calendar-day length of every S&P 500 bull and bear market dating back to the start of the Great Depression in September 1929. Whereas the average bear market downturn has resolved in 286 calendar days (roughly 9.5 months), the typical S&P 500 bull market has lasted for 1,011 calendar days, or approximately two years and nine months.

Furthermore, Bespoke's data set shows that the longest bear market persisted for only 630 calendar days. If the current S&P 500 bull market is extrapolated to the present day, 14 out of the 27 bull markets examined since September 1929 have stuck around longer than the lengthiest bear market.

Historical precedent strongly suggests that maintaining a long-term perspective and investing accordingly is a recipe for success.