Although Amazon (AMZN +0.40%) has historically been a poster child for growth stocks, its performance in recent years has been underwhelming by most standards. In 2025, its stock finished the year up 5%, underperforming every other "Magnificent Seven" stock, as well as indexes like the S&P 500 and Nasdaq Composite.

Despite the disappointing year, I'm not ready to throw in the towel on Amazon. In fact, now seems like a good time to double down on the stock, as the overall market seems to be underappreciating it. If you're considering investing in Amazon, here are three reasons you should.

Image source: Amazon.

1. Its e-commerce is becoming more profitable

The average person knows Amazon for its e-commerce business, but they may not be aware of how much money it has historically lost in that business. Amazon generates revenue through e-commerce but relies on other segments to drive profits.

Now, Amazon's e-commerce business seems to be turning the corner and is heading toward more sustainable profitability. The reason is robotics and automation. Unfortunately, this has cost many people their jobs, but from a business standpoint, these investments are poised to save Amazon billions in operating costs.

By the end of this year, Amazon is estimated to have 40 robot-equipped fulfillment centers, saving the company as much as $4 billion, according to research by Morgan Stanley. Morgan Stanley also estimates that Amazon could save about $10 billion annually if 30% to 40% of its U.S. orders were to run through its next-gen warehouses by 2030.

In mid-2025, Amazon said that it had deployed more than 1 million robots across its global fulfillment network.

NASDAQ: AMZN

Key Data Points

2. AWS is increasing its computing capacity

Amazon Web Services (AWS) -- Amazon's biggest profit maker and the world's largest cloud platform -- came under intense scrutiny during the past year as its growth slowed and other platforms, such as Microsoft's Azure and Alphabet's Google Cloud, gained market share.

Considering AWS's size, the slowdown in revenue growth wasn't totally unexpected. Even so, 17% to 20% year-over-year (YOY) growth (which it accomplished during the past four quarters) isn't something that should cause investors to ring the alarm and jump ship. Although less than other growing platforms, that's still decent.

Amazon has been investing heavily in AWS, making sure the platform is positioned to meet growing demand during the artificial intelligence (AI) arms race. In the past year or so, it has added 3.8 gigawatts of computing capacity, with plans to double capacity through 2027.

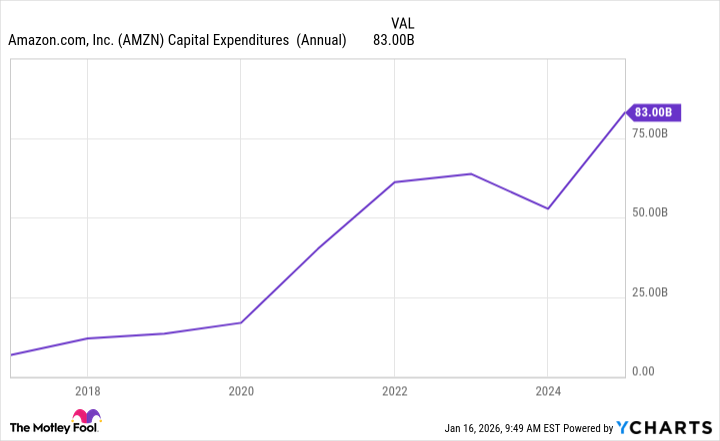

This is important because more computing capacity lets AWS begin clearing out its backlog and bring on more customers. If AWS were a highway, adding more computing capacity is like adding more lanes. Amazon's 2025 capital expenditure (capex) will likely exceed $125 billion, which would be $42 billion more than it spent in 2024. It's a lot, but even if, or when, AI demand slows, these investments will pay off long term as AWS continues to power a large share of the internet.

AMZN Capital Expenditures (Annual) data by YCharts

3. A lucrative business is emerging for Amazon

E-commerce and AWS rightfully get most of the attention, but advertising is quietly becoming a lucrative moneymaker for Amazon. In the third quarter of 2025, it generated $17.7 billion in revenue, up 24% from a year ago. It has been Amazon's fastest-growing segment in recent quarters.

Amazon has tons of data on millions of customers, including their shopping, viewing, browsing, and listening habits. This is an advantage when it comes to predicting behavior and enabling advertisers to run more targeted ad programs. It also allows advertisers to capture eyeballs on Amazon.com, Prime Video, Twitch, Freevee, and across its device ecosystem.

Amazon won't reach Google or Meta Platforms' scale in advertising in the foreseeable future (if ever), but for its business, having a third profit center is the key to investing in other lower-margin, risky, or expensive businesses.