Tech companies are investing heavily in quantum computing, which uses quantum mechanics to develop faster computing systems. One pure-play quantum computing company is the aptly named Quantum Computing (QUBT -3.63%), or QCi for short. It develops photonics technology that manipulates particles of light and operates at room temperature, unlike the superconducting technology favored by many quantum computing companies.

Quantum Computing stock has soared over the last three years, rising 591% (as of Jan. 22). Despite those amazing returns, I won't touch it because of a few serious risks.

Image source: Getty Images.

It trades at a staggering premium

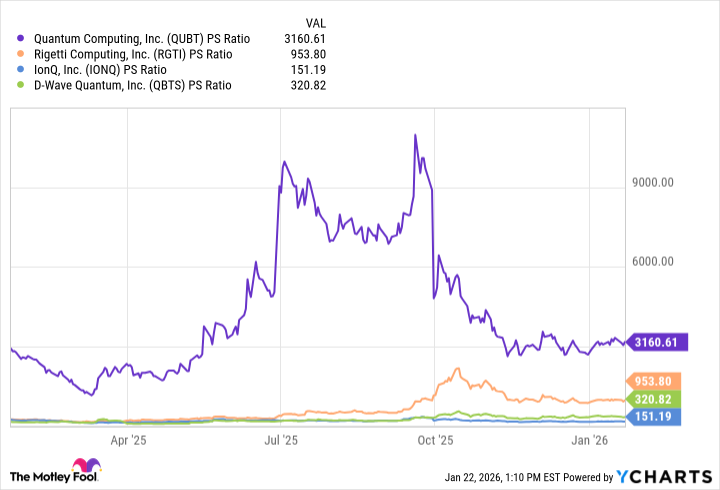

QCi hasn't generated much revenue -- just $546,000 over the trailing 12 months (TTM). With a market cap of $2.7 billion, it currently trades at over 3,000 times trailing sales.

For comparison, Nvidia has generally traded between 20 to 40 times sales in recent years. Even compared to the other pure-play quantum computing stocks, QCi is an outlier. Here's how its price-to-sales (P/S) ratio compares to D-Wave Quantum, IonQ, and Rigetti Computing.

QUBT PS Ratio data by YCharts

In fairness, QCi's photonics technology can operate at room temperature and requires low power compared to other quantum systems, which are important advantages. However, it's still unclear which quantum computing method will prove to be the most effective, so QCi's cost is hard to justify.

A history of share dilution

Another reason QCi trades at a premium is its robust balance sheet, with over $1.5 billion in cash and investments. Given the high research and development (R&D) costs of quantum computing, cash reserves are crucial to avoid running out of money.

The problem is that much of QCi's cash reserves have come from issuing new shares. Over the last three years, the company's outstanding shares have quadrupled, from about 60 million to 224 million. If you invested in QCi three years ago, your current stake would be about one-fourth of the size it was when you started.

NASDAQ: QUBT

Key Data Points

Share dilution can work out well for everyone if it generates cash that the company uses to grow. But as mentioned earlier, QCi's earnings are still very small. The fact that it has repeatedly issued new shares to raise money is a concern for investors.

Fierce competition

QCi could reward shareholders if its photonics systems become the leading quantum computing technology. You could say the same for D-Wave, IonQ, and Rigetti -- they're all trying to solve the same problem in a different way. And those are just the pure-play options. Several tech giants are investing in quantum computing, including Alphabet, International Business Machines, and Nvidia.

I'm not convinced QCi will be the winner in this space, especially considering its revenue is a fraction of its closest competitors. With all the competition, the sky-high valuation, and the risk involved, QCI is a stock I'm avoiding.