Energy Transfer (ET +1.99%) is off to a strong start in 2026, with its stock price up about 14% as of this writing. With the company just reporting its Q4 results, let's look at why it is one of the most intriguing master limited partnerships (MLPs) to own right now.

NYSE: ET

Key Data Points

Solid growth ahead

While most investors are attracted to Energy Transfer's attractive forward yield of 7.2%, the company also has some of the best growth opportunities in the midstream space. The company is in the midst of two large-scale natural gas projects out of the Permian Basin, with the Hugh Brison Pipeline and Desert Southwest Pipeline. The former is 75% complete, with phase 1 expected to come online by the end of the year. Meanwhile, it just upsized the Desert Southwest project due to the strong demand from customers, with an in-service date of late 2029.

Image source: Getty Images.

The pipeline company will increase its capital expenditures (capex) this year to a range of $5 billion to $5.5 billion. That's up from the $4.5 billion it spent in 2025. It has said it expects a mid-teens return, or 6 times adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) build rate of these projects. That would be close to adding $90 million in incremental EBITDA once these projects come online and are fully ramped up.

Turning to its Q4 results, Energy Transfer's EBITDA in the quarter climbed by 8% year over year to $4.18 billion. It said that a favorable regulatory ruling around NGL (natural gas liquid) pipeline pricing led to a $56 million benefit in the quarter and that the ruling will have a small positive impact moving forward.

Distributable cash flow (DCF) to partners, which is operating cash flow minus maintenance capex, rose 3% to $2.04 billion, up from $1.98 billion a year ago. It paid out $1.15 billion in distributions in the quarter, good for a coverage ratio of nearly 1.8.

The company also slightly upped its full-year EBITDA forecast, taking it to a range of $17.45 billion and $17.85 billion, up from a prior guidance range of $17.3 billion to $17.7 billion. The increase was attributed to an acquisition made by its subsidiary, USA Compression. It continues to expect to raise its distribution by a 3% to 5% clip moving forward.

Is the stock a buy?

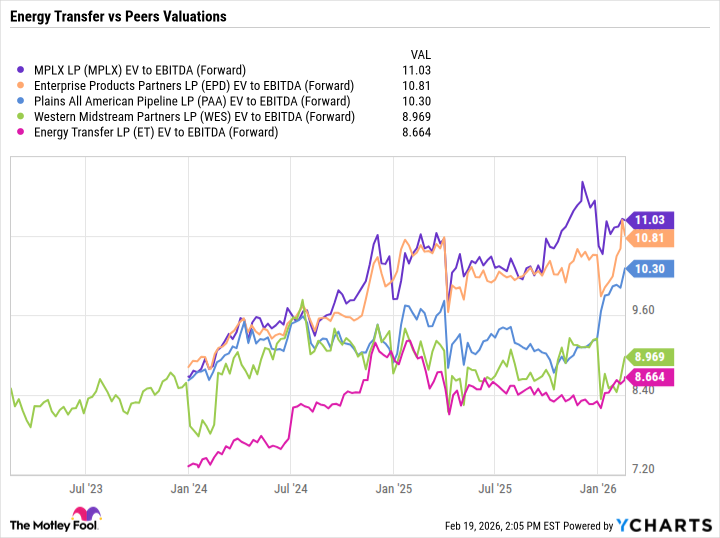

Energy Transfer is a great combination of a stock with a high yield that is well covered with solid growth opportunities ahead. Meanwhile, the stock is attractively valued, trading at an enterprise value-to-EBITDA (EV/EBITDA) multiple of just 8.6 times. That's one of the lowest valuations in the midstream MLP sector.

Data by YCharts.

In my view, Energy Transfer is the best stock in the midstream sector to buy right now.