The pressure was on Broadcom (AVGO 5.15%) to deliver blowout fourth-quarter and full-year fiscal 2025 results on Dec. 11. And it didn't disappoint.

Full-year revenue was up 24%, diluted earnings per share soared a mind-numbing 288%, and free cash flow (FCF) popped 39%. Broadcom is doing a phenomenal job of converting sales into high-margin growth and managing its spending so that it doesn't impact its FCF.

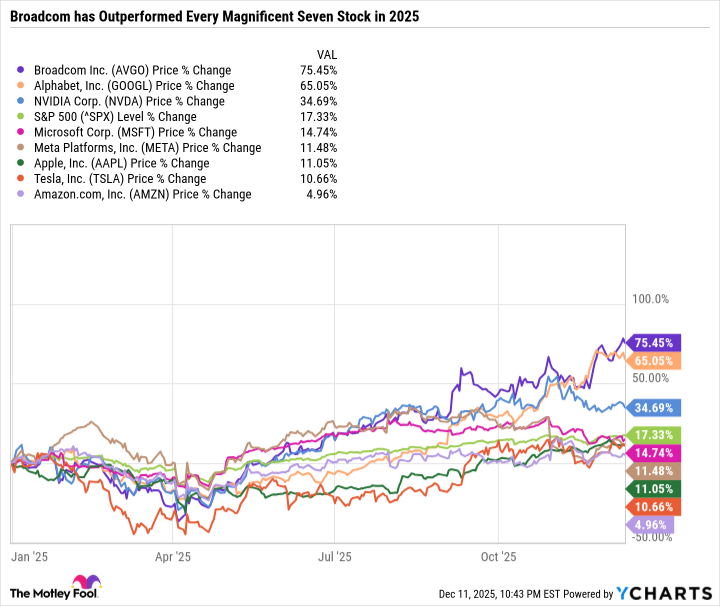

But the market cares more about where a company is going than where it has been. And Broadcom is up huge in 2025, outperforming every "Magnificent Seven" stock -- Nvidia (NVDA +1.47%), Apple, Alphabet (GOOG 0.41%) (GOOGL 0.29%), Microsoft, Amazon, Meta Platforms, and Tesla.

Over the last three years, Broadcom's stock price has skyrocketed over seven-fold. Broadcom is now the sixth-most valuable U.S. company and is within striking distance of surpassing $2 trillion in market capitalization.

With such a rapid run-up in the stock in a relatively short amount of time, some investors may be wondering if Broadcom is overvalued or still has room to run.

Here's how investors should be thinking about Broadcom in December, and if the artificial intelligence (AI) growth stock is a buy for the new year.

Image source: Getty Images.

AI is driving Broadcom's high-margin growth

AI has transformed Broadcom's revenue mix, making it a majority semiconductor solutions business (AI, AI networking, broadband, industrial, networking and general connectivity, server and storage, wireless) rather than infrastructure software (cybersecurity, enterprise software, fiber channel networking, mainframe software, and private cloud).

In fiscal 2025, 58% of Broadcom's revenue came from semiconductor solutions. AI semiconductor revenue increased 74% year over year in Broadcom's latest quarter. For first-quarter fiscal 2026, Broadcom is forecasting $8.2 billion in AI semiconductor revenue, which is twice as much as the first quarter of 2025.

Based on a total revenue forecast of $19.1 billion, Broadcom's AI semiconductor revenue is expected to make up 42.9% of total revenue thanks to growing demand for Broadcom's custom AI chips, called XPUs, and its associated hardware, like Jericho routers and Tomahawk switches. For context, Broadcom generated $12.2 billion in AI revenue for the entirety of fiscal 2024.

NASDAQ: AVGO

Key Data Points

Broadcom's custom AI chips are in the spotlight

Broadcom has room to run because its AI revenue growth is showing no signs of slowing down. A significant reason for this is Broadcom's custom chips used by hyperscalers.

In late November, news broke that Meta Platforms is considering purchasing Alphabet's Tensor Processing Unit (TPU) chips. Broadcom has been collaborating with Alphabet on the development of TPUs for years.

Broadcom's AI accelerator chips are ideally suited for task-specific functions, particularly when dealing with known patterns, whereas Nvidia's graphics processing units (GPUs) are more versatile for AI training, inference, and high-performance computing.

Hyperscalers are realizing that while GPUs are the workhorse of the modern data center, custom solutions with Broadcom can help reduce costs in certain applications. This is why Broadcom is winning massive deals with hyperscalers, and its AI business has increased several times over in just a couple of years.

A balanced AI bet

Unlike Nvidia, which is now almost entirely dependent on selling AI chips and associated software and infrastructure for data centers, Broadcom remains a well-rounded business. AI is its fastest-growing segment, but the rest of the business is performing well. This balance makes Broadcom a better choice for investors seeking diversification. In other words, if there's a slowdown in AI, Broadcom can lean on other parts of its business to pick up the slack.

Broadcom is a solid choice for investors seeking a high-margin business with strong cash flow. Compared to fiscal 2021, Broadcom's fiscal 2025 revenue was up 133%, gross margins grew to a five-year high of 78.6%, adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) were up 160%, and FCF more than doubled.

Broadcom's high profitability and FCF allow it to support a stable and growing dividend. Broadcom has increased its payout for 16 consecutive years, averaging a 30% compound annual growth rate between fiscal 2016 and fiscal 2026. Despite these rapid increases, Broadcom yields only 0.6%, but that's only because the stock has outpaced the dividend growth rate, not a lack of commitment to the dividend.

Data by YCharts.

Broadcom stock is expensive

Broadcom is a phenomenal company. But that's well known. As Warren Buffett famously said, "You pay a very high price in the stock market for a cheery consensus." And that certainly applies to Broadcom at this time.

Analyst consensus estimates call for fiscal 2026 earnings per share of $9.39, and $12.72 in fiscal 2027. Even if we zoom out two years from now to the fiscal 2027 projection, Broadcom is still trading at just over 30 times those earnings.

That doesn't sound too bad, but that's assuming a lot goes right. If there's an industrywide slowdown or Broadcom loses market share to a competitor, the stock could look much more expensive.

Quality at a premium price

Broadcom remains a solid long-term buy for patient investors. But it's unlikely the stock will produce massively outsized returns going forward -- at least until its actual results catch up with expectations.

Broadcom is rising for the right reasons, as its earnings growth is genuine, and it has carved out an invaluable niche within AI data centers and the networking value chain. It's just that Broadcom isn't a great value anymore, so the stock is only a buy for investors who don't mind paying an ultra-premium price.