Tobacco giant Altria Group (MO +2.62%) is in a difficult position. The company has long mitigated the detrimental effect of declining smoking rates on its revenue by raising product prices. Now, revenue falling anyway seems to suggest that the approach has stopped working.

Even more puzzling, the stock price has trended higher since the beginning of 2024 despite this new development, and despite the share price gain, the stock now sells at a price-to-earnings (P/E) ratio of 12. The conflicting data has some investors questioning whether that makes the stock too cheap to ignore, as well as asking whether they should avoid it.

Image source: Getty Images.

Altria and its dividend

When it comes to surviving strong headwinds, it is difficult to find a story that surpasses Altria's. The Surgeon General released a report in 1964 highlighting the dangers of smoking. Between declining usage and hundreds of billions of dollars in legal settlements related to its product, it might be easy to dismiss the tobacco company's stock on the surface.

However, since then, both the stock and its dividend have moved higher for most of that history. The annual payout, now at $4.24 per share, has a dividend yield of 6.8%. Altria's dividend has also risen every year since 2009 and increased annually between 1989 and 2006.

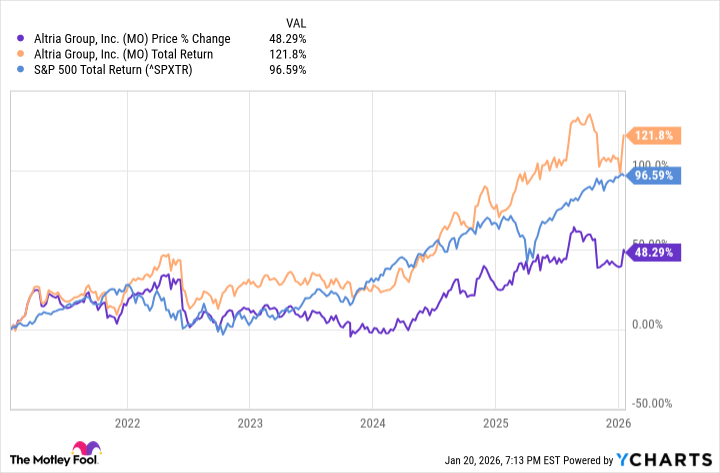

Unfortunately, the tobacco giant has delivered a mixed performance more recently. Altria beat the S&P 500 when including dividend returns, though the stock itself dramatically underperformed the market.

Data by YCharts.

Its failed attempts to counter the decline in smoking may be the heart of the problem, considering what Altria owns. In 2018, it paid $12.8 billion for a 35% stake in e-cigarette maker Juul. Amid issues with lawsuits and regulatory crackdowns, it traded that stake for some of Juul's intellectual property and invested in e-cigarette market NJOY.

Also, in 2019, it invested 2.4 billion Canadian dollars ($1.7 billion) for a 45% stake in cannabis company Cronos Group. Today, Cronos' market cap is under $1 billion.

Such missteps cost the company, and now, sustaining the dividend is becoming a struggle. Over the trailing 12 months, it generated around $9.2 billion in free cash flow. That covered the $6.9 billion in dividend costs but left relatively little cash available for other purposes.

Hence, unless Altria can reverse the revenue declines, it could endanger its ability to continue raising the dividend.

NYSE: MO

Key Data Points

Is Altria stock too cheap to ignore?

Given Altria's challenges, investors can likely afford to ignore the stock despite a low valuation.

On the surface, its 6.8% dividend yield may look appealing when considering its P/E ratio of 12. Unfortunately, price increases are failing to sustain revenue levels as more people quit smoking. Moreover, attempts to start new business lines in related industries cost the company billions. As a result, its rising dividend claims a large majority of its free cash flow.

Admittedly, it is not too late to succeed with e-cigarettes or even cannabis, and it is also possible that tobacco use will stop declining. Nonetheless, unless conditions in its business turn around soon, this is likely not a stock worth buying, even at its current valuation.