CrowdStrike (CRWD 0.13%) developed the Falcon cybersecurity platform, which is one of the industry's only holistic, all-in-one solutions. It protects the entire enterprise, from cloud networks to endpoints. It also secures the growing use of artificial intelligence (AI) agents and chatbot applications, which have created new attack surfaces for hackers to exploit.

CrowdStrike stock currently trades down 22% from its all-time high, but it's still one of the most expensive stocks in the cybersecurity space. With that said, the company has issued a 10-year forecast that could fuel significant upside in its stock over the long term.

Does that mean investors should swoop in and buy the dip right now?

Image source: Getty Images.

Falcon is the future of cybersecurity

Legacy cybersecurity vendors require the customer to install clunky software on every device in their organization. Falcon uses a cloud-based architecture instead. This means that each device only requires a lightweight software sensor that streams information back to a centralized data center, where it is analyzed by advanced AI algorithms. These algorithms are trained on over 1 trillion security events every single day, so they are constantly improving.

Enterprises can choose from 33 different Falcon modules (products), so they can build a cybersecurity solution that specifically fits their needs. CrowdStrike offers a subscription option called Falcon Flex, which allows customers to chop-and-change modules during their contract period in line with their predetermined budget. This is great for growing businesses, because their needs are constantly shifting.

NASDAQ: CRWD

Key Data Points

More and more businesses are using AI to boost their productivity, so CrowdStrike continues to launch new products aimed at protecting them. AI agents, for example, have access to sensitive data and mission-critical applications, so a hacker gaining control of just one of them would have catastrophic consequences.

Last August, CrowdStrike introduced Next-Gen Identity Security, which uses a "zero standing privileges" approach to revoke access to critical assets for both human and digital identities when it is no longer needed. It also uses the company's industry-leading threat intelligence to authenticate trusted users and flag strange behavior. Together, these features help reduce the risk of unauthorized access by a hijacked AI agent.

Accelerating revenue growth reflects incredible demand

CrowdStrike generated $1.3 billion in revenue during its fiscal 2026 fourth quarter (ended Jan. 31), which was a 23% increase from the year-ago period. It was the third consecutive quarter in which that growth rate accelerated, which highlights the company's momentum.

CrowdStrike also ended the fourth quarter with a record $5.2 billion in annual recurring revenue (ARR), which was up 24% year over year. The strong growth was led by Falcon Flex subscriptions, which contributed $1.7 billion in ARR. That was up by a staggering 120%. This proves that a substantial number of customers are choosing the Flex option over a more traditional subscription agreement, because of its versatility.

CrowdStrike also had a great year from a bottom-line standpoint in fiscal 2026, with its adjusted (non-GAAP) profit growing by 17% to a record $956.5 million. However, non-GAAP figures exclude one-off and non-cash expenses like stock-based compensation, so Wall Street doesn't always consider this to be "true" profitability. Without those exclusions, the company actually lost $162.5 million for the year, so it still has some work to do on this front.

Should investors buy the dip?

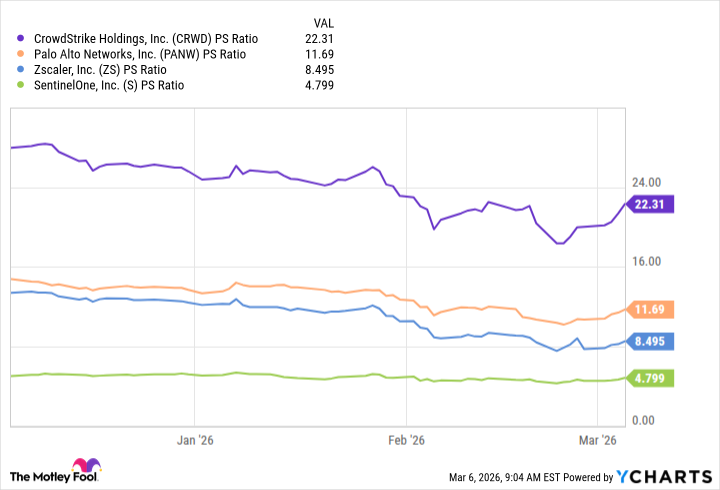

Whether or not investors should buy CrowdStrike stock might entirely depend on their time horizon. Despite its recent 22% share-price decline, it's still trading at a hefty price-to-sales (P/S) ratio of 22.3, making it far more expensive than its rivals in the AI cybersecurity space, including Palo Alto Networks, Zscaler, and SentinelOne.

Data by YCharts.

However, although CrowdStrike stock looks expensive today, management has put forward an ambitious long-term growth forecast which could make its valuation palatable for investors who are willing to hold its stock for the next decade or so. The forecast suggests that the company's ARR could hit $20 billion by fiscal 2036, which would be a whopping 284% increase from its current ARR of $5.2 billion.

It places CrowdStrike stock at a forward P/S ratio of just 5.3, leaving plenty of room for upside relative to its present valuation, and the valuation of its closest rival, Palo Alto Networks. However, investors who buy CrowdStrike stock based on this forecast must be prepared to hold on for the long haul.