Artificial intelligence (AI) has been a huge source of stock market returns over the last few years, but not every player in this space has been a winner. For example, SoundHound AI (SOUN 2.52%) stock suffered a 49% collapse last year as investors decided its sky-high valuation was no longer palatable.

SoundHound is a leading developer of conversational AI software, which is now being used by some of the world's biggest brands in industries like hospitality, automotive manufacturing, healthcare, and more. The company's revenue is growing at a lightning-fast pace, but will that be enough to spark a recovery in its stock price this year?

Image source: Getty Images.

A leader in conversational AI

SoundHound's portfolio of conversational AI products is expanding. For car manufacturers, its Voice AI platform is a white-label solution for deploying custom AI assistants, which can give drivers information about the weather -- or even the stock market -- on command. Manufacturers can give their assistants a unique personality to suit their brands, so they can differentiate themselves from the competition.

For fast-food restaurants, SoundHound offers products like Dynamic Drive-Thru and Dynamic Kiosk, which can autonomously take customers' orders from their cars and in-store. Then there's Employee Assist, which is like an on-demand handbook for workers. It's voice-activated and stands ready to help with anything from store policies to preparing menu items. Panda Express, Applebee's, and Krispy Kreme are just a few of the top restaurant chains using SoundHound's products.

SoundHound also entered the agentic AI race in 2024 when it acquired a company called Amelia. Businesses in almost any industry can use the latest Amelia 7 platform to create custom AI agents capable of handling incoming customer-service queries, whether they come by phone or online. Global financial services giant BNP Paribas used Amelia to create an agent called NOA, which can update clients on the status of their investments and even retrieve historical statements on command.

SoundHound's revenue is soaring

SoundHound will report its operating results for the final quarter of 2025 in February. According to management's guidance, its total revenue for the year should come in somewhere between $165 million and $180 million. The midpoint of the range ($172.5 million) would represent a whopping 103% growth, compared to 2024.

NASDAQ: SOUN

Key Data Points

However, SoundHound's top line is growing so quickly because it's spending very heavily on growth initiatives. For instance, its marketing costs nearly doubled year over year during the third quarter of 2025 (ended Sept. 30), and administrative costs jumped by 43%. As a result, the company posted a net loss of $109.2 million for the period on a generally accepted accounting principles (GAAP) basis.

The loss was more palatable at $13 million on an adjusted (non-GAAP) basis, after excluding one-off and non-cash expenses like those relating to acquisitions. However, with just $269 million in cash on hand as of Sept. 30, SoundHound can't afford to keep burning significant amounts of money or it will have to raise capital in the next couple of years, which will dilute existing shareholders.

Despite its crash in 2025, SoundHound stock is still expensive

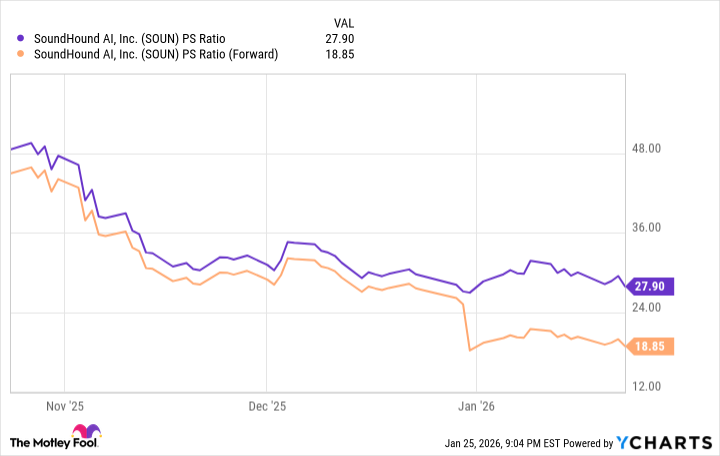

SoundHound stock is trading at a price-to-sales ratio (P/S) of 27.9, as of this writing. While that's far more reasonable than its peak of over 100, I would argue it's still relatively expensive, considering Nvidia stock trades at a lesser P/S ratio of 24.6.

Nvidia is one of the AI industry's highest-quality companies. It's producing significant growth at the top and bottom lines, has a rock-solid balance sheet, and a track record of success spanning decades. I don't think SoundHound deserves to trade at a premium to Nvidia for those reasons.

However, Wall Street's consensus estimate (provided by Yahoo! Finance) suggests SoundHound could generate $230.2 million during 2026, placing its stock at a forward P/S ratio of 18.8.

SOUN P/S Ratio data by YCharts.

Therefore, if we assume Wall Street's estimate is accurate, I actually think there's room for SoundHound stock to move marginally higher during 2026. Investors who are willing to hold the stock for a longer-term period of three to five years will probably have a much higher chance of earning a positive return because it will give SoundHound's business more time to mature.

In summary, there's a reasonable chance SoundHound stock reverses some of its losses from 2025 as this year progresses. However, given the company's history of extreme volatility, investors might want to keep their positions small, in order to manage risk.