It's been a tough three years for energy stocks. After surging during the COVID-19 pandemic, prices of crude oil and natural gas have both fallen since the middle of 2022, dragging many of the sector's stocks lower.

There's no end in sight either. Indeed, the U.S. Energy Information Administration predicts crude oil prices will sink to an average of about $55 per barrel this year and next, down from 2025's average of $69, further threatening the business's profit margins.

If you're an income-minded investor who can look a little further down the road, though, oil giant BP (BP +0.65%) may be a great "forever" name to step into while its 15% pullback from its early 2023 peak has pumped its forward-looking dividend yield up to a healthy 5.6%.

Image source: Getty Images.

More longevity than you might expect

Rumors of the oil and gas business's death have been greatly exaggerated. The so-called "peak oil" pivot (where daily consumption of crude oil begins to permanently dwindle)? It's been pushed back to 2050, according to the International Energy Agency, jibing with outlooks from OPEC as well as industry powerhouse ExxonMobil. And even then, we'll still need plenty of oil for the next several decades. BP's got the assets it needs to deliver for this time frame.

That being said, perhaps the chief reason income investors might want to jump into this energy name right now is that it's already managing the inevitable -- even if lengthy -- shift away from fossil fuels and toward the aforementioned renewables.

Case(s) in point: BP's partnership with JERA Nex is designed to develop offshore wind farms. It can currently generate on the order of 1 gigawatt, but plans for eventual power production of 13 gigawatts. That's enough electricity for roughly 10 million homes, or more relevantly now, several data centers. Meanwhile, Lightsource BP is working on generating and storing solar power for use by institutional clients, including utility companies.

NYSE: BP

Key Data Points

It's still a relatively small business for BP, and one that hasn't yet paid off. In fact, the company recently announced it would be booking a noncash impairment of between $4 billion and $5 billion for its low-carbon business, reminding investors just how challenging the transition from fossil fuels to renewables can be.

BP is still wisely preparing for this future, though, recognizing that it's better to be proactive rather than reactive ... even if it means the occasional setback.

Perhaps more important to income investors, the renewables business that it's building is also one that -- like its oil and gas business -- will generate recurring revenue, and therefore support continued dividend payments.

Not the best, but one of the better

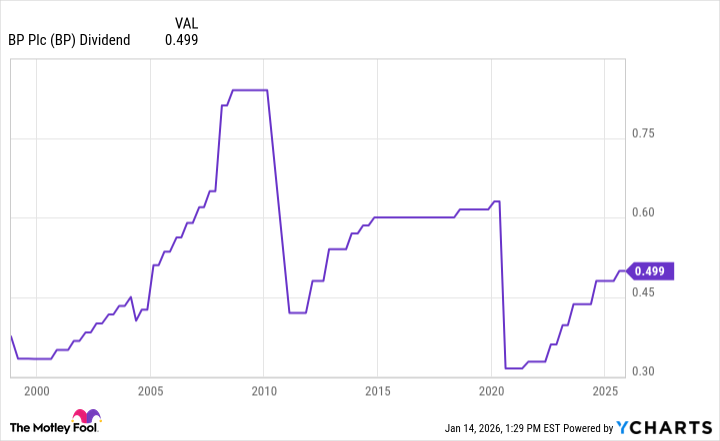

There is one arguable "catch" with this income stock's dividend. That is, it's not consistent. Although it generally rises, its per-share payouts tend to reset when crude prices suffer jolting setbacks, as they did in 2010, and then again in 2020 (and as most energy names do).

Data by YCharts.

So, if you need a permanently predictable dividend payment, this ticker might not be the best one to start with or the only one to hold.

With a strong starting yield of 5.6% and a compelling long-term future, though, BP certainly wouldn't make for a bad third or fourth holding in an income portfolio.