I'd be willing to bet my last dollar that if you've even remotely peeped at the news or social media over the past year, you've heard about artificial intelligence (AI). It has become an inescapable topic, and the hype has transformed many companies and pushed stock prices up to record highs.

Many of the world's top AI stocks delivered impressive gains in 2025, but Amazon (AMZN 1.45%) lagged behind. The worst performer among the "Magnificent Seven," it finished the year up only around 5%. But I think it's ready to change the narrative again in 2026.

Image source: Amazon.

Amazon is playing the long game

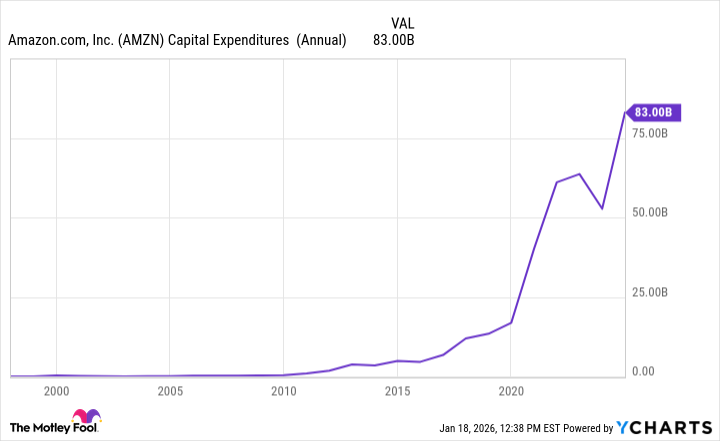

Amazon's stock struggled in large part because investors grew impatient with the disconnect between how much the company was spending and how much it was receiving on its investments. For 2025, management was guiding for capital expenditures of around $125 billion -- the highest in the company's history, and one of the highest annual capex budgets of any company, period.

While companies like Nvidia and Microsoft are already seeing benefits from their investments, Amazon's payoff seems to be further down the road. It has been spending on developing its own custom AI chips, building out data centers, and buying energy sources that can supply the massive electricity demands of those data centers.

These are moves that may not show up in its next earnings report, but they're keys to Amazon's long-term competitive advantage. By designing its own application-specific integrated circuits, it will reduce its reliance on Nvidia and make in-house AI model development easier. And by acquiring power production capacity, it reduces its dependence on utility companies. I think investors will become more appreciative of that this year.

AMZN Capital Expenditures (Annual) data by YCharts.

AWS growth should pick back up

The largest share of the company's massive capital outlays has gone to Amazon Web Services (AWS). The more cloud computing capacity AWS has, the more customers it can take on and support, and the more efficiently the company can run its own AI tools and services.

AWS hit a rut for a bit, but its 20% revenue growth in the third quarter was an encouraging sign that it could be picking up momentum again -- especially as it now has more capacity available, which will allow it to turn more of its $200 billion backlog into revenue.

It also recently struck a $38 billion deal with ChatGPT developer OpenAI. Under the deal, announced in November, AWS will provide processing power to ChatGPT and supply OpenAI with access to the AI accelerator clusters it needs to continue developing its technology.

With all this in mind, I expect a much better performance from AWS in 2026.