CoreWeave (CRWV +3.31%) stock has been battered badly following the release of its fourth-quarter 2025 results on Feb. 26. Shares of the neocloud infrastructure company shed more than 18% of their value on the day following the earnings release, which isn't surprising when you take a closer look at its numbers.

Though CoreWeave's revenue was ahead of Wall Street's expectations, it posted a bigger-than-expected loss. Moreover, the guidance missed consensus estimates. It is easy to see why investors pressed the panic button, but this may have opened an opportunity for savvy investors to buy a top artificial intelligence (AI) stock on the cheap.

Image source: Getty Images.

CoreWeave's growth is poised to accelerate significantly

Hyperscalers and AI companies have been spending hundreds of billions of dollars to build AI data centers. CoreWeave is in the business of building dedicated AI data centers and renting out its computing capacity to hyperscalers such as Meta Platforms and Microsoft, as well as AI specialists such as OpenAI. It also offers managed services that enable customers to train and fine-tune models, run AI inference applications, and monitor their AI infrastructure from end to end.

NASDAQ: CRWV

Key Data Points

Not surprisingly, CoreWeave's business is booming. It reported a 168% increase in revenue in 2025 to $5.1 billion. The company ended the year with 850 megawatts (MW) of active data center capacity, up from 360 MW at the end of 2024. It added 11 new data centers in 2025, bringing the total count to 43. This aggressive capacity expansion is why CoreWeave's capital expenditures (capex) are growing much faster than its revenue.

The company plans to spend $30 billion to $35 billion in capex in 2026, more than double last year's outlay of $14.9 billion. The big jump in CoreWeave's capex will fuel the company's top-line growth, enabling it to convert more of its backlog into revenue.

CoreWeave finished 2025 with a revenue backlog of almost $67 billion, up by 342% over the year-ago period. It needs to add more data center capacity to fulfill this backlog, especially given that it has already allocated all of the additional capacity it is poised to bring online in 2026.

Another important point worth noting is that CoreWeave exited 2026 with 3.1 gigawatts (GW) of contracted data center capacity, which refers to the power capacity that the company has access to through its contracts with utility providers and power companies. CoreWeave aims to convert this contracted capacity into active capacity by the end of 2027.

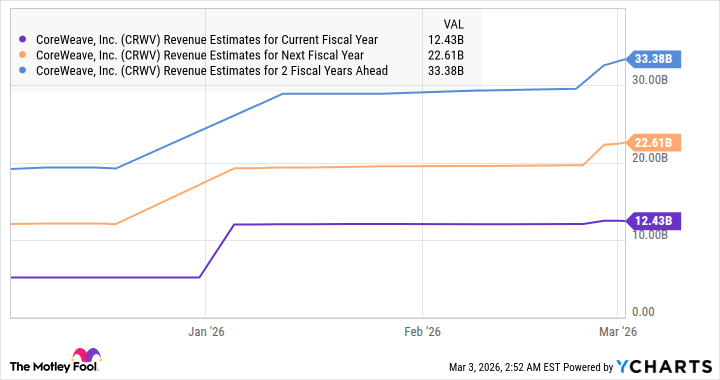

So, CoreWeave's active data center capacity could get close to 4 GW by the end of next year, an increase of almost fivefold from its capacity at the end of 2025. This explains why analysts have raised their revenue expectations from CoreWeave following its latest report.

Data by YCharts.

Here's why the stock is headed to $150

CoreWeave is trading at 6.6 times sales following its recent plunge. That's a slight premium to the tech-focused Nasdaq Composite index's sales multiple of 4.8. The premium can be justified by the phenomenal growth in CoreWeave's revenue and its terrific future potential.

Even if CoreWeave trades in line with the index's average and achieves $33.4 billion in revenue in 2028 (as seen in the chart above), its market cap will jump to almost $160 billion. That's a potential fourfold increase over the current market cap. Given that CoreWeave stock is currently trading around $78, it has the potential to easily coast past $150 within the next three years.