It's been a brutal start to 2026 for Microsoft (MSFT +2.38%) investors. In just over a month, the stock is down about 18% year to date as of this writing. Even worse, the stock is down about 28% from a 52-week high of $555.45. The tech stock's decline comes as many software stocks are taking a beating as investors reassess their valuations and the risks in an era of AI (artificial intelligence).

But it's not like the underlying business is struggling. Not only did the tech company just report another strong quarter of double-digit top-line growth, but the software giant's operating income rose by a strong double-digit rate even as the company invests heavily in growth opportunities in cloud computing and AI.

So, with the underlying business doing extremely well even as its stock is getting pummeled, is this a buying opportunity for investors?

Image source: Getty Images.

Accelerating growth

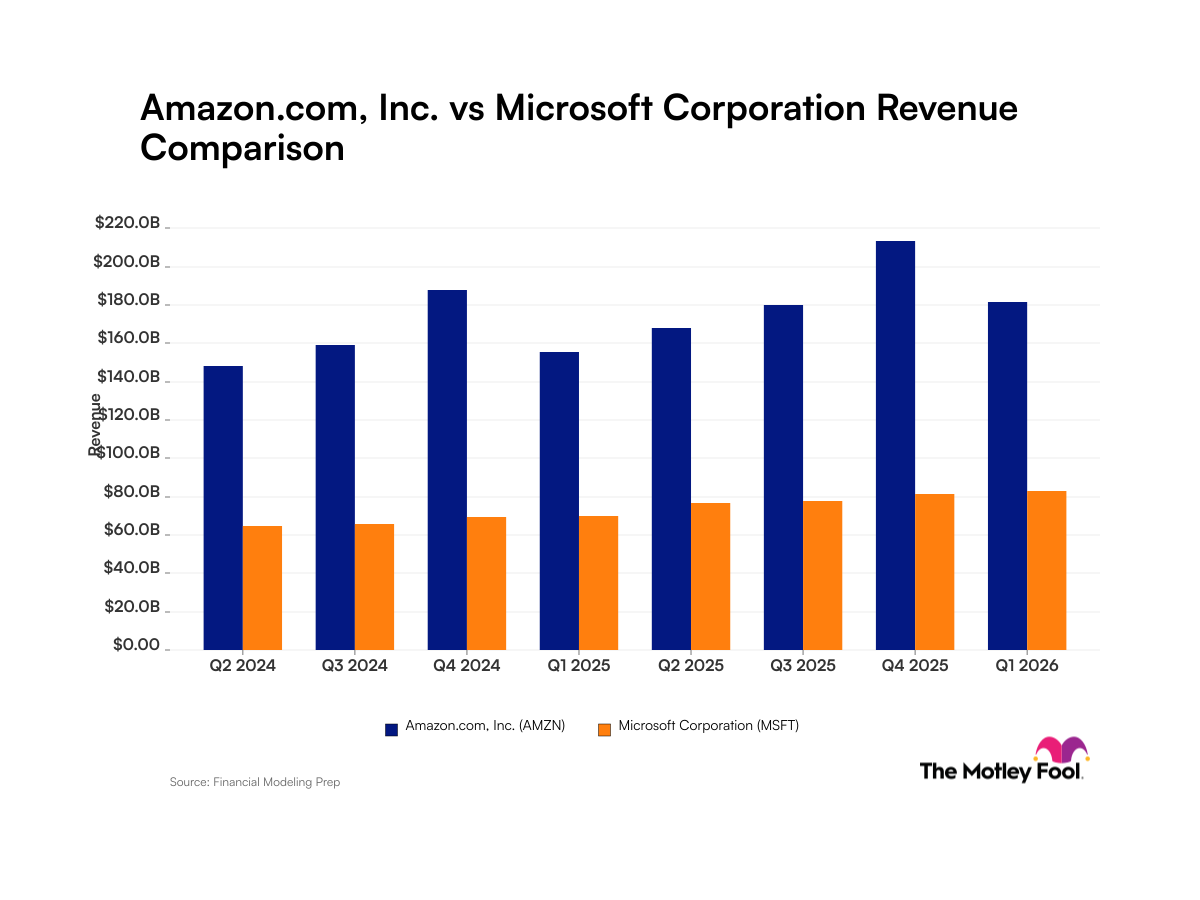

The company's most recent quarter did a good job of capturing the company's business momentum. Microsoft's fiscal second-quarter revenue rose 17% year over year, or 15% on a constant-currency basis. And operating income rose 21% year over year, or 19% in constant currency, to $38.3 billion.

Highlighting the robustness of Microsoft's business, its growth drivers remain broad-based. Its fiscal second-quarter revenue in its productivity and business processes segment, which includes Microsoft 365 Commercial and consumer products and cloud services, LinkedIn, and Dynamics products and cloud services revenue, rose 16% year over year to $34.1 billion.

Additionally, Microsoft's second-largest segment, intelligent cloud, which includes its important and fast-growing cloud computing business, Azure, saw revenue rise 29% year over year to $32.9 billion during the quarter. Its "Azure and other cloud services" revenue, specifically, climbed 39% year over year.

But there was a weak spot, though it was in Microsoft's smaller "more personal computing" segment. The segment contributed $14.3 billion in revenue during the period and includes revenue from Windows original equipment manufacturing (OEM) and devices, Xbox, search, and more saw revenue decline, albeit not much. This segment's revenue decreased 3% year over year.

A huge backlog

Even more, there could be even faster growth for Microsoft on the horizon -- particularly in cloud computing. Fueled by its fast-growing demand for AI-capable computing, Microsoft revealed in its fiscal second quarter that its commercial remaining performance obligations (RPOs) hit $625 billion during the period, up a mind-boggling 110% year over year.

Of course, the company won't be able to plow through its backlog immediately, but it did tell investors in its earnings call that it expects 25% of this backlog (about $156 billion) to be recognized as revenue in the next 12 months.

And for investors looking for exposure to AI, they'll get it with Microsoft. The company disclosed that about 45% of its RPO balance is from OpenAI, the creator of ChatGPT.

NASDAQ: MSFT

Key Data Points

Microsoft stock: Buy, sell, or hold?

So, with all of this business momentum, is now a good time to buy Microsoft stock?

While shares don't appear overvalued at their current valuation, they don't look like a clear buy either.

Sure, the stock's current price-to-earnings ratio multiple of about 25 doesn't look very expensive. But investors should note that the company's big growth opportunities in cloud and AI come with massive costs. This is becoming clear in recent quarters -- particularly in fiscal Q2. During the period, Microsoft's capital expenditures were $37.5 billion, up about 66% year over year. With a large portion of this coming from investments in infrastructure to support AI computing, such as graphics processing units (GPUs) and central processing units (CPUs), this is a preview of the heavy investment cycle required to support its effort to capitalize on its massive commercial backlog. As capital expenditures continue to rise rapidly, they will eventually show up as depreciation on Microsoft's income statement and could weigh on the company's margins.

All of this is a way of saying that, given the heavy investment cycle Microsoft is embarking on, shares look more like a hold than a buy at the moment. But for investors who really believe Microsoft's AI investments will pay off in strong, profitable growth over the long term, this may be a good opportunity to at least start a position in the stock.