ASML Holding (ASML 2.61%) is one of the most important companies in the global semiconductor supply chain. It has a monopoly in advanced chipmaking equipment manufactured using extreme ultraviolet (EUV) lithography, the technology that enables chipmakers and foundries to print chips sized 7 nanometers (nm) or smaller.

Chips manufactured using these advanced process nodes are more powerful and power-efficient, as they pack more transistors into a smaller area. As a result, these advanced chips are now powering key artificial intelligence (AI) applications such as data centers, smartphones, and personal computers (PCs). Not surprisingly, demand for ASML's machines has been increasing rapidly, driven primarily by robust spending on AI data centers.

This explains why investors have been buying ASML stock hand over fist of late. The semiconductor stock has shot up by 96% in the past six months. Importantly, it has room to run higher from current levels even after its terrific rally. Let's see why that's likely to be the case and check how fast each share of ASML could be worth $2,000.

Image source: ASML.

ASML's bookings are accelerating thanks to the AI boom

ASML released its fourth-quarter 2025 results on Jan. 28. The company's full-year revenue increased by almost 16%, while earnings rose by 28%. However, the important thing to note in ASML's latest quarterly results was the big spike in its bookings, which refers to the sales orders for which it has received written authorizations.

The company's net bookings landed at just over 28 billion euros in 2025, up by 48% from the previous year. So, ASML received more orders than it fulfilled last year. Management remarked on the latest earnings call that it is seeing "a notable increase and acceleration of capacity expansion planning across the large majority of our customer base."

CEO Christophe Fouquet added that the semiconductor industry's outlook has "improved notably over the last months specifically as related to the continued build-out of data centers and AI-related infrastructure." He pointed out that ASML's foundry customers have been ramping up the production of advanced chips to support the growing demand for high-performance computing and mobile applications.

At the same time, the booming demand for memory chips is another catalyst for ASML. The company says that its memory customers are adopting its EUV manufacturing process. All this explains why ASML is expecting a significant increase in revenue from sales of its equipment to foundries and memory manufacturers.

After all, ASML's customers, such as Taiwan Semiconductor Manufacturing and Micron Technology, are poised to significantly increase their capital expenditures this year, putting the Dutch company on track to exceed its 2026 revenue guidance of 34 billion euros to 39 billion euros.

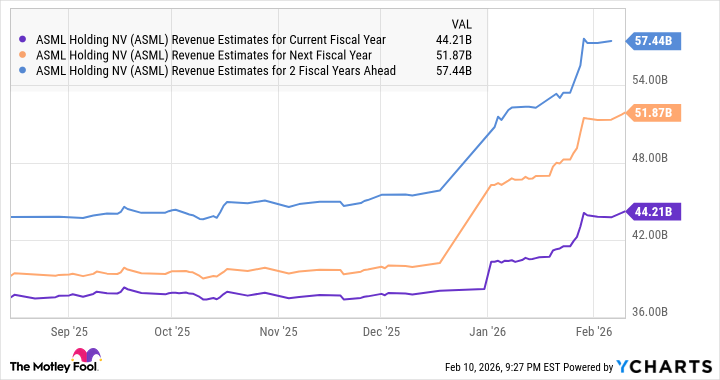

Analysts are already expecting ASML's revenue to slightly exceed the midpoint of its guidance to just over 37 billion euros, potential growth of 13% from 2025. More importantly, its growth is anticipated to accelerate next year, as is evident from the following chart (which shows amounts in U.S. dollar terms).

ASML Revenue Estimates for Current Fiscal Year data by YCharts

ASML could post $51.3 billion in revenue in 2027, up by 17% from this year's estimated revenue. Investors, however, shouldn't forget that ASML had a backlog of 39 billion euros at the end of 2025, which exceeds the midpoint of its 2026 revenue guidance. Also, spending on wafer and fabrication equipment is predicted to increase by 13% in 2026 and 12% in 2027, according to Mizuho Financial Group.

So, ASML could continue to land new orders at a healthy clip, setting the company up for stronger growth in 2026 and 2027 compared to what analysts are expecting.

It may not be long before the stock hits $2,000

We have seen that ASML's revenue is anticipated to increase by 13% this year and 17% in 2027. For comparison, ASML's top line increased by 16% last year, and the points discussed above suggest that it is capable of doing better than that going forward. Assuming ASML's top line increases by 18% in 2026 and 2027, its revenue could hit nearly $54 billion by the end of next year (using 2025's revenue of $38.7 billion as the base at the current exchange rate).

NASDAQ: ASML

Key Data Points

The stock is trading at 14.3 times sales, a premium to the U.S. technology sector's average sales multiple of 8. However, that multiple seems justified given the potential acceleration in ASML's growth and its sunny prospects amid a favorable AI infrastructure spending environment.

Let's say ASML is trading at 14.3 times sales at the end of next year and achieves $54 billion in revenue, its market cap could jump to $769 billion, an increase of 40% from current levels. That's very close to what ASML stock needs to jump from current levels to hit a stock price of $2,000, suggesting that it can achieve this milestone within the next two years.

However, don't be surprised to see the ASML shares jumping to $2,000 much sooner than next year, as the company's guidance seems conservative. Its actual growth could exceed its forecast, paving the way for a big jump in this AI stock in 2026.