CoreWeave (CRWV -2.73%) is emerging as one of the most important players in the global artificial intelligence (AI) infrastructure ecosystem, building dedicated AI data centers that help customers train models and run inference applications.

The neocloud provider has a close relationship with Nvidia, the leading company in AI chips. CoreWeave's data centers are primarily powered by Nvidia's popular graphics processing units (GPUs) and server processors. What's worth noting is that Nvidia invested $2 billion in CoreWeave in January 2026 to accelerate the build-out of AI infrastructure.

The good news for CoreWeave investors is that the company's close ties with Nvidia are paying off. The neocloud specialist's revenue pipeline is growing rapidly. In fact, it won't be surprising to see CoreWeave stock becoming a multibagger over the next three years. Let's see why that may be the case.

Image source: The Motley Fool.

CoreWeave's aggressive data center build-out will accelerate its growth

The demand for dedicated AI data centers is exceeding supply, primarily due to constraints posed by the electricity needed to run these data centers. Goldman Sachs predicts that data center demand could exceed supply through the end of the decade in a bullish scenario.

NASDAQ: CRWV

Key Data Points

CoreWeave's focus on quickly adding new data center capacity and securing power to build additional data centers in the future explains why the company is witnessing remarkable growth in revenue and backlog. Its revenue in the first quarter of 2026 shot up by 112% year over year to $2.1 billion. However, the year-over-year growth in its revenue backlog was much higher at 284%.

CoreWeave finished Q1 with a revenue backlog of $99.4 billion, driven by the addition of new customers such as Anthropic, Perplexity, and other AI labs. What's more, CoreWeave's existing customers, such as Meta Platforms, Jane Street, and Mistral AI, expanded their contracts with the company. It is easy to see why these companies are giving lucrative contracts to CoreWeave.

The neocloud specialist was operating 1 gigawatt (GW) of active data center capacity in the first quarter of 2026, spread across 49 data centers in the U.S. and Europe. That's a major improvement over the year-ago period's active data center capacity of 420 megawatts (MW). CoreWeave operated 33 active data centers at the end of Q1 2025.

But what's worth noting is that CoreWeave's contracted power capacity, which refers to the agreements it has in place with utility providers for the electricity required to set up more data centers, more than doubled year over year to 3.5 GW. CoreWeave estimates that it will end 2026 with 1.7 GW of active data center capacity.

The company aims to operate 8 GW of active data center capacity by 2030. The good news for CoreWeave investors is that the aggressive conversion of contracted capacity into active capacity will boost its margins. CoreWeave management noted on the latest earnings call that it starts generating revenue from new data centers by the third month of deployment, and its contribution margin (the difference between the revenue generated by the data center and the variable costs associated with running it) starts normalizing in the mid-20% range.

So, the aggressive build-out of new data centers by CoreWeave will eventually have a positive impact on its margins, even though this strategy will lead to surging costs and wider-than-expected losses in the near term. Investors will do well to note that CoreWeave management anticipates "adjusted operating margin to expand sequentially for the remainder of the year, returning to low double digits by Q4."

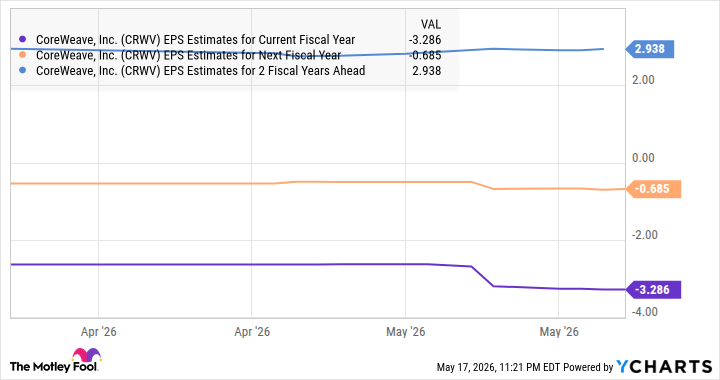

As such, it is easy to see why analysts are expecting CoreWeave's bottom line to improve significantly over the next three years.

Data by YCharts

Consider buying this potential multibagger before it is too late

CoreWeave stock pulled back sharply after the company released its quarterly results on May 7, as its numbers weren't in line with Wall Street's expectations. Investors, however, are missing the bigger picture here.

CoreWeave is playing a crucial role in the proliferation of AI by building dedicated AI data centers. Its aggressive roadmap of bringing 8 GW of active capacity online by 2030 points toward exponential revenue growth, which would eventually boost its bottom line as it starts generating revenue from the data centers it builds.

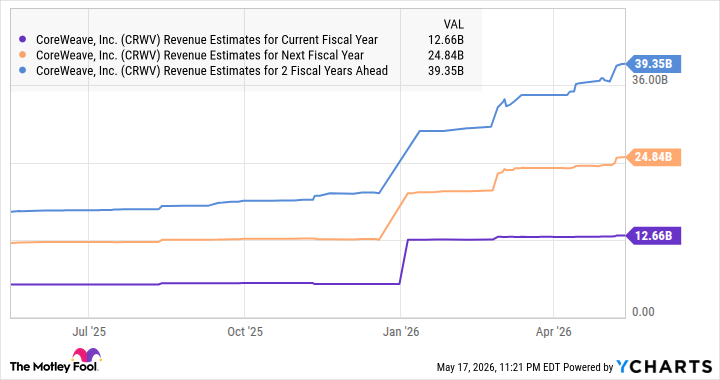

Analysts have become even more bullish about CoreWeave's revenue growth following its latest quarterly report.

Data by YCharts

Assuming its revenue reaches $39.3 billion by the end of 2028, and it trades at 5.6 times sales at that time (in line with the Nasdaq Composite index's average sales multiple), its market cap could reach $220 billion. CoreWeave currently has a market cap of $58 billion, suggesting that this AI stock indeed has multibagger potential, and it would make sense to use the recent pullback to buy its shares before it goes on a bull run.