Taiwan Semiconductor Manufacturing (TSM 1.26%) is coming off another solid year, gaining 54% in 2025. It has many tailwinds and an excellent business model, and Wall Street rates it a buy -- with 98% of 49 covering analysts calling it one.

However, the average consensus target price is $408.50, or a 25% increase over the next 12 to 18 months. While that might sound encouraging, I think Wall Street is wrong; I think TSMC can go much higher.

Image source: Taiwan Semiconductor.

AI needs TSMC

TSMC is a foundry, and it makes the semiconductors that drive much of today's technology, from smartphones and autonomous vehicles to the all-important artificial intelligence (AI). The company works with nearly every high-profile AI developer, counting names like Nvidia, Amazon, and Apple as clients. It's not the only game in town, but TSMC has the dominant position, and its partners rely on it to keep their platforms competitive.

Companies like Amazon, Meta Platforms, and Alphabet all said they were planning to increase their AI spend this year, which altogether equals several hundred billion dollars. TSMC is also raising its capital expenditure (capex) spend to meet this increasing demand, and management said that increased spend correlated with increasing opportunities. It's guiding for sales to increase 30% in 2026.

NYSE: TSM

Key Data Points

The stock will follow the results

A stock could move based on a variety of factors, and sometimes it doesn't seem to make logical sense; that's what often creates opportunities for astute investors.

However, in general, a stock moves along with performance. Wall Street has certain expectations for each company, and how well the company grows as well as how well it meets expectations will generally dictate where the stock goes. That's where valuation fits in, since the higher a company's earnings, for example, the higher the stock can grow without exceeding a reasonable P/E ratio.

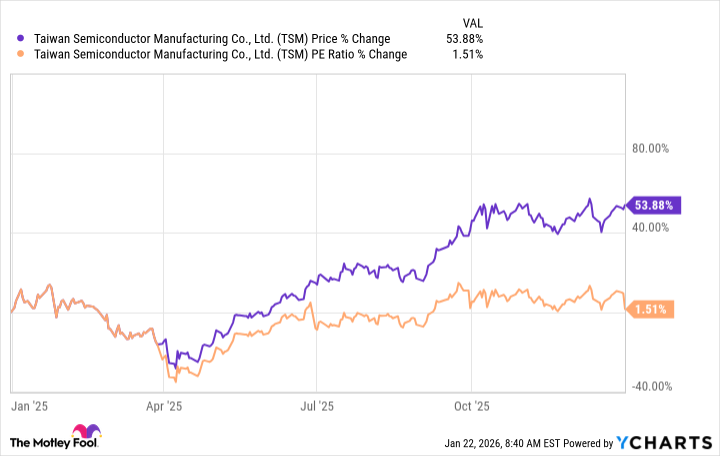

In TSMC's case, it trades at a P/E ratio of 31, which is quite attractive for a company growing as fast as it is and with as many opportunities. The stock has gained 54% over the past year while the P/E ratio has remained essentially flat.

That means it should easily jump higher with increased sales and earnings.

Wall Street expects 2026 earnings per share (EPS) of $13.05 on average, up from $10.65 in 2025, a 23% increase. It's also looking for a 31% increase in sales, in line with management's guidance. However, the company beat on EPS for the past four quarters, and by quite a bit, including $0.16 in the fourth quarter.

The highest price target for TSMC stock is $520, which is 59% higher than today's price, and I think there's a good chance that it can reach that price over the next 12 to 18 months.