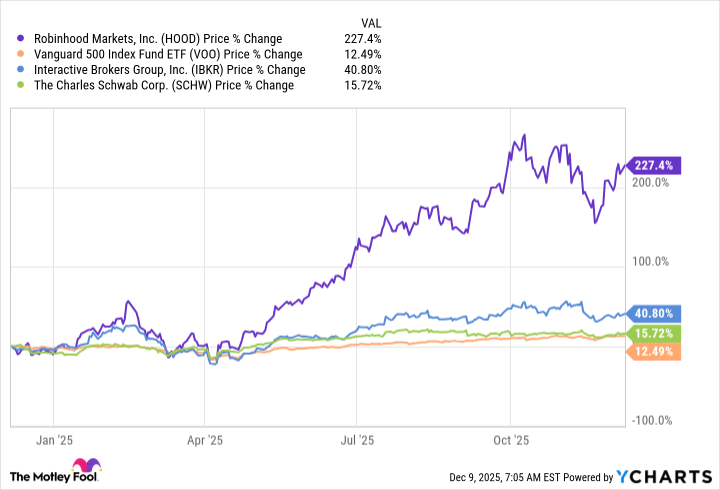

Robinhood Markets (HOOD 3.20%) is a market darling at the moment. That's highlighted by the huge 240% stock price advance over the past year, besting the S&P 500 index (^GSPC 1.23%) by more than 220 percentage points. That's a shocking advance, and it has pushed the stock's valuation to worrying levels. Here's why investors hoping to buy Robinhood and ride it to millionaire riches should probably tread with caution.

What is Robinhood worth?

Charles Schwab is one of the oldest and most respected discount brokers, having effectively helped create the industry in which it now competes. The stock's price-to-earnings (P/E) ratio is 22. Interactive Brokers (IBKR 2.85%) is a large, digitally native discount broker that is a highly respected company. It has a P/E ratio of 32. Robinhood is a relatively young competitor in the discount broker space that has yet to experience a bear market as a public company. Its P/E ratio is a lofty 57.

Image source: Getty Images.

Investors are placing a very high value on Robinhood relative to its peers. To be fair, the company has been a significant force in the discount brokerage industry. For example, the company's free trading approach forced competitors to cut their commission rates. Robinhood has also been quick to embrace alternative assets, like cryptocurrency trading and sports betting. It is, clearly, an industry innovator.

It is also performing very well at the moment. Total net revenue increased 100% in the third quarter of 2025 compared to the same period in 2024. Net income rose 271% and earnings per share jumped 259%. Those are phenomenal results, and they are much better than the numbers put up by Schwab or Interactive Brokers. Schwab's earnings jumped 77% while Interactive Brokers' earnings increased 40%, both of which are solid results.

So, really, all of the discount brokers are doing fairly well at the moment. Robinhood is just doing much better. However, there's a catch. Robinhood's revenue came in at about $1.2 billion, which is a bit smaller than the nearly $1.7 billion Interactive Brokers generated at the top of its income statement. Schwab, however, is much bigger, with revenue of $6.1 billion. Interestingly, Robinhood's top line is about the same size as Interactive Brokers' top line was a year ago.

Robinhood has benefited from being small

The key takeaway from all of this is that Robinhood has been afforded a premium valuation due to its rapid growth; however, that growth has occurred from a relatively small base. Interactive Brokers' recent results offer a warning that continued rapid growth could be harder to achieve from here for Robinhood. Any slowdown in growth could lead investors to drop the stock.

There's one other important issue to consider. Robinhood held its initial public offering (IPO) in mid-2021. That was after the coronavirus pandemic bear market ended. So the only environment in which Robinhood has operated as a public company is in a bull market. Moreover, its customer base skews young and, based on its product offerings, tends to be aggressive.

NASDAQ: HOOD

Key Data Points

While Schwab customers have probably lived through tough bear markets, like the 2007 to 2009 period, Robinhood investors might not know how terrible it feels to watch your wealth shrink day after day. It could have an outsize negative impact on Robinhood's results if its customers stop investing due to the fear associated with deep market downturns. In fact, until the company's business has lived through a bear market, it is hard to know how sustainable the business's growth opportunity really is.

Don't bet too much on Robinhood

Being innovative with risky products in a risk-on market is easy. What happens when a bear market occurs, and investors shift to a risk-off mentality? If that stalls Robinhood's rapid growth, investors are likely to rethink the stock's valuation. However, it might not even take a bear market to slow the discount broker's growth. Its increasing size could make growth harder to achieve. Once again, slower growth could prompt investors to reconsider the above-peer valuation the stock has been afforded.

The only way the current valuation makes sense is if Robinhood's astronomical growth continues. That could happen, but it seems increasingly unlikely. At this point, the big money has likely been made, and all but the most aggressive growth investors should probably tread with caution.