UnitedHealth Group (UNH +0.31%) is coming off a brutal 2025, when its stock lost a staggering 35% in value, despite the markets enjoying a fairly strong year with the S&P 500 climbing by 16%. Historically, UnitedHealth has been a fairly dependable and safe stock to hang on to, but last year, it faced many concerning issues.

In recent months, however, the stock has been rising as investors appear to be more bullish on it, given its low valuation. What should you do with the stock in 2026: buy, sell, or hold?

Image source: Getty Images.

Is UnitedHealth back on the right track?

When the company last reported earnings in October, it gave investors some good news with the announcement of not only strong 12% revenue growth, but also that it was raising its earnings outlook for the full year. Several months earlier, the company delivered poor results, pulled its guidance, and also changed its CEO, resulting in an all-out crash for the stock.

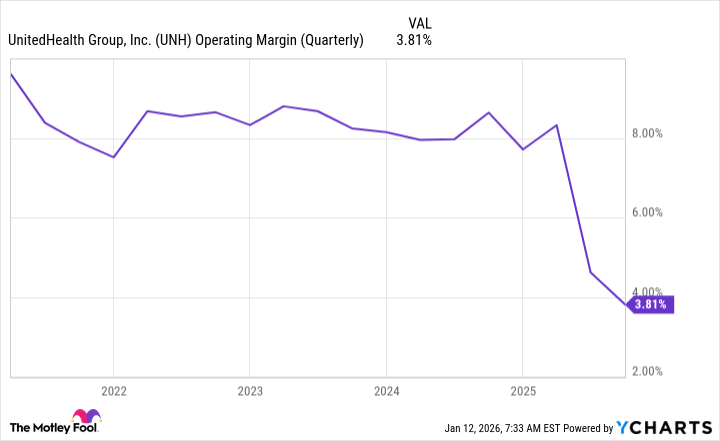

However, the business is still battling high expenses as its medical care ratio was 89.9% in the most recent quarter. Just two years earlier, that percentage was only 82.3%. That indicates how high the health insurer's medical expenses are in relation to the premiums it collects. That number heavily affects its operating margin, which has deteriorated in recent years.

Data by YCharts.

Although the company's operations appear to be stabilizing, it may simply be that investors and analysts have adjusted to lower expectations, rather than the business doing a whole lot better. Investors also appear to be adjusting the premium they're willing to pay for the stock.

Is UnitedHealth's stock too cheap to pass up?

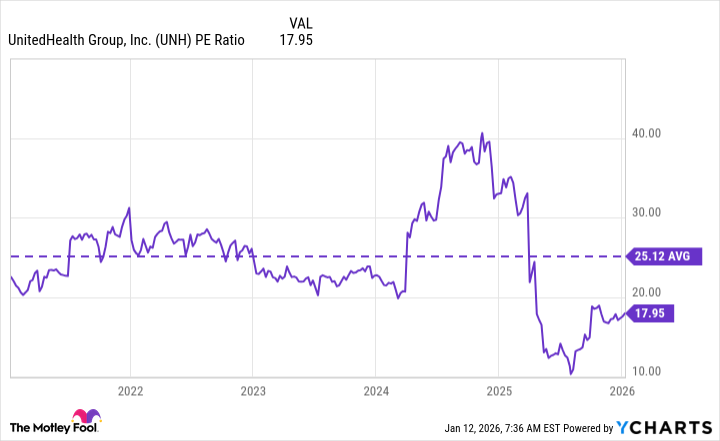

Due to last year's steep sell-off, UnitedHealth Group stock is now trading at a much lower price-to-earnings (P/E) multiple than in the past. At 18 times earnings, the multiple is well below UnitedHealth's five-year average of 25.

Data by YCharts.

This discounted valuation can offer investors a bit of a margin of safety with the investment; in the event that the company may not do well in the future, the sell-off may not be as drastic as it was in 2025.

But investors may also be worried about the Department of Justice investigating the company's billing practices. There was also a report last year that UnitedHealth allegedly paid nursing homes not to transfer patients, which would have reduced its expenses. Between the high costs, bad press, and the potential for legal repercussions, the stock's P/E multiple may not rise much higher until investors' concerns about at least some of these issues subside.

NYSE: UNH

Key Data Points

The stock could still make for a good buy in the long run

I'm optimistic that UnitedHealth's stock could do well this year as the market has appeared to adjust to the realities of higher expenses for the company. There wasn't a large sell-off the last time UnitedHealth posted earnings, despite its costs being high and margins being low. The discount in its valuation can help offer an incentive as well. Plus, a dividend that yields 2.6% (which is more than double the S&P 500's average of 1.1%) can boost your returns.

If you're a long-term investor who's willing to be patient and hold onto shares for multiple years, I think UnitedHealth Group can be a good stock to own. It may take some time for the company's earnings to recover and for its margins to improve, but overall, this is still a big player in the healthcare industry with a lot of room to grow in the future.