What a difference a few years can make. Macy's (M 3.68%), a one-time poster boy for the retail apocalypse, saw its share price not only grow across 2025 (by over 30%) but also convincingly outperform the broader market as the bellwether S&P 500 index increased at a 16% clip. That was the first year since 2022 that the stock has achieved either feat.

Macy's was something of a cautionary tale for much of this decade. What went right for the famous retailer in 2025 to turn investor sentiment around so dramatically? Let's explore.

Apocalypse avoided

For a time in 2024, it appeared as if Macy's would be sold. Two strategic investors, Arkhouse Management and Brigade Capital Management, teamed up and began accumulating Macy's shares in late 2023. Drawn by Macy's considerable real estate holdings, the pair subsequently made increasingly pricey bids to buy the company. All were effectively rejected.

Image source: Getty Images.

Instead, Macy's management decided to move forward with its "bold new chapter" strategy, which involved selling off assets like that real estate and reducing the company's still considerable brick-and-mortar presence. The retail apocalypse, after all, had claimed numerous retail peers that retained large networks of physical stores.

To its credit, throughout 2025, Macy's largely succeeded in these tough-love goals. It's not far from its aim of shuttering 150 stores by the end of the current fiscal year, leaving the most productive locations. It also actively divested unwanted holdings, especially land, to hungry buyers like shopping mall real estate investment trusts (REITs).

Macy's was anticipating it would earn $150 million from property sales this year under the strategy. That would add to the approximately $275 million it collected from the activity in 2024.

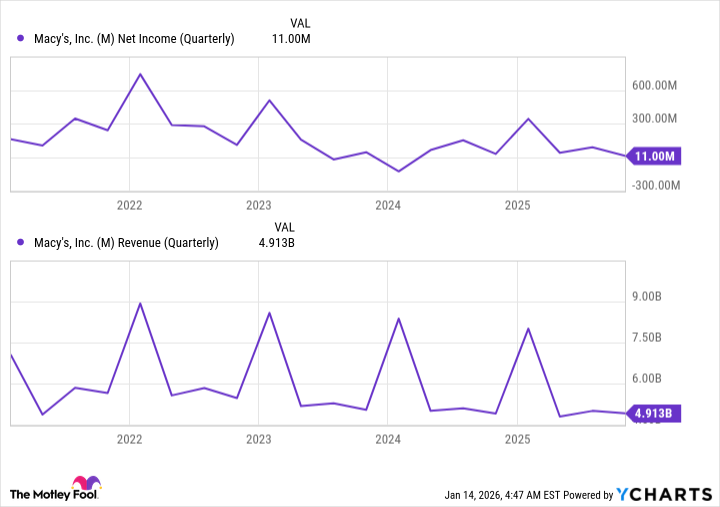

Although revenue has generally been waning lately, due in no small measure to those store closures, Macy's bottom line has landed in the black -- if not always impressively so -- in recent quarters.

M Net Income (Quarterly) data by YCharts

There are some luminous bright spots within these results, particularly Bloomingdale's 9% year-over-year increase in comparable sales in last year's third quarter. Meanwhile, in the same period, Macy's Bluemercury cosmetics retail brand posted its 19th consecutive rise in "comps."

NYSE: M

Key Data Points

On the right track, at least

I like the direction in which Macy's is heading. That slimming-down strategy of bold new chapter is sensible, and management has done a solid job of implementing it. The company is effectively transforming into a more exclusive and efficient retailer, and it seems customers are responding positively to the shift.

Yet I'm not convinced that Macy's can return to its glory days as a retail powerhouse with a commanding presence in every major American market. The consistent profitability of recent times is encouraging, sure. However, I think the company will need to show reliable growth in both that metric and on the top line for this stock to really pop with investors.