Shares of Figma (Nasdaq: FIG) continued to fall last month even though there was little news out on the design-focused cloud software stock. Instead, Figma, like other software-as-a-service (SaaS) stocks, has fallen sharply amid fears that AI will disrupt software by making it easy to substitute for things like the web design that Figma enables.

Those fears hit a fever pitch toward the end of the month as SaaS leaders like Microsoft, ServiceNow, and SAP all fell sharply after reporting earnings.

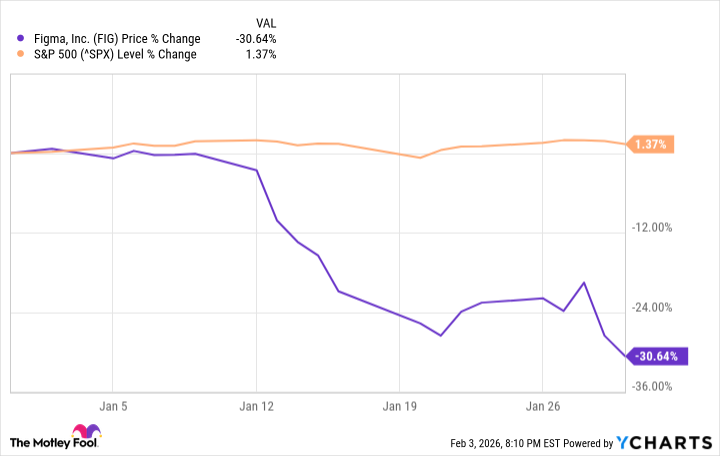

According to data from S&P Global Market Intelligence, the stock fell 31% last month. As you can see from the chart below, the stock slide picked up speed as the month went on.

Why Figma keeps falling

There was little company-specific news out on Figma last month, though a number of Wall Street analysts updated their price targets on the stock.

Most analysts maintained a bullish stance on the stock even as the price came under pressure. Wells Fargo, for example, upgraded the stock to overweight, saying it deserves a premium given its leadership status in product design and track record of efficient growth.

What seemed to accelerate the stock's sell-off was the round of earnings reports at the end of the month from Microsoft, ServiceNow, and SAP. While those companies mostly turned in results in line with expectations, there were some questions about the guidance and Microsoft's sharp increase in capital expenditures, as investors are starting to doubt whether these companies will get a return on their investment.

Figma rival Adobe has also fallen sharply, losing 16% of its value last month, showing that sell-off was less about Figma, and more a result of pressure on the sector.

Image source: Getty Images.

What it means for Figma

Part of the challenge facing Figma and its peers is that software stocks have historically been very expensive, often trading for 10 times or even 20 times sales.

Even after the sell-off, which continued into the first days of February, Figma still trades at 12 times sales, and the stock is down by more than a third from its IPO price six months ago and 85% from its peak in the euphoria shortly after the IPO.

In my opinion, Figma looks oversold at this point. This is a healthy business that is both growing rapidly and historically profitable on a generally accepted accounting principles (GAAP) basis, and knowing how to use Figma is an in-demand skill.

Disrupting Figma and its software peers, if it happens, will take years. We'll learn more when it reports fourth-quarter earnings on Feb. 18. Analysts are expecting revenue of $293.2 million and adjusted earnings per share of $0.06.