UnitedHealth Group (UNH +1.91%) has long been one of the premier health insurance companies in the United States, but it and its stock are not unfamiliar with controversy or volatility. It's been a rough year so far for UnitedHealth's stock. Through Dec. 30, the stock is down roughly 34%.

Much of UnitedHealth's business is stable, but the company is undergoing a transition period. There's a lot to like about the stock -- including how cheap it has become after its recent plunge (a 17 price-to-earnings ratio) -- but I recommend waiting until after its Jan. 27 report before making a decision on whether to buy shares.

Image source: Getty Images.

Why Jan. 27 is important for UnitedHealth Group

UnitedHealth is scheduled to release its full-year 2025 results and, arguably more important, its 2026 financial guidance on Jan. 27 before the markets open.

In May 2025, UnitedHealth suspended its profit forecast for the year after having its first quarterly earnings miss in over a decade. The company blamed the miss on rising costs, as people had more doctor visits and surgeries, which meant UnitedHealth had to pay out more in insurance claims than expected. And since the company had no idea how much its costs would increase, it withdrew its profit forecast.

For investors, this was a red flag, leading to its stock price plunge this year. However, on Jan. 27, UnitedHealth has a chance to change the narrative and clear some of the fog and confusion surrounding its profitability and long-term growth prospects.

NYSE: UNH

Key Data Points

What should investors look for before buying the stock?

When UnitedHealth releases its 2026 guidance, investors should look for projections for earnings per share (EPS), medical care ratio (MCR), and operating margin.

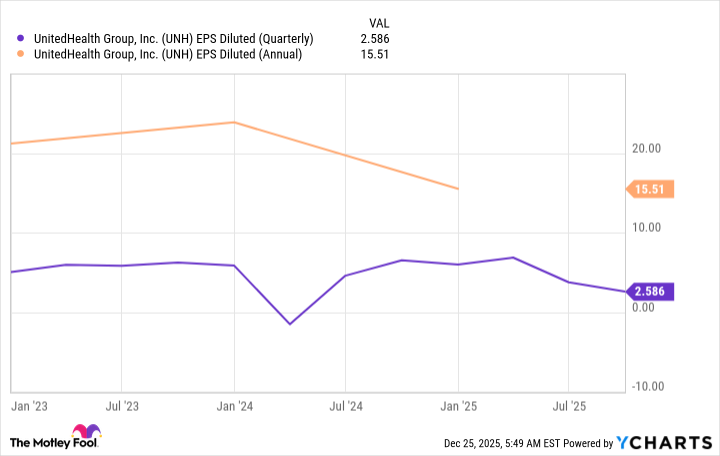

UnitedHealth's 2025 adjusted EPS is projected to come in at at least $16.25, so any 2026 projection that's only a bit above that would mean proceed with caution.

UNH EPS Diluted (Quarterly) data by YCharts. EPS = earnings per share.

MCR is the percentage of money UnitedHealth earns from premiums that it spends on medical claims; the lower the better for the company. Ideally, this number is near the mid-80% range.

Operating margin indicates how much money is left after paying doctors and covering other costs. The higher the better, but 4% is a good benchmark to look for. Though this would likely require UnitedHealth to consider price increases, which would surely bring more scrutiny from politicians and its customers.

So while I would not buy UnitedHealth shares ahead of its Jan. 27 report, if things look good in that release of info, its current valuation could look like a steal for long-term investors.