It was famed investor Warren Buffett who said, "Whether we're talking about socks or stocks, I like buying quality merchandise when it is marked down." I'm with "Uncle Warren" on that, particularly in the case of Lindsay Corporation (LNN 0.50%), a global manufacturer and distributor of agricultural irrigation systems. The company's most recent earnings were less than flattering, pushing the stock down 12% in a day. But I think that presents an opportunity for investors.

Revenue came in at $157.7 million, down about 16% year over year. Earnings also dropped sharply, with earnings per share falling to $1.15.

But this shouldn't really come as a shock. After all, Lindsay is tied directly to the agricultural cycle. When crop prices fall and farmer sentiment weakens, spending gets delayed. Equipment purchases get pushed out. That's what we're seeing right now. And the share price is reflecting this reality.

That said, you should not write this one off. In fact, at these levels, it's actually looking like a bit of a bargain.

NYSE: LNN

Key Data Points

Sound and stable

The truth is, Lindsay's core business is very much sound and stable. In fact, the company's backlog has actually increased to approximately $151.8 million, up from $127 million.

We know that the company is actively executing an $80 million irrigation and technology project in the MENA region (Middle East/North Africa), which management expects will deliver around $70 million in revenue this year.

And while there is evidence that demand for Lindsay's products is constrained by low commodity prices, tight farm credit, and high interest rates, these constraints are temporary.

What isn't temporary are the structural forces driving Lindsay's business: water scarcity, the need for food security, and the limits of arable land.

Long-term demand is key

Global food demand is rising rapidly. At the same time, agriculture already uses about 70% of global freshwater, nearly 40% of cropland faces water scarcity, and there's little room to expand farmland, meaning future growth must come from higher yields.

That's where Lindsay Corporation comes in. Its irrigation systems are designed to improve water efficiency and boost crop output. So while farmer spending may fluctuate in the short term, the underlying need is only increasing.

Image source: Getty Images.

Food demand is rising, water is tightening, and land is finite, making efficient agriculture essential, not optional. And based on where Lindsay trades today, the market isn't fully pricing that in. Especially when you compare it to its peers.

Bargain hunting

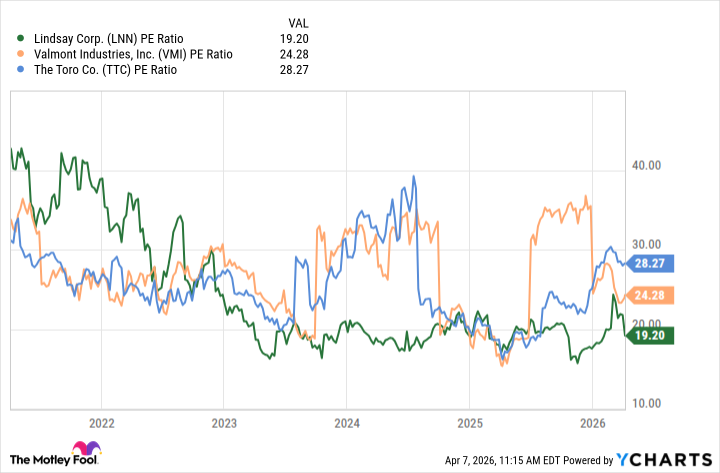

Lindsay is currently trading at about 19 times earnings. Over the past five years, the average P/E has been around 25. So that's a roughly 22% compression in valuation, even though nothing about the long-term story has actually changed.

And when you stack Lindsay up against peers, such as Valmont Industries (VMI +0.81%) and The Toro Company (TTC +0.86%), the valuation gap starts to look a little hard to justify.

LNN PE Ratio data by YCharts

Valmont trades in the mid-20s multiple range, but growth is modest, and while margins are solid, they're not vastly different from Lindsay's.

Then there's Toro, trading 28 times earnings, with the market clearly pricing it like a high-quality growth compounder. But peel that back, and there's nothing particularly exciting here. Revenue growth has been low single digits, and margins aren't meaningfully superior. Yet the stock still commands a premium.

Here's the disconnect: Valmont and Toro are being priced like steady, dependable winners. Which, from a long-term perspective, they are. Lindsay, on the other hand, is being priced like something is fundamentally wrong. But when you look at the numbers, the gap in growth and profitability doesn't support that kind of difference in valuation. And that's where the opportunity starts to show up.

Lindsay doesn't need to suddenly become a fast-growing company for that valuation gap to close. If the market simply values it more in line with its peers, say around 22–24 times earnings, that would imply about a 14% to 23% upside, putting the stock somewhere in the $120 to $130 range.

In other words, nothing extraordinary has to happen. The stock just needs to be viewed as a normal, healthy business. And that's what the numbers indicate.