Amazon (AMZN 0.01%) has been a poor stock to own in 2025. The stock is essentially flat for the year, which is disappointing because the S&P 500 is up around 14%. With 2025 being a disappointing year, investors are hoping that 2026 could be a comeback year.

However, hope isn't an investment strategy; we need real results that will help turn Amazon's stock around. I think Amazon's stock is primed for a good 2026, and I've got a few reasons to back that up.

Image source: Getty Images.

Amazon's stock was expensive entering 2025

First, let's diagnose what went wrong with Amazon's stock in 2025. If you look at Amazon's growth, there is nothing wrong with it

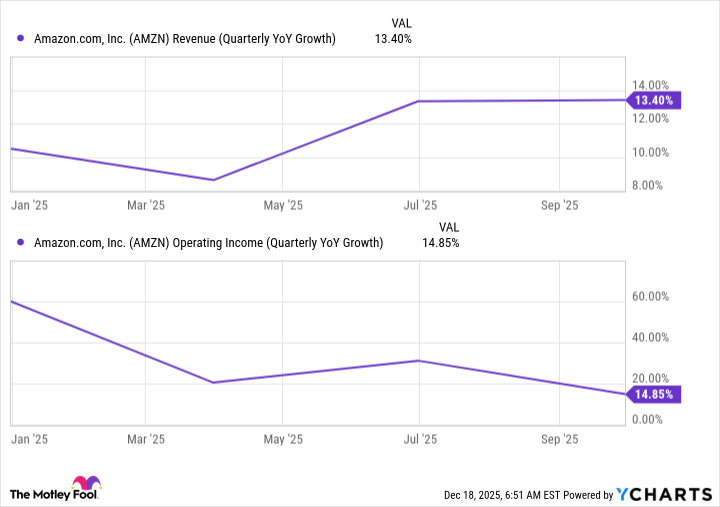

AMZN Revenue (Quarterly YoY Growth) data by YCharts

Outside of one quarter, Amazon's revenue growth was in the low double-digits, which is expected from a mature business. Its operating income growth did slow, but Amazon's efficiency measures were delivering impressive results last year, and those elevated growth rates could never last forever.

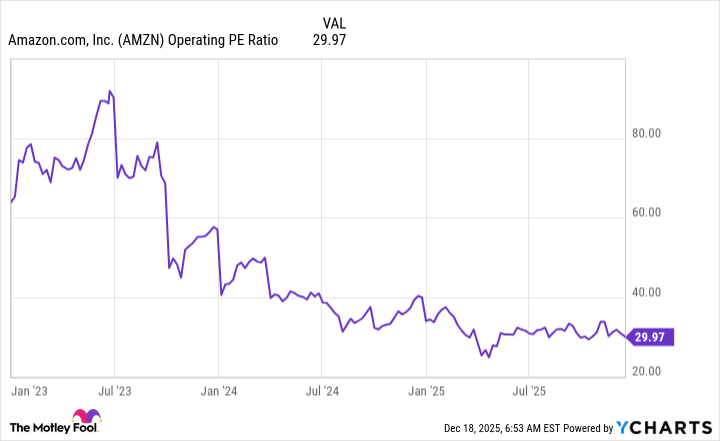

Valuing Amazon's stock using operating income is a wise idea, as it has substantial investments in other companies that can cause its diluted earnings per share (EPS) metric to rise and fall even if it hasn't realized gains or losses on its investments. From a price-to-operating income standpoint, Amazon's valuation has come down throughout 2025.

AMZN Operating PE Ratio data by YCharts

While 30 times operating income isn't necessarily cheap, it isn't far off from its peers. Others like Alphabet and Microsoft trade for 28 and 26 times operating profits, so Amazon isn't overly expensive. With its valuation coming down to a somewhat normal level, Amazon's stock is free to deliver returns in line with business growth, and 2026 is shaping up to be a strong year.

Amazon's most important business unit isn't commerce

Most people think about Amazon's sprawling e-commerce site, but that's not the profit driver in the company. Instead, Amazon Web Services (AWS), its cloud computing wing, drives most of the profits. In Q3, 66% of operating income came from AWS, despite making up 18% of revenue. AWS also grew revenue at a 20% pace in Q3 -- the fastest rate in multiple years. This bodes well for 2026, as AWS is starting to capture more AI workloads, especially with its new chip.

While many AI companies are using Nvidia graphics processing units (GPUs) to train and run AI models, competitors are starting to launch alternatives, including Amazon. Amazon recently unveiled its Trainium3 chips, which helped generative AI companies like Anthropic dramatically reduce their costs. It estimates that Trainium3 chips created an AI video four times faster at half the cost of a GPU. That's just one scenario, but it shows that Amazon's chips are impressive and can compete at the highest level.

NASDAQ: AMZN

Key Data Points

Another area to watch is advertising. Amazon's advertising service has been a monster over the past few years and has grown to become one of its largest segments. Although Amazon doesn't break out advertising's profitability as it does with AWS, it's fairly obvious that this is a high-margin division, as there are several companies that get the majority of their revenue from ads, like Alphabet. In Q3, ad revenue grew 24% year over year. If it keeps up this growth in 2026, it will continue driving outsized profit growth for Amazon.

Ads and AWS may be a smaller dollar figure of Amazon's total, but they account for the majority of Amazon's profits. As long as these two continue posting incredible results, I'll be bullish on Amazon's stock. I think Amazon is due for a comeback in 2026, and these two will be the primary reasons why Amazon's stock is a great buy now.