It's also a smart idea to consider cutting expenses, which you can do proactively or when a recession hits. It can be a useful exercise to identify how much money you're spending on things you don't need. Try printing out the past two months of your bank and credit card statements and highlighting any expenses you could potentially cut.

Finally, getting rid of high-interest debt before a recession hits can be a smart way to recession-proof your personal finances. In recessions, we typically see loan default rates spike as people lose their jobs and can't pay their bills. As a general rule, the lower your debt level, the better prepared you’ll be for a recession.

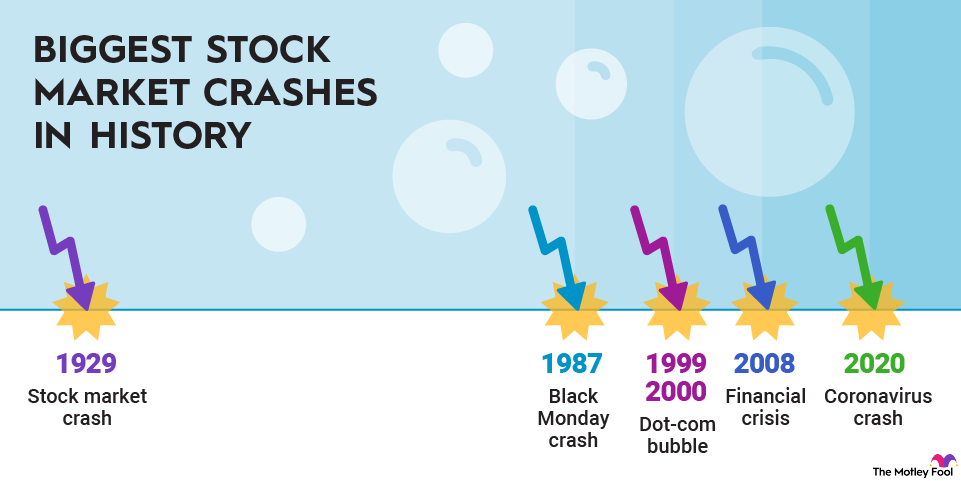

Don't cash out of the stock market

It's common knowledge that the central goal of investing is to buy low and sell high, whether you're talking about long-term investments like a 401(k) or a stock trading strategy. We invest because we hope to sell whatever we buy for more money in the future. However, our instincts tell us to do the exact opposite when times get tough. When the stock market plunges, it's a natural reaction to wonder, "Should I sell and cut my losses before things get any worse?"

With that in mind, it's important to emphasize that cashing out during a recession or market downturn is one of the worst moves a long-term investor can make. For example, if you had cashed out of an S&P 500 index fund when the market first dropped by 20% in the 2007-09 recession, you would have avoided another 30 percentage points of losses before the market reached the bottom. However, you also would have missed out on a subsequent 300% gain. If stock fluctuations stress you out, stop checking your stock portfolio every day and focus on the long term.

Related recession topics