Palantir Technologies (PLTR 1.87%) delivered another year of stellar returns in 2025, driven by an acceleration in its growth. The booming demand for Palantir's artificial intelligence (AI) software solutions, which are being used by both governments and enterprises, sent the stock up by an impressive 135% last year.

Investors, however, are wondering if it is a good idea to buy Palantir stock following its terrific surge. After all, the company is trading at an expensive 417 times earnings and 117 times sales. Even analysts aren't expecting much upside from Palantir in the next year. Its 12-month median price target of $200 is just 11% higher than the current stock price. Additionally, only a quarter of the 26 analysts covering Palantir suggest buying it now.

However, there is another AI stock that significantly outperformed Palantir last year and is trading at an incredibly cheap valuation right now: Western Digital (WDC +1.64%). Shares of the data storage solutions specialist shot up 282% in 2025. Let's see why that was the case.

Image source: Getty Images.

Western Digital is growing at a red-hot pace

Western Digital is known for manufacturing and selling data storage solutions such as hard-disk drives (HDDs) and solid-state drives (SSDs). It sells these products to consumers, enterprises, and cloud service providers. The company is now getting close to 90% of its revenue from the cloud segment. That's not surprising, as there is terrific demand for storage solutions in AI data centers.

NASDAQ: WDC

Key Data Points

Western Digital management pointed this out on its October 2025 earnings call, with CEO Irving Tan stating:

The rapid adoption of AI and data-driven workloads at hyperscalers is driving robust demand for our products and solutions.

It is easy to see why that's the case. AI model training and inference applications are creating the need to store huge amounts of data, which can then be acted upon by graphics processing units (GPUs) or other types of processors. As reported by Tom's Hardware, each GPU can consume several terabytes of storage.

As a result, the amount of data generated globally is expected to jump by three times between 2023 and 2028, according to IDC. Given that 2% of the data created is stored, Western Digital's addressable market is set to expand at a terrific pace. Specifically, Western Digital points out that AI will lead to a 131% increase in HDD shipments between 2024 and 2028.

However, data center storage demand is growing at a faster pace than supply. There is reportedly a waiting period of more than a year for HDDs. This has led to a jump in the price of HDDs and enterprise flash storage chips. Not surprisingly, Western Digital reported a terrific year-over-year increase of 137% in its non-GAAP earnings to $1.78 per share in the first quarter of fiscal 2026 (which ended on Oct. 3, 2025).

Its top line jumped by 27% during this period to $2.8 billion. Analysts anticipate a 58% jump in Western Digital's earnings in the current fiscal year (which will end in July 2026). However, the company could eventually do better than that. Western Digital said in its previous earnings call that it doesn't plan to add any more production capacity for now. Given that it is one of the leading sellers of storage devices, this decision is likely to boost prices further.

So, there is a good chance of Western Digital's earnings growth coming in hotter than analysts' expectations both this year and in the next fiscal year.

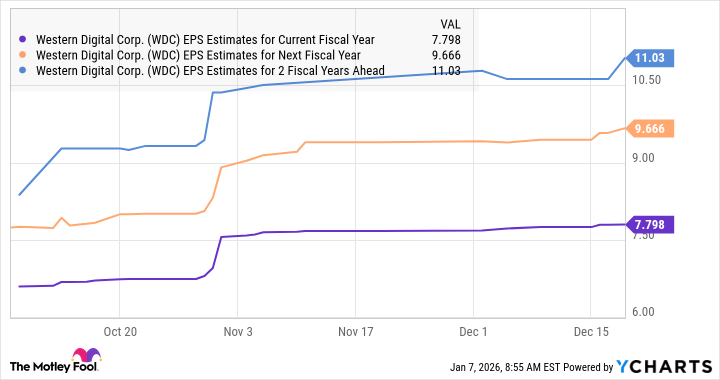

Data by YCharts.

Why the stock is a no-brainer buy right now

The chart above tells us that Western Digital is on track to deliver healthy double-digit earnings growth for the next three fiscal years. It could do better than that thanks to the favorable dynamics of the storage market, but even if its earnings increase in line with Wall Street's expectations, the stock could keep soaring.

Western Digital stock trades at just 23 times forward earnings. That's lower than the Nasdaq-100 index's average earnings multiple of 33 (using the index as a proxy for tech stocks). If Western Digital stock trades in line with the index's average and delivers $9.67 per share in earnings in the next fiscal year (as seen in the chart above), its stock price could hit $319 in the next year and a half.

That's 45% higher than its current stock price. The stock's attractive valuation suggests that investors are getting a good deal on Western Digital, and they should consider buying it hand over fist before it surges higher.