Picture, just for a second, the iconic image of a nuclear power plant: a massive, sprawling facility with giant, curved cooling towers and concrete domes that contain reactors.

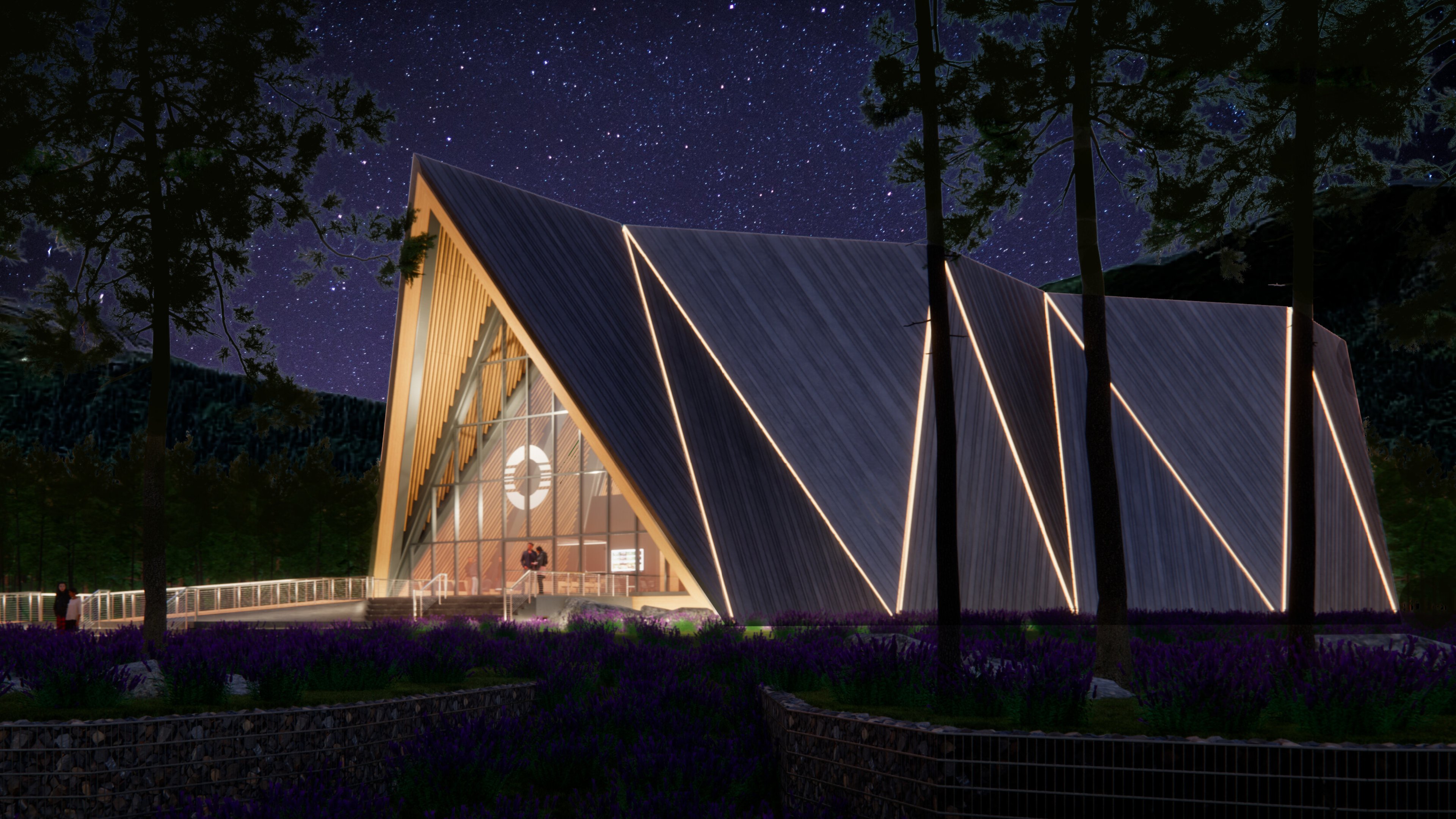

Now, compare this to the small reactor that Oklo (OKLO +9.88%) is trying to commercialize: a small A-frame design with a glassed-in atrium, no cooling towers, and the square footage of a large house. What a difference!

Image source: Oklo.

If Oklo succeeds, this Nordic-looking cathedral (called an Aurora powerhouse) could be found at data centers, industrial and mining sites, research facilities, and other remote areas around the country. That could open a huge market, especially with artificial intelligence (AI) data centers in great need of on-site power.

Getting to that point, however, isn't frictionless. Indeed, if we're going to see this nuclear energy stock more than double past $100, a few things need to happen soon.

What Oklo needs to do to get its stock to $100

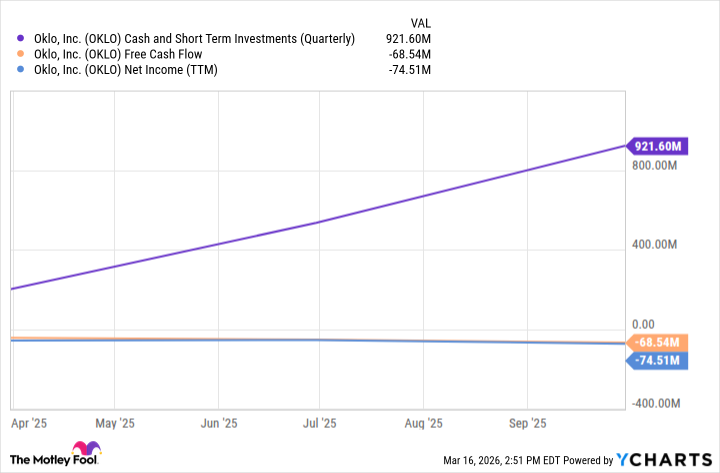

The first thing Oklo needs is the most obvious: a license from the Nuclear Regulatory Commission (NRC) that says it can build and operate its technology at a commercial level. Until it has that license, this company remains essentially pre-revenue, meaning it will burn cash and operate at a loss.

Data by YCharts. TTM = trailing 12 months.

On that front, Oklo has made noteworthy progress. Indeed, over the last year, the policy environment has shifted in Oklo's favor. A new Reactor Pilot Program from the Department of Energy (DOE) has given Oklo the opportunity to demonstrate its technology. If it succeeds in this demonstration, it could move significantly closer to securing a commercial license.

If, for the sake of argument, Oklo does secure that commercial license, that would be wonderful for the company, but it would only set it up for the next challenge: deploying its first Aurora reactor.

For any investors watching rival microreactor developer NuScale Power, which has a commercial license for a small modular reactor (SMR) but lacks a first sale, you know clients aren't exactly lining up for new reactor constructions. Oklo supposedly has 14 gigawatts of projects in the backlog, but until those translate into firm sales, I wouldn't count them as guaranteed revenue yet.

And that brings me here: If Oklo is to trade at $100 or higher, it needs to prove its business model works. This means not just testing one or two reactors for the government or deploying one or two for a customer, but rather rolling out fleets that produce steady cash flow. Until Oklo proves its reactors aren't just functional but also profitable, I don't see this company carrying a $15 billion market capitalization in the future.

NYSE: OKLO

Key Data Points

Oklo faces other risks, too. For example, its reactor design calls for a special fuel called high-assay low-enriched uranium (HALEU), much of which comes from Russia. If its reactors scale up faster than its fuel supply chain can keep up, it could face a bottleneck down the road.

In sum, Oklo remains a high-risk venture, and its stock is going to be volatile for the next year or two. It might hit $100 off positive investor sentiment, but don't expect it to stay there unless the three points above -- NRC licensing, first deployment, scaled operations -- are actually executed.